Send this article to a friend:

November

19

2018

|

Send this article to a friend: November |

|

Soaring Health-Care Costs Forced This Family to Choose Who Can Stay Insured

Then, in 2012, Maribel discovered she had breast cancer. “Your world comes crumbling down,” David says. Maribel had a double mastectomy, paid for by the insurance David obtained through his job, a small welding business with fewer than a dozen employees. But two years into Maribel’s recovery and treatment, David’s boss gathered his staff into his office. Don’t worry, he said, business is good. Your jobs are safe. But there would be one change: Health insurance offered through the company would soon be discontinued. It had simply become too expensive for the small company to provide it. For David, the responsible head of a thriving middle-class family, having health insurance was non-negotiable. But the coverage he found to replace the company plan cost $1,375-a-month, up from the $260 a month he had been paying. Suddenly, the family’s health insurance tab “was more than what we were paying for our mortgage,” David says.

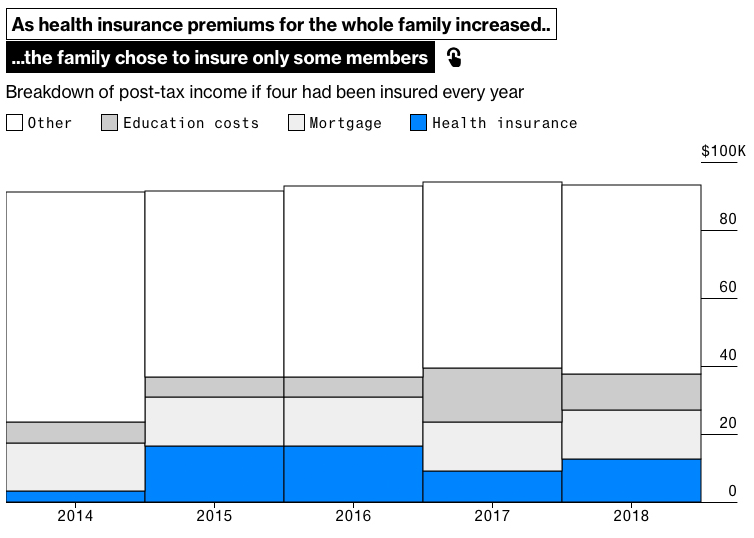

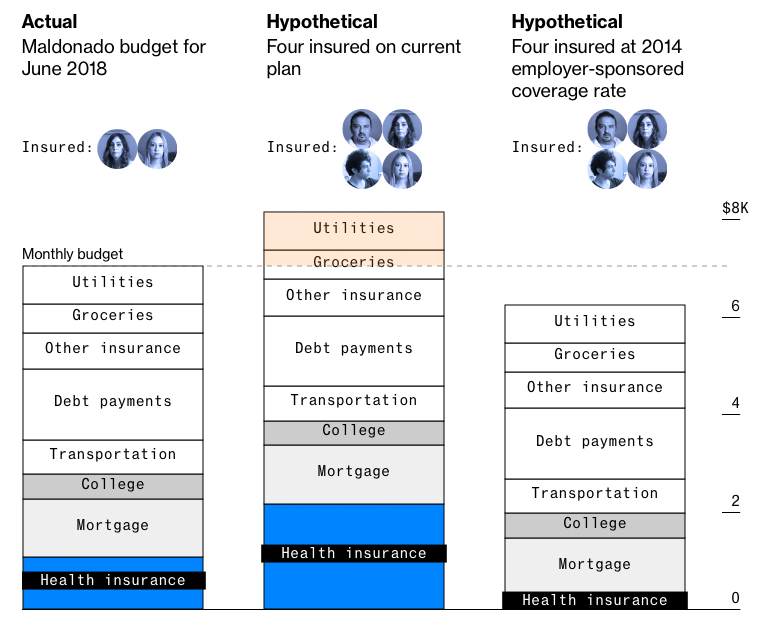

The Maldonados’ story is a tale of middle-class Americans juggling family finances. With the ever-present pressure of a mortgage and looming college tuition, many otherwise-financially sound families face a stark choice when health-care premiums shoot wildly higher: Take on debt or opt out of the medical system and hope for the best. The Maldonados’ story is part of Bloomberg’s year-long examination of Americans struggling to afford the rising costs of health care—and the painful financial and medical trade-offs that inevitably follow. Since Bloomberg began talking to the family in July, their insurance costs have leveled off and are even expected to dip next year, by about $100 a month. While that might sound like a positive development, the Maldonados have been so rocked by escalating health insurance costs in recent years that David holds little hope for real improvement. Nor does he think the outcome of the midterm elections will change anything. “It’s just going to be a bigger mess,” he says. He wasn’t always so downbeat. But the last six years have been brutal. Just as he doubled down to pay for the family’s new health-care coverage, other expenses seemed to conspire to cut even more into the Maldonados’ budget. Their son Cristian graduated from high school in 2014 and enrolled at Texas A&M Commerce, adding to the family’s budget about $20,000 in annual expenses for college tuition, rent and food. The family income was too high to qualify for financial aid, so the Maldonados began borrowing the roughly $13,000 a year they needed to cover their savings gap for Cristian’s tuition during his college years. Then, a few weeks before the 2016 presidential election, David received a letter from his insurer, Blue Cross Blue Shield of Texas, Inc., announcing a 38 percent increase in premiums for the upcoming year. His monthly premiums would shoot up to almost $1,900. That’s the day David says he decided to vote for Donald Trump. The family stopped going on vacation. They stopped eating out, even on weekends. They refinanced the mortgage, taking advantage of low rates, tapping $20,000 in equity. That got swallowed up almost immediately. With their daughter Alexa about to start college to study nursing, more expenses loomed. So when it came time to sign up for coverage for 2017, David knew he wouldn’t be able to swing the nearly $23,000 annual tab for the family’s plan. There was only one thing left to do, as David saw it. He dropped out of the family plan, leaving himself uninsured. He also asked Cristian whether he’d be all right doing the same. Cristian agreed. That would bring the monthly premium to $750. “We went by who got sick the most,” David says. Of the three—dad, son and daughter—Alexa required more care. She’d been plagued by asthma attacks most of her teenaged years. Still, the decision didn’t go down easily. David worked hard all his life and was a solid, successful member of his community. Yet he couldn’t afford proper health insurance for the family. That realization stung. “I work my butt off,” David says. “Why’s the deductible so high, and everything’s so high,” when insurance executives take home millions of dollars a year.

To further economize, David stopped getting routine check-ups, even though he was diagnosed years ago with high blood pressure. Instead, he donates blood every four or five months in exchange for a free check on his own blood pressure, as well as his hemoglobin and cholesterol levels. Cristian forgoes doctors altogether. “If I have a fever or something,” Cristian says, “I just go to the drugstore and buy some Tylenol and wait it out.” Even with half the family off health insurance, medical bills for Alexa and Maribel piled up. They were able to keep seeing their doctors—Alexa for her asthma and walking pneumonia flare-ups, Maribel for her cancer screenings and tamoxifen to keep the disease in check. But with the plan’s $5,000 deductible, a lot of money was bleeding out of the family budget for the drugs before coverage kicked in. Another round of health insurance premium hikes hit the family as Alexa started college. This time, the dreaded letter from Blue Cross Blue Shield announced that monthly premiums for mother and daughter would increase to $1,060 from $750—an additional $3,720 per year—for one of the least-expensive plans available. His daughter’s asthma hadn’t improved, and his wife was still taking tamoxifen every day. David had already been running a monthly household deficit of $500 to $600 that year, piling on credit-card debt to be able to keep up with the monthly premiums. No matter. When January 2018 came around and the new rates kicked in, David kept paying. By then, everyone in the family was focusing on ways to save health-care dollars. Alexa visited an alternative-medicine clinic in Houston. About a week into the treatment, with her breathing improving, Alexa felt she no longer needed her inhaler. David, reluctantly, saw an opportunity to cut back. In June, he pulled her aside and asked whether she’d be all right off the insurance policy.

“It was a waste of money,” Alexa recalls. At college, “I maybe went to the doctor once.” David took her off the plan. That immediately saved about $300 in monthly expenditures. Since July, Alexa has been without health insurance, leaving Maribel as the only family member covered through the policy, which still costs $750 every month. David has trouble accepting that, just a few years ago, he was paying merely $260 a month for the entire family’s coverage. “If something happens to me, who’s going to pay the bills?” He briefly considered getting health care in Mexico, but the idea quickly fizzled. “If I were closer to the border, I would go to Mexico every time,” he says. “It’s about eight to nine hours driving. It would be cost-ineffective.” But not impossible: He holds dual citizenship, while his wife and children are eligible for Mexican passports. Still, it wouldn’t be an easy road. “It’s a process and it’s paperwork—and anything with the Mexican government, they make it so complicated,” David says. Plus, he’s wary of the quality of care and availability of care under Mexico’s socialized medical system. “It’s fine if you break an arm,” David says, “but if you have anything big, you’re going to be put on the waiting list.”

David recently turned 49. Maribel is 48. Though they’ve paid off all but $20,000 on their mortgage, they have no retirement savings so far, other than the equity in their house. “I wish someone would’ve told me back then: ‘Start saving, you know, even if it’s just 5 percent out of your paycheck every week,’” David says. “I wasn’t told that.” It wasn’t long ago that the family’s finances seemed to be on a permanent upward trajectory. Now, he laments, there’s not even enough cash on hand to fix the windshield of Alexa’s SUV, which has been cracked for several months. David doesn’t see any real light until the day both kids will be out of college with well-paying jobs, health benefits and retirement plans of their own. What could throw a wrench into that vision, of course, is an unexpected medical emergency. The midterm elections have only reinforced David’s sense that Washington isn’t up to the task of improving the family’s health-care options. He’s still a firm Trump supporter, and the prospect of Republicans and Democrats sharing power isn’t something for him to celebrate. He watched the Texas Senate race results closely on election night, flipping among Fox News, ABC and CNN. While he thinks Ted Cruz was “the lesser of two evils,” David was relieved to see the candidate he voted for prevail over Democrat Beto O’Rourke, who ran on a platform that listed single-payer health care as one of its cornerstones. “I’m all for health care for all,” David says, “but I’m also realistic. Where are you going to cut the money to pay for that?”

www.bloomberg.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)