Send this article to a friend:

October

14

2021

|

Send this article to a friend: October |

|

Retirement Security Month Missing Its Most Important Ingredient

And it doesn’t matter which politicians take office, both sides of the aisle often meddle with Social Security and other retirement safety nets, but neither seem to produce tangible results that actually make retirement more secure. (At least, not very often). October is National Retirement Security Month This means the government is devoting resources to promote the idea that retirement savers can enjoy their “golden years” without worrying about their expenses. This sounds like a great idea when taken at face value. No retiree wakes up and hopes their day-to-day expenses and emergencies will overtake their retirement income (which is usually fixed to some degree). It’s also easy to take for granted the elements that make up a secure retirement, like these highlighted in an article in Capital Journal:

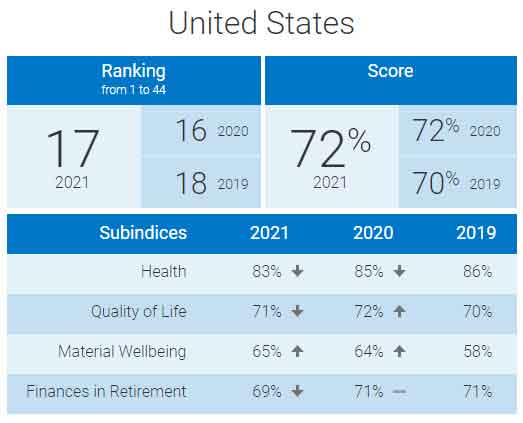

The way it’s written, it sounds like all of these things are easy to do, but what if the real-world picture is much more complex than a few nice sounding bullet points? 40% say “It will take a miracle” to boost retirement security There is a lot more to enjoying a secure retirement than just estate planning and tax advantages. According to the Natixis Global Retirement Index (GRI), there are also “four critical concerns for retirement savers, including inflation, interest rates, public debt, and a world of worries.” Natixis ranks countries according to its GRI, and by their methodology, the United States isn’t doing quite as well as you might think. In fact, it doesn’t even crack the top 10:

The same ranking system puts the U.S. public debt near the top, at #3 out of the top 25 countries in the world, with Japan and Greece leading the way. But worse than all of that, according to this Naxis report, even wealthier retirement savers think “it will take a miracle” to retire securely:

A miracle isn’t something we should count on to happen. Which leaves the question: What can retirement savers do to boost the security of their retirement? The same report finished with a similar conclusion that we’ve reached a number of times:

We have to look out for ourselves. We just can’t count on anyone else to do it for us – not Congress, or the Social Security Administration or our parents. We must each overcome this challenge for ourselves. The good news is, this means you do have options. But it also means you might have to consider solutions that fall outside of the traditional way of saving for retirement. Secure your own retirement by thinking outside the boxTo help increase retirement security, savers can consider diversifying beyond stocks and bonds. That means thinking outside of the box, which can help increase the chances you’ll enjoy a stress-free lifestyle well into your golden years. And that’s where a self-directed IRA shines. A self-directed IRA focuses on the benefit of providing more flexibility with your investments. For example, you’re not restricted to choosing from one broker’s menu of mutual funds and other paper-based assets. It’s like taking the training wheels off your retirement savings. After all, it’s your hard-earned money. Why should you let a stranger tell you what you should and shouldn’t invest in? This flexibility also allows you to diversify your retirement savings with often-overlooked assets. Adding physical precious metals like gold, silver or platinum to your savings helps provide the benefits of diversification in a form that can’t be hacked, crashed or simply inflated away. Many Americans feel a sense of stability and security based on their ownership of physical precious metals. There’s a reason gold is called “portfolio insurance.”

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)