Send this article to a friend:

December

16

2021

|

Send this article to a friend: December |

|

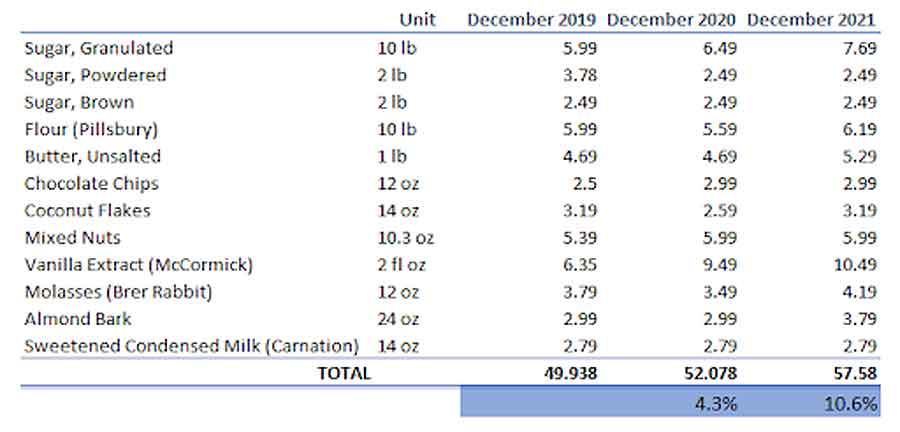

Christmas Cookie Inflation Index, 2021 Update

— Strong Towns: A Bottom-Up Revolution to Rebuild American Prosperity Last year, I published the first Christmas Cookie Inflation Index, drawing on data I collected in 2019 and updated in 2020. It was a nice article where I shared the story of my dear grandmothers and their Christmas baking, a tradition I picked up and adapted after they passed away. I’ve been baking for a couple weeks now this year, and look forward to sharing the results of my labor with friends and family. In last year’s article, I wrote that “Americans are being gaslit about inflation.” In my assessment, we were more than a decade past the “there won’t be inflation” phase and were well established in the “there is no inflation” part of the narrative. When you give rich people money, the stuff that rich people buy—stocks, real estate, yachts, art—goes up in price. The inflationary mechanism of more dollars chasing the same number of goods is too simple (and inconvenient) to be worthy of intellectual objectification. Unfortunately, too simple doesn’t mean wrong. This year saw inflation escape into the common narrative. Money given to non-elites as part of COVID recovery chased the same goods—notably, labor—and, predictably, prices went up, dramatically in many instances. Let’s start with the Christmas Cookie Inflation Index, a basket of 10 ingredients I use to bake cookies. These are the same ingredients my grandmothers used for decades baking the same cookies. In other words, this basket is comparable over time without needing substitution or hedonic adjustments, two mechanisms used to suppress inflation during the first two phases of the inflation story. Substitution is the idea that people react to changing prices by substituting one set of goods for another. For example, if steak is too expensive, you can substitute chicken. As the Bureau of Labor Statistics (BLS) suggests, “the dominant substitution effect is one of consumers shifting toward relatively cheaper products.” In the mind of an economist, this has the effect of overstating inflation, so substitution adjusts the inflation rate downward to compensate. If you can no longer afford steak because the price has gone up and instead switch to eating chicken, that actually reduces the rate of inflation, since your overall cost of living is now less. This is why many of us have long experienced rising prices while we’re told “there is no inflation.” Hedonic adjustment is another method used to reach the same conclusion. Your new television may cost 500% more than the television you bought a few years ago, but if it is determined that the television is 507% more valuable because of all the new features, then an hedonic adjustment will say that the price has actually gone down by 7% (that’s the example given on the BLS website). You are paying more, but you are getting more. That works in theory—especially for the affluent, where this price differential is not critical—but the reality is that you don’t have the option of buying the cheaper television with fewer features. For you, the price goes up while you are told “there is no inflation.” The way you know that substitution and hedonic adjustments are a gimmick is that they only work in one direction. It’s a lot like computing time lost to congestion when trying to justify a road widening, but ignoring it when building an interchange. The goal, and it’s not really a secret, is to adjust inflation rates downward from what would be reported if the same basket of goods were reflected over time. Many economists and politicians call this an increase in accuracy. I think that is too comforting for policymakers and don’t subscribe to that interpretation. The Christmas Cookie Inflation Index conveniently avoids substitution effects (don’t you dare substitute these ingredients) and also hedonic adjustments, since it is the same base ingredients year after year. This year, it is up 10.6% over last year, including some items that are up more than 20%, such as almond bark (27%), coconut flakes (23%), and molasses (20%).

Like usual, and as would be expected from a non-adjusted basket of goods, the Christmas Cookie Inflation Index is running hotter than the official inflation rate, which is 6.8% over the past 12 months. Over the last year, we passed completely through the third phase of the inflation story, “inflation is transitory.” In other words, inflation escaped into the general population and has to be acknowledged, but it is a short-term effect that will go away soon. We were bombarded with this messaging throughout the summer and fall but Jerome Powell, after being re-nominated for another term as chair of the Federal Reserve, acknowledged that inflation was not going away anytime soon. One thing to note on the transitory argument is that it largely hinged on so-called supply chain shortages. We were all shown pictures of ships backed up at the ports, waiting to offload goods into a system where we just didn’t have the workers or the capacity to unload it. Fix those supply chain problems, and it will all go back to normal, or so the story went. That narrative would hold some validity if we were importing less than we were in the past, if a worker shortage and other COVID effects were cutting into our capacity to process imported goods and get them distributed to markets across the country. That’s not the case. We have had month after month of record trade deficits, importing vastly more than we are exporting. Supply chain shortages or more money chasing the same goods? I find the supply chain narrative unconvincing. This gets us to the most interesting part of the story. We’re now being told that inflation is good, which is the fourth and final phase. Serious people are saying that rising prices of everyday goods like rent, food, and transportation is bad for the rich and good for the rest of us. We even have Paul Krugman arguing that there really is no “good reason to believe that inflation hits low-income households especially hard.” Only an economist could be so out of touch with reality. If you need reasons to believe the obvious, Gallup reports that inflation is causing hardship for nearly half of all American households. That’s okay, though, because hardship is good for you. I know this because I’m a Catholic and believe in redemptive suffering, although I’m guessing that is not what inspires Krugman and his peers. Either way, we seem almost certain to be in for more redemptive suffering (aka inflation) in 2022. That is because, from a policy perspective, we are trapped. Having too much money in the system chasing goods is driving up prices and creating hardship, especially for the poor. To address that, we are going to be told that we need to give money to the poor. Extending the child tax credit, which sends a check each month to families with children, is a major part of the president’s Build Back Better agenda and would do just that. Whether you like this policy or not (I think it is popular enough to become law), standard economic theory would call this inflationary. You’re giving more money to people when excessive money in the system is the problem. They are going to compete with each other to spend it and that will drive up prices. Then there is the Modern Monetary Theory (MMT) approach, which would say to go ahead and send that check but, now that we have inflation, we must also undertake a broad tax increase to get all that excess money out of the system. The tax-increase-during-inflationary-episode was always the poison pill that made MMT completely absurd from a real life standpoint. Prices are going up, which makes it the perfect time for a middle class tax hike. Such a tax increase will never happen, the honest among MMT advocates know it, and so you hear them clinging—in the most obnoxiously parsed kind of way—to the idea that “transitory” may mean a long time, but it will eventually be over. Quite a theory. That it will be over someday is little consolation for those who are going to suffer during the transition, a list of our fellow humans that will only expand. If we aren’t going to raise taxes to get the excess money out of the system (we’re not, sorry MMT), then we are going have either: (a) sustained inflation and all the pain and anxiety that comes with it, or (b) substantially higher interest rates, which is the only remaining mechanism to remove money from the system. It seems very likely that even modestly higher interest rates (let’s say 6.8%, which would make real, inflation-adjusted rates 0%) will crash the stock market, which is weighed down with record levels of corporate debt. It will certainly blow up the bond market, which has not seen significant rate increases for a generation. The largest real-estate bubble in history would experience a massive pin prick with rising rates, something many of us remember from 2008 as being a near-fatal experience. And try refinancing a $29 trillion national debt with interest rates 5% higher than they are now. The president’s Build Back Better plan has been stalled all year, largely over its size, which is currently around $1.75 trillion, an amount that would be spent over multiple years. In comparison, a 5% hike in rates would require the federal government to come up with an additional $1.45 trillion every year just to pay interest on our existing debt. Sure, you can have the Federal Reserve print that money and use that to pay our debts, in which case the inflation cycle accelerates. That’s what is meant by “trapped,” and, have no doubt, we are trapped. The final stage in the inflation story, before the painful resolution of it, will be the part where our leaders, and their followers, demand that people like me be silent. Or be discredited. You see, inflation quickly becomes a game of expectations. If the broad society is expecting inflation, they will act in ways that accelerate inflation, like raising prices knowing everyone is already anticipating it. The policy response is to talk us all down. I would call this gaslighting. It’s a credible strategy that has worked for more than a decade now. In the coming months and potentially years, look for more articles like this onecalling people with inflation concerns “hysterical.” They will say that people who talk about inflation are causing inflation, that which shall not be named. I don’t think this will be effective, but I believe it will happen. When it does, you know the endgame is near. For years, I have been criticized as heartless and backward for insisting on sound economics, hard money, and fiscal discipline. I am not heartless. In fact, quite the opposite. I am fearful of a world where we run large experiments on ourselves, willing—as humans so often are—to offer up the poor and disenfranchised in pursuit of what the elites (far too conveniently) believe is for the greater good. Early, painful feedback on our hubris is necessary to avoid the long-term pain and suffering wrought by our folly. This is the lesson of history, one we seem destined to relearn again and again. I’ll end this with the words of Jane Jacobs, who wrote so poignantly about the folly of the comparatively less insane macroeconomics of her day, in Cities and the Wealth of Nations:

To repair the damage, let’s make 2022 the year we dedicate ourselves to doing what we can to localize our economy. It won’t be a perfect solution, but it is the only viable alternative to ceding ever more power to centralized authorities, those promising to save us from the wreckage they continue to create.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)