Send this article to a friend:

December

04

2023

|

Send this article to a friend: December |

|

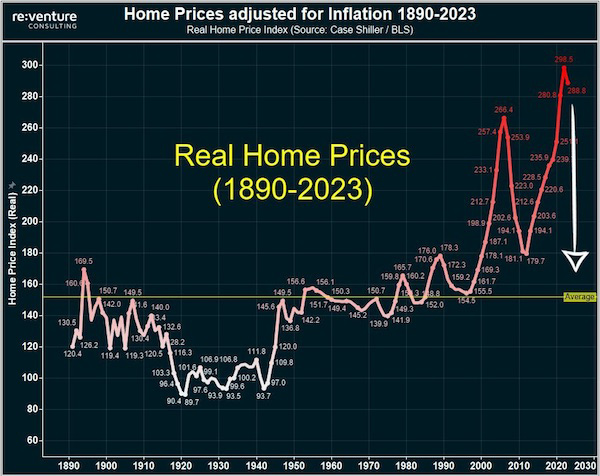

Only a 50% Fall From Here

Then reality regained control from 2006 through 2012, with a 33% crash in home prices, except The Fed and Wall Street decided to not let home prices revert to their mean. They colluded to have Wall Street hedge funds buy up all the foreclosed properties at pennies on the dollar. Part two of the plan was for the captured scumbags at the Fed to reduce interest rates to zero and ignite a home price bubble to exceed all home price bubbles. Of course they also purposefully took the national debt from $16 trillion in 2012 to $34 trillion today, a 110% increase. Meanwhile, the Fed increased their balance sheet from $900 billion to $9 trillion, a ten fold increase.

Virtually no one believes home prices could possibly drop 50%, to the long-term average. Except, long term averages are created by prices going below the long-term average. That would be a 75% decline in home prices. The reason no one believes it could happen is because most people have most of their wealth tied up in their homes. The thought of that asset declining by 50% to 75% is unthinkable, therefore they say it could never happen. Denial is not a river. They say this even though the chart above clearly shows we are in the middle of the greatest bubble of all time, generated solely by money printing. If you think the Federal Government can take our national debt to $60 trillion with no consequences and the Fed can take their balance sheet up another ten fold to $90 trillion, then you can rationalize today’s home prices. With five to ten years remaining in this Fourth Turning, I do anticipate another financial crash to match the level of the debt created boom. That, along with some sort of global conflict and domestic chaos when the 2024 presidential election goes off the rails, will accelerate the reversion past the mean. Of course, I’ve been predicting this since 2012, so take that into account. My message to those who understand maff is: Look Out Below.

As an Amazon Associate I Earn from Qualifying Purchases

-----------------------------------------------------

It is my sincere desire to provide readers of this site with the best unbiased information available, and a forum where it can be discussed openly, as our Founders intended. But it is not easy nor inexpensive to do so, especially when those who wish to prevent us from making the truth known, attack us without mercy on all fronts on a daily basis. So each time you visit the site, I would ask that you consider the value that you receive and have received from The Burning Platform and the community of which you are a vital part. I can't do it all alone, and I need your help and support to keep it alive. Please consider contributing an amount commensurate to the value that you receive from this site and community, or even by becoming a sustaining supporter through periodic contributions. [Burning Platform LLC - PO Box 1520 Kulpsville, PA 19443] or Paypal

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)