Send this article to a friend:

October

30

2020

|

Send this article to a friend: October |

|

The Fed Will Monetize All Of The Debt Issuance

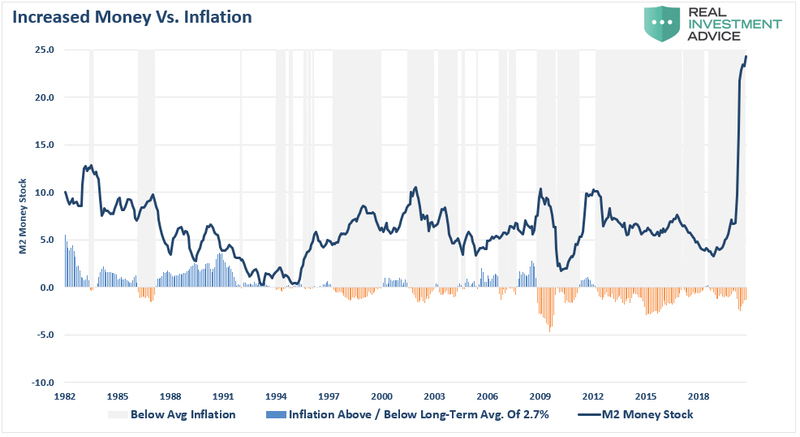

The Inflation Premise To fully explain why the Fed is now trapped, we must start with the inflation premise. The consensus expectation is the massive increases in monetary stimulus will spark inflationary pressures. Using the money supply as a proxy, we can compare the money supply changes to inflation.

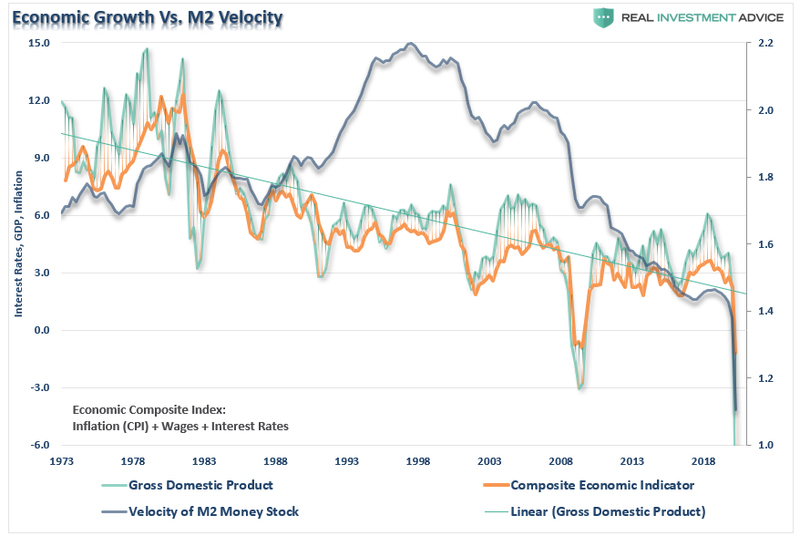

What we find is since 1980, increases in the money supply tend to precede periods of below-average inflation. Such tends to contradict the mainstream belief that increases in the money supply will lead to hyper-inflation due to the currency’s devaluation. Collapse Of Velocity Such has not been the case since 1990 as the byproduct of the money supply, known as “monetary velocity,” has been non-existent. As discussed previously:

The chart below shows the problem. Despite increases in the money supply, the “velocity of money” has plunged along with economic growth. The “economic composite,” which tracks GDP, comprises the components derived from “economic growth,” namely wages, inflation, and interest rates.

The question we must address is, “what happened in 1998” caused monetary velocity to collapse? Fed Has Crossed The Rubicon We often assume that “bad outcomes” happen overnight. Such is not the case. Whether it is the outbreak of war, an economic recession, or a “bear market,” there is always a long-period of events leading up to the crisis. As is often stated, “a crisis happens slowly, then all at once.” Such is the “trap” the Federal Reserve finds themselves in today. In 1980, the Federal Reserve became active in monetary policy, believing they could control economic growth and inflationary pressures. Decades of their monetary experiment have succeeded only in reducing economic growth and inflation and increasing economic inequality.

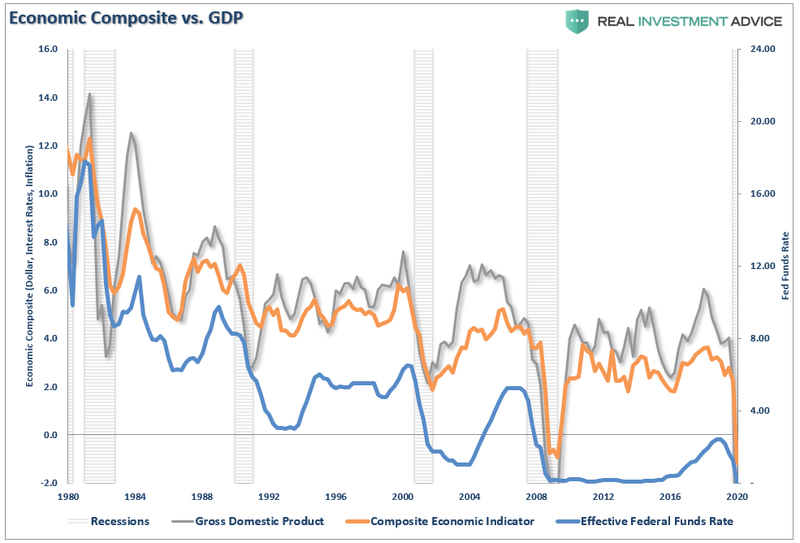

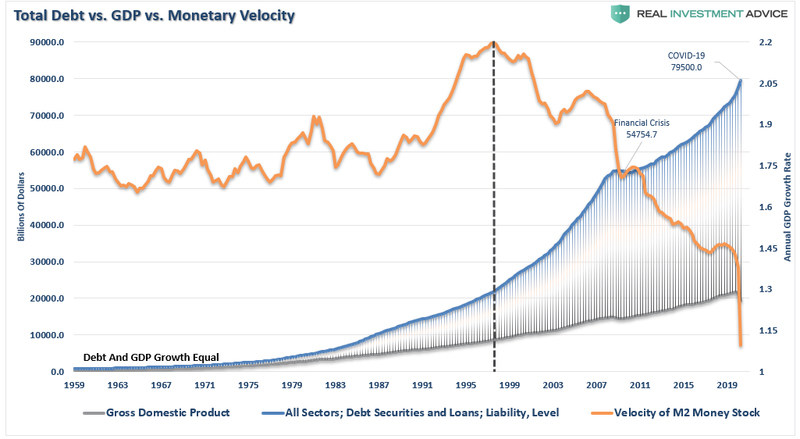

However, in 1998, the Federal Reserve “crossed the ‘Rubicon,’ whereby lowering interest rates failed to stimulate economic growth or inflation as the “debt burden” detracted from it. When compared to the total debt of the economy, monetary velocity shows the problem facing the Fed.

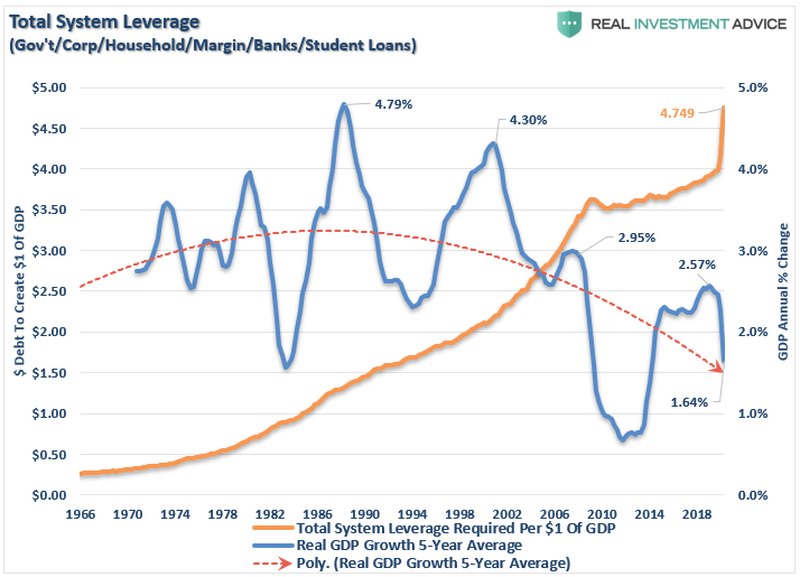

Look closely at the chart above. From 1950-1980 the economy grew at an annualized rate of 7.70%. The total credit market debt to GDP ratio was less than 150% to accomplish this growth rate. The CRITICAL factor to note is that economic growth was trending higher during this span, rising from roughly 5% to nearly 15%. There were a couple of reasons for this. Lower levels of debt allowed for personal savings to remain robust, fueling productive investment in the economy. Secondly, the economy focused primarily on production and manufacturing, which has a high multiplier effect on the economy. This growth feat also occurred in the face of steadily rising interest rates peaking with the economic expansion in 1980. How did the Federal Reserve get themselves into this trap?

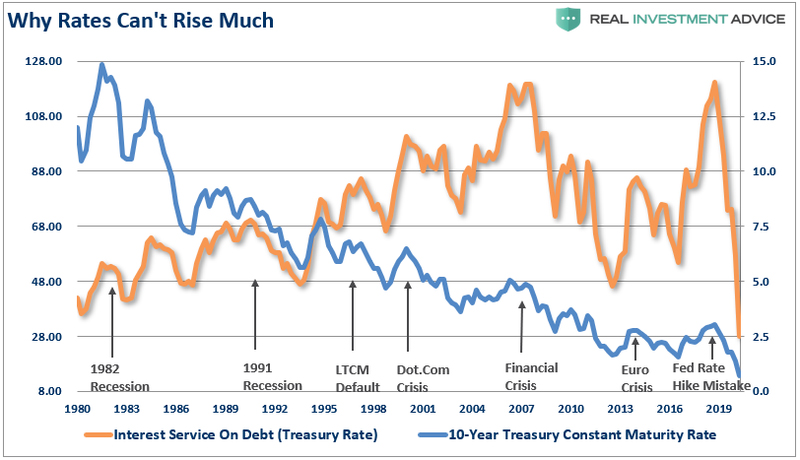

The Interest Rate Trap One of the biggest problems over the last decade is why interest rates don’t rise. While all of the “bond gurus” have had an annual prognostication of “the death of the bond bull market,” it has yet to occur. In an economy laden with $75 Trillion in total debt, higher interest rates have an immediate impact on consumption, which is 70% of economic growth. The chart below shows this to be the case, which is the interest service on total credit market debt. (The chart assumes all debt is equivalent to the 10-year Treasury, which is not the case.) Importantly, note that each time rates have risen substantially from previous lows, there has been a crisis, recession, or a bear market. Currently, with rates at historic lows, consumers are rushing out to buy houses and cars. However, if rates rise to between 1.5 and 2%, economic growth will quickly stall.

The Federal Reserve is well aware of the problem and why they have been quick to reduce rates and increase bond purchases. Such is because higher rates spread through the economy like a virus. The Rate Virus In an economy that requires $5 of debt to create $1 of economic growth, changes to interest rates have an immediate impact on consumption and growth.

I could go on, but you get the idea. The Liquidity Trap While the Federal Reserve keeps wanting higher inflation rates, which should correspond with economic growth, its policy actions continue to work to the contrary. In theory, their actions should lead to higher inflation as low rates spur consumption and investment. However, a signature characteristic of a “liquidity trap” is:

Pay particular attention to the last sentence. As discussed through the entirety of this article, every “check box” of a liquidity-trap has gotten filled:

Long-Term EvidenceGiven that higher rates of inflation would also correspond with higher interest rates, such will negatively impact virtually every aspect of the economy. As rates rise, so do rates on credit card payments, auto loans, business loans, capital expenditures, leases, etc., while reducing corporate profitability. In an economy supported by debt, rates must remain low. Therefore, the Federal Reserve has no choice but to monetize as much debt issuance as is needed to keep rates from substantially rising. Unfortunately, higher levels of debt continue to retard economic growth keeping the Fed trapped in a debt cycle as hopes of “growth” remain elusive. The current 5-year average inflation-adjusted growth rate is just 1.64%, a far cry from the 4.79% real growth rate in the ’80s.

Deflation Still Present The debt problem exposes the Fed’s risk and why they have no choice but to monetize the Government’s debt issuance to keep interest rates suppressed. More importantly, the decline in monetary velocity clearly shows that deflation is a persistent threat, and one the Fed is most afraid of. Treasury&Risk clearly explained the reasoning:

No Real Options The Federal Reserve has no real options unless they are willing to allow the system to reset painfully. Unfortunately, given we now have a decade of experience of watching monetary experiments only succeed in creating a massive “wealth gap,” maybe we should consider the alternative. Ultimately, the Federal Reserve, and the Administration, will have to face hard choices to extricate the economy from the current “liquidity trap.” However, history shows that political leadership never makes hard choices until those choices get forced upon them. While we continue to “hope” we can “grow” our way out of our debt problem, “hope” has never been a functional strategy for fixing problems.

|

Send this article to a friend:

|

|

|

There has been a rising concern as of late about surging inflation as the Government injects more stimulus into the economy. While it seems logical, the reality will be quite different as weak economic growth rates force the Fed to monetize the entirety of future debt issuances.

There has been a rising concern as of late about surging inflation as the Government injects more stimulus into the economy. While it seems logical, the reality will be quite different as weak economic growth rates force the Fed to monetize the entirety of future debt issuances.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)