Send this article to a friend:

October

08

2021

|

Send this article to a friend: October |

|

The funding challenges ahead

There are three categories of buyer for US Federal debt: the financial and non-financial private sector, foreigners, and the Fed. The banks in the financial sector have limited capacity to expand bank credit, and American consumers are being encouraged to spend, not save. Except for a few governments, foreigners are already reducing their proportion of outstanding federal debt. That leaves the Fed. But the Fed recently committed to taper quantitative easing, and it cannot be seen to directly monetise government debt. That is one aspect of the problem. Another is the impending rise in interest rates, related to non-transient, runaway price inflation. Funding any term debt in a rising interest rate environment is going to be considerably more difficult than when the underlying trend is for falling yields. There is the additional risk that foreigners overloaded with dollars and dollar-denominated financial assets are more likely to become sellers. Not only are foreigners overloaded with dollars and financial assets, but with bond yields rising and stock prices falling, foreigners for whom over-exposure to dollars is a speculative position going wrong will undoubtedly liquidate dollar assets and dollars. If not buying their own national currencies, they will stockpile commodities and energy for production, and precious metals as currency hedges instead. The Fed will be faced with a bad choice: protect financial asset values and not the dollar or protect the dollar irrespective of the consequences for financial asset values. And the Federal Government’s deficit must be funded. The likely compromise of these conflicting objectives leads to the risk of failing to achieve any of them. Other major central banks face a similar quandary. Funding ballooning government deficits is about to get considerably more difficult everywhere.

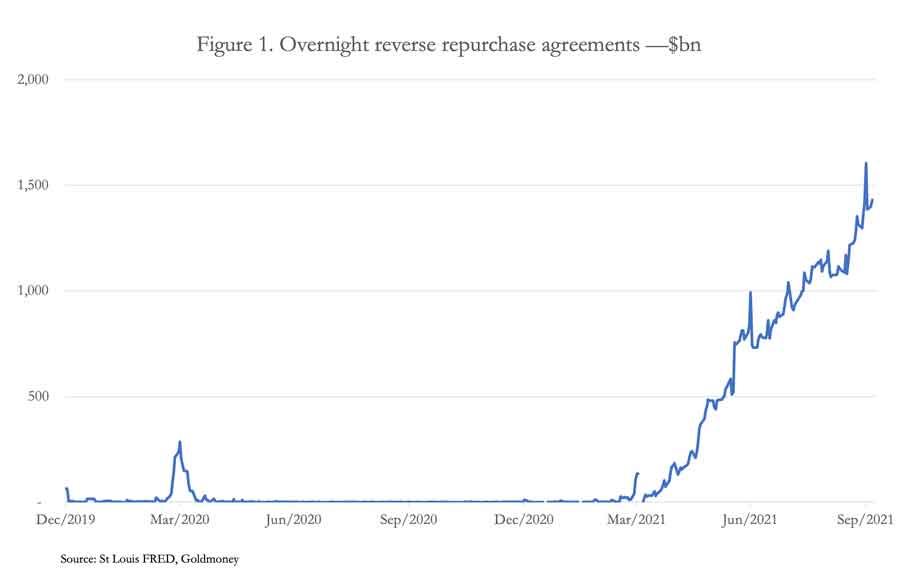

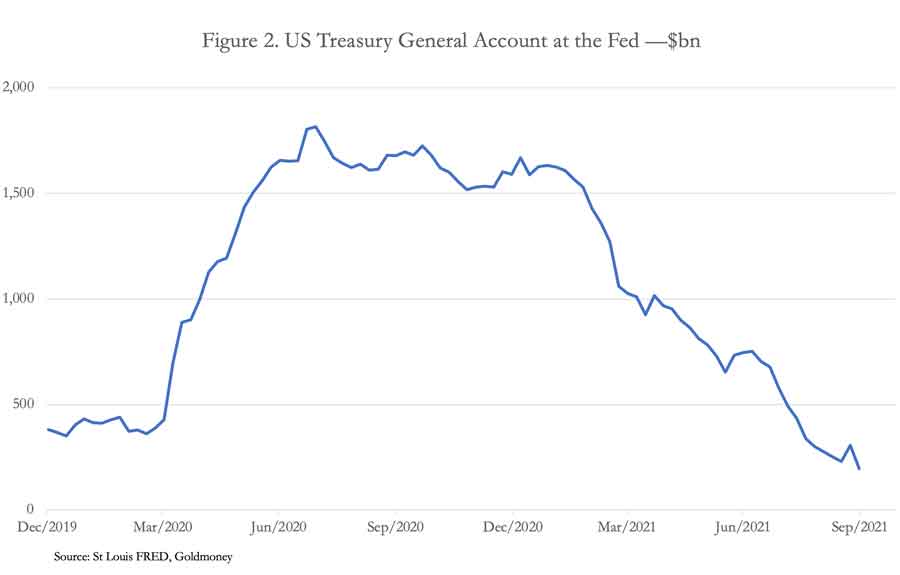

IntroductionOur headline chart in Figure 1 shows the excess liquidity in the US economy that is being absorbed by the Fed through reverse repos (RRPs). With a reverse repo, the Fed lends collateral (in this case US Treasuries overnight from its balance sheet) to eligible counterparties in exchange for overnight funds, which are withdrawn from public circulation. As of last night (6 October), total RRPs stood at $1,451bn, being the excess liquidity in the financial system with interest rates set by the RRP rate of 0.05%. Simply put, if the Fed did not offer to take this liquidity out of public circulation, overnight dollar money market rates would probably become negative. The chart runs from 31 December 2019 to cover the period including the Fed’s reduction of its funds rate to the zero bound and the commencement of quantitative easing to the tune of $120bn every month —they were announced on 19th and 23rd March 2020 respectively. Other than the brief spike in RRPs at that time which was a wobble to be expected as the market adjusted to the zero bound, RRPs remained broadly at zero for a full year, only beginning a sustained increase last March. Much of the excess liquidity absorbed by RRPs arises from government spending not immediately offset by bond sales. Figure 2 shows how this is reflected in the government’s general account at the Fed. The US Treasury’s balance at the Fed represents money not in public circulation. It is therefore latent monetary inflation, which is released into the economy as it is spent. Since March 2021, the balance on this account fell by about $800bn, while reverse repos have risen by about $1,400bn, still leaving a significant balance of liquidity to be absorbed arising from other factors, the most significant of which is likely to be seepage into the wider economy from quantitative easing (over two trillion so far and still counting).

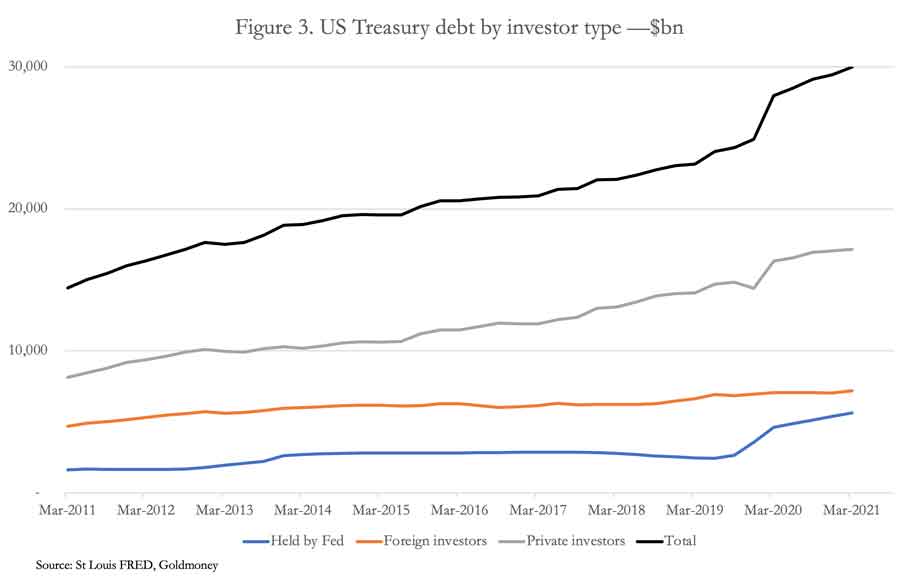

The US Treasury has draw down on its general account because had it accumulated balances from bond funding in excess of its spending ahead of the initial covid lockdown. And its debt ceiling was getting closer, which is currently being renegotiated. But this is only part of the story, with the Federal deficit running at about $3 trillion in the fiscal year just ended. That is a huge amount of government “fiscal stimulus”, and clearly, the private sector is having difficulty absorbing it all. The scale of this deficit, debt ceilings aside, is set to increase under the Biden administration. If the US economy is already drowning in dollars, it is likely to worsen. Assuming the debt ceiling negotiations raise the Treasury borrowing limit, the baseline deficit for the new fiscal year must be another $3 trillion. Optimists in the government’s camp have looked for economic recovery to increase tax revenues to reduce this deficit enough together with selective tax increases to allow the government to invest additional capital funds in the crumbling national infrastructure. A more realistic assessment is that unexpected supply disruption of nearly all goods and rising production costs are eating into the recovery, which is now faltering. And it is raising costs for the government in its mandated spending even above the most recent assumptions. It is increasingly difficult to see how the budget deficit will not increase above that $3 trillion baseline. This article looks at the funding issues in the new fiscal year following the expected resolution of the debt ceiling issue. The principal problems are its scale, how it will be funded, and the impact of price inflation and its effect on interest rates. Assessing the scale of the funding problemThere are three distinct sources for this funding: the Fed, foreign investors, and the private sector, which includes financial and non-financial businesses. Figure 3 shows how the ownership of Treasury stock in these categories has progressed over the last ten years and the sum of these funding sources up to the mid-point of the last US fiscal year (31 March 2021). Over that time total Treasury debt more than doubled to nearly $30 trillion.

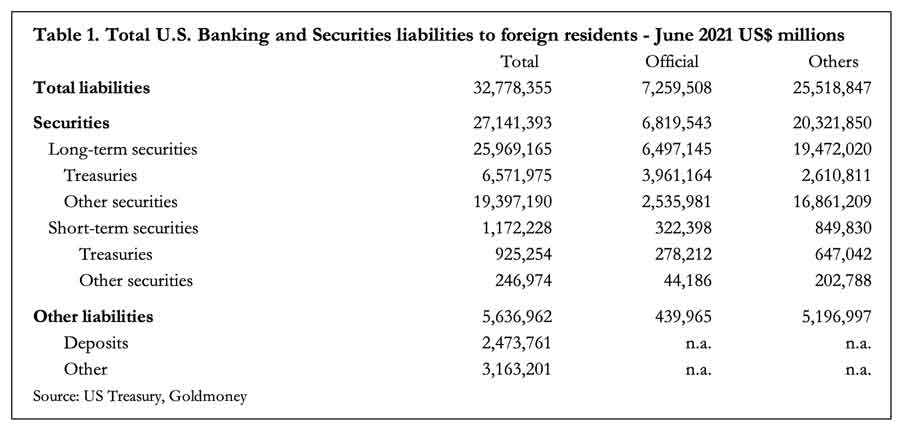

The funding of further debt expansion from these levels is likely to be a significant challenge. Initially, the Fed can release funds by reducing the level of overnight RRPs, some of which will become absorbed directly, or indirectly, in Treasury funding. But after that financing will become more problematic. Since 2011, the Fed’s holdings of US Treasury debt have increased from 11% to 19% of the growing total, reflecting QE particularly since March 2020. At the same time the proportion of total Treasury debt owned by foreign investors has fallen from 32% to 24% today, and now that they are highly exposed to dollars, they could be reluctant to increase their share again, despite continuing trade deficits. Private sector investors, whose share of the total at 57% is virtually unchanged from ten years ago, can only expand their ownership by increasing their savings and through the expansion of bank credit. But with bank balance sheets lacking room for further credit expansion and consumers inclined to spend rather than save, it is difficult to envisage this ratio increasing sufficiently as well. Clearly, the Fed has been instrumental in filling the funding gap. But the Fed has now said it intends to taper its bond purchases. Unless foreign investors step in, the Fed will be unable to taper. Excess liquidity currently reflected in outstanding RRPs can be expected to be mostly absorbed by expanding T-bill and short-maturity T-bond funding, which might buy three- or four-months’ funding time and not permit much longer-term bond issuance. But after that, the Fed may be unable to taper QE. Foreign funding problems While we cannot be privy to the bimonthly meetings of central bankers at the Bank for International Settlements and at other forums, we can be certain that there is a higher level of monetary policy cooperation between the major central banks than is generally admitted publicly. On matters such as interest rate policy it is important that there is a degree of cooperation, otherwise there could be instability on the foreign exchanges. And to support the dollar’s debasement, policy agreements between important foreign central banks may need to be considered. This is because the dollar’s role as the reserve currency gives the US Government and its banks not just an advantage of seigniorage over the American people, but over foreign holders of dollars as well. Dollar M1 money supply is currently $19.7 trillion, approximately 50% of global M1 money stock.[i] Therefore, its seigniorage and the world-wide Cantillon effect from increasing public circulation is of great advantage to the US Government, not only over its own people but in transferring wealth from foreign nations as well. This is particularly to the disadvantage of any other national government which, following sounder monetary policies, does not expand its own currency stock at a similar rate while being forced to use dollars for international transactions. Ensuring currency debasement globally is therefore a compelling reason behind monetary cooperation between governments. By agreeing on permanent currency swap lines with five major central banks (the ECB, the Bank of Japan, the Bank of England, the Bank of Canada, and the Swiss National Bank) they are drawn into supporting a global inflationary arrangement which ensures the stock of dollars can be expanded without consequences on the foreign exchanges. Ahead of its massive monetary expansion on 19 March 2020, to keep other central banks onside temporary swap arrangements were extended to nine other central banks, ensuring their compliance as well.[ii] But notable by their absence were the central banks whose governments are members and associates of the Shanghai Cooperation Organisation, which will have found that their dollar holdings and financial assets (mainly US Treasuries) have been devalued without consultation or recompense. It is therefore not surprising that foreign governments other than those with permanent swap lines are increasingly reluctant to add to their holdings of dollars and US Treasuries. By selectively excluding major nations such as China from swap line arrangements, by default the Fed is pursuing a political agenda with respect to its currency. International acceptability of the dollar is being undermined thereby when the US Treasury is becoming increasingly desperate for inward capital flows to fund its budget deficits. Even including allied governments, all foreigners are now reducing their exposure to US dollar bank deposits, by 12.9% between 1 January 2020 and end-July 2021, and to US T-Bills and certificates by 20.7% over the same period. The only reason for holding onto longer-term assets is in expectation of speculative gains. The situation for longer-term Treasury bonds is not encouraging. The US Treasury’s “major foreign holders” list of holders of longer-maturity Treasury securities, shows the list to be dominated by Japan and China, between them owning 31.5% of all foreign owned Treasuries. Japan’s cooperative relationship with the Fed was confirmed by Japan increasing her holdings of US Treasuries, but only by 1.3% in the year to July 2021, while China and Hong Kong, which between them hold a similar amount to Japan, reduced theirs by 3%.[iii] The ability of the US Treasury to find foreign buyers other than for relatively smaller amounts from offshore financial centres and oil producing nations therefore appears to be potentially limited. We should also note that total financial assets and dollar cash held by foreigners already amounts to $32.78 trillion, roughly one and a half times US GDP — dangerously high by any measure. This total and its breakdown is shown in Table 1.

The question then arises as to what foreigners will buy when they sell their dollars. Governments without a strategic imperative may prefer at the margin to adjust their foreign reserves in favour of the other major currencies and gold. But out of the total liabilities shown in Table 1 official institutions only hold $4.284 trillion long- and short-term Treasuries, which includes China and Hong Kong’s holdings, out of the $7.2 trillion total shown in Figure 2 earlier in this article. The $3 trillion balance is owned by private sector foreign investors. Excluding China and Hong Kong’s $1.3 trillion, US Treasury debt held by foreign governments is under 10% of all foreign holdings of dollar securities and cash. What is held by foreign private sector actors therefore matters considerably more, bearing in mind that it can all be classified as speculative, being a foreign currency imparting accounting risk to balance sheets and investment portfolios. If interest rates rise because of price inflation not proving to be transient, it will lead to significant investment losses and therefore selling of the dollar, triggering a widespread repatriation of global funds. A global increase in bond yields and falling equity values will also force sales of foreign securities by US investors. But with US investors being less exposed to foreign currencies in correspondent banks and with a significantly lower level of foreign investment exposure, the net capital flows would be to the disadvantage of the dollar. Some of the proceeds from dollar liquidation by foreigners are likely to lead to commodity stockpiling and at the margin some of it will hedge into precious metals, driving their prices higher. The long-term suppression of precious metal prices would to come to an end. Domestic problems for the Fed Clearly, the resumption of government deficit funding will no longer be supported by foreign purchases of US Treasuries at a time when trade deficits remain stubbornly high. This throws the funding emphasis onto the Fed and domestic purchasers of government debt. But as stated above, the private sector will need to reduce its consumption to increase its savings. Alternatively, banks which have limited capacity to do so will have to expand credit to purchase Treasury bonds, which is not only inflationary, but diverts credit expansion from the private sector.Consumers are charging in the opposite direction from increasing savings, drawing them down in favour of increased consumption. This is partly due to them returning to their pre-covid relationship between consumption and savings, and partly due to a shift against cash liquidity in favour of goods increasingly driven by expectations of higher prices. With their fingers firmly crossed, the latter is believed by central bankers and politicians to be a temporary phenomenon, the consequence of imbalances in the economy due to logistics failures. But the longer it persists, the more this view will turn out to be wishful thinking. Increasing prices for energy and essential goods, which are notoriously under-recorded in the broader CPI statistics, are emerging as the major concern. So far, few observers appear to accept that they are the inevitable consequence of earlier currency debasement. There is a growing risk that when consumers realise that rising prices are not just a short-term and temporary phenomenon, they will increasingly buy the goods they may need in the future instead of buying them when they are needed. This alters the relation between cash liquidity-to-hand and goods, increasing the prices of goods measured in the declining currency. And so long as consumers expect prices to continue to rise, it is a process that is bound to accelerate until it is widely understood by the currency’s users that in exchange for goods, they must dispose of it entirely. If that point is reached, the currency will have failed completely. It is this process that undermines the credibility of a fiat currency. Before it develops into a total rout, it can only be countered by an increase in interest rates sufficient to stop it, as well as by strictly limiting growth in the stock of currency. And even then, some form of convertibility into gold may be required to restore public trust. This, the only cure for fiat currency instability, is too radical for the establishment to contemplate, and is a crisis that increases until it is properly addressed. The rise in interest rates exposes all the malinvestments that have grown and persisted while interest rates were suppressed from the 1980s onwards, finally ending at the zero bound. The shock of widespread business failures due to rising interest rates will impact early in the currency’s decline when it becomes obvious that initial increases in interest rates will be followed by yet more. Importantly, the supply of essential goods is then further compromised by business failures instead of being alleviated by improving logistics. And consumer demand shifts even more in favour of the essentials in life and away from luxury and inessential spending. The poor are especially disadvantaged thereby and the middle classes begin to struggle. The private sector’s growing economic woes further undermine government finances. Unemployment increases and tax revenues collapse, adding to the budget deficit and therefore to the government’s funding requirements. Mandatory costs increase more than budgeted. Interest charges, currently about $400bn, add yet more to the deficit. Today, in all the major currencies control over interest rates by central banks is being challenged. Like the Fed, other major central banks are also insisting that rising prices are temporary, while markets are beginning to suspect the reality is otherwise. All empirical evidence and theories of money and credit scream at us that statist control over interest rates is being eroded and lost to market-driven outcomes. The consequences for markets and government funding costsThere is growing evidence that accelerating monetary expansion in recent years is feeding into a purchasing power crisis for major currencies. Covid and logistics disruptions, coupled with lack of inventories due to the widespread practice of just-in-time manufacturing processes have undoubtedly made the situation considerably worse. But in the history of accelerating inflations, there have always been unexpected economic developments. Shifting consumer priorities expose hitherto unforeseen weaknesses, so it would be a mistake to disassociate these problems from currency debasements.It is leading to a situation which confuses statist economists, who tend to think one-dimensionally about the relationships between prices and economic prospects. For them, rising prices are only a symptom of increasing demand. And so long as expansion of demand remains under control and is consistent with full employment, it is their policy objective. They do not appear to understand rising prices in a failing economy. But classical economics and on the ground conditions militate otherwise. Inflation is monetary in origin, and it is the destruction of the currency’s purchasing power that is evidenced in rising prices. And when the public sees prices of needed goods rising at an increased pace, they begin to rid themselves of the currency. And far from stimulating production and consumption, high rates of monetary inflation act as an economic burden. Monetary policy now faces the dual challenge of rising prices and rising interest rates as the economy slumps. When central banks would expect to reduce interest rates, they will now be forced to increase them. When deficit spending is deployed to stimulate the economy, it must now be curtailed Just when they matter most, bond yields will rise along their yield curves from the short end, and equity market values will be undermined by changing yield relationships. Falling financial asset values become a consequence of earlier monetary inflation undermining a currency’s purchasing power. The Fed, the Bank of England, the Bank of Japan, and the ECB have all acted together to accommodate government budget deficits, to be funded as cheaply as possible by suppressing interest rates. That they have acted together has so far concealed the consequences from bond markets, whose participants only compare one government bond market with another instead of valuing bond risks on their own merits. And through regulation, banks have been made to view investment in government bonds as being risk-free for counterparty purposes. All this is about to change with the turn in the interest rate trend. Monetary policy will have two basic options to weigh; between supporting the currency’s purchasing power by increasing interest rates, or to support financial markets by suppressing them. If the latter is deemed more important than the currency, it will most likely require more quantitative easing by the Fed, not less. Expressed another way, either central banks will pursue the current policy of maintaining domestic confidence and the wealth effect of elevated financial asset values and let the currency go hang. Alternatively, they can aim to support their currencies, and be prepared to preside over a collapse in financial asset values and accept the knock-on consequences. It is a dirty choice, with either policy option likely to fail in its objective. The end of the neo-Keynesian statist road, which started out lauding the merits of deficit spending is in sight. Mathematical economics and the state theory of money are about to be shown for what they are — intellectualised wishful thinking. As the most distributed currency, the dollar is likely to lead the way for all the others, slavishly followed by the Bank of England, the Bank of Japan, and the ECB. And all their high-spending governments, addicted to debt, will face unexpected funding difficulties.

[i] See rankred.com/how-much-money-is-there-in-the-world [ii] Reserve Bank of Australia, Banco Central do Brasil, the Danmarks Nationalbank, The bank of Korea, the Banco de Mexico, the Monetary Authority of Singapore and Sveriges Riksbank —all for up to $60bn each. [iii] See US Treasury TIC figures

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)