Send this article to a friend:

October

03

2020

|

Send this article to a friend: October |

|

The Fed and the Housing Bubble/Bust

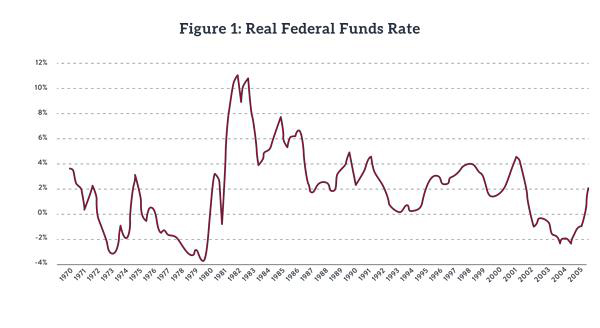

In chapter 8 we presented Ludwig von Mises’s circulation credit theory of the trade cycle, or what is nowadays referred to as Austrian business cycle theory. In the present chapter, we will apply the general theory to the specific case of the US housing bubble and bust, which began sometime in the early 2000s and culminated in the financial crisis in the fall of 2008. In a nutshell, the Austrian narrative recognizes the role that private sector miscreants can play in any particular historical boom but argues that these excesses were fueled by the easy money policy in the early 2000s enacted by then Fed chair Alan Greenspan. By flooding the market with cheap credit that came from the printing press rather than genuine saving, Greenspan pushed interest rates (including mortgage rates) down to artificially low levels. This caused (or at least exacerbated) the bubble in house prices and misallocated too many real resources to the housing sector. When the Fed got cold feet and began gently raising rates from mid-2004 onward, the bubble in house prices eventually tapered off and turned to a crash . The present chapter draws on material developed in three separate articles that the author wrote for Mises.org in response to critics who tried to exonerate the Federal Reserve from blame for the housing bubble.1 The chapter takes the standard Austrian theory for granted—as it was already explained back in chapter 8—and provides empirical support for the application of the theory to the historical case of the US housing bubble and bust. Link #1: Evidence That Changes in Interest Rates Affected Home PricesTo validate the Austrian explanation of the housing bubble, we must first establish that interest rates did indeed fall into unusually low territory during the boom phase, while they were hiked going into the bust. Figure 1 below shows the “real” (i.e., consumer price inflation–adjusted) federal funds rate, as a quarterly average from 1970–2006:

As Figure 1 indicates, the federal funds rate (which was the Fed’s target variable at this time), taking account of price inflation, was pushed down to negative 2 percent by early 2004. This was the lowest it had been going back to the late 1970s. Then interest rates began rising after 2004.

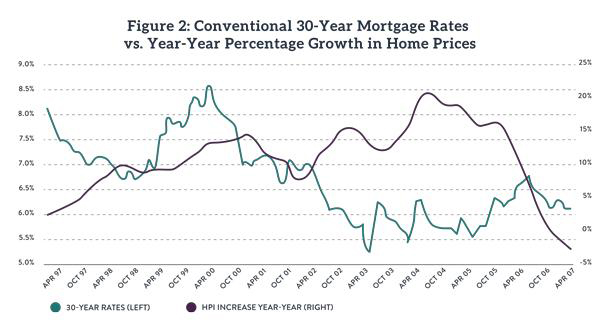

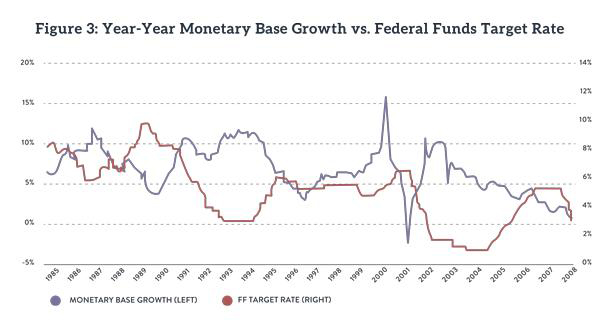

It wasn’t just short-term rates, but also mortgage rates, that fell during the peak years of the housing bubble. In Figure 2, we plot conventional thirty-year mortgage rates but also include year-over-year increases in the Case-Schiller Home Price Index (HPI). Taking figures 1 and 2 together, it is clear that interest rates—whether we look at the overnight fed funds rate or the thirty-year mortgage rate—really did fall significantly as the housing bubble accelerated. (It’s not shown in figure 2, but the trough for mortgage rates represented record-low rates going back at least through the 1970s.) Moreover, notice by comparing figures 1 and 2 that the bubbliest of the bubble years occurred when short-term rates were at their lowest, in 2004, and then home price appreciation began slowing as short rates were gradually hiked. To reiterate, this is perfectly consistent with the Austrian story of what happened. Link #2: Evidence That Monetary Inflation Affected the Level of Interest Rates In the previous section we established the fact that interest rates really did fall to historically low levels as the housing bubble intensified, while the cooling off of the boom went hand in hand with rising interest rates. However, some apologists for the Fed argue that Alan Greenspan had nothing to do this. Why, it was Asian saving that explains what happened with US interest rates during the 2000s. I have elsewhere directly rebutted the “Asian savings glut” explanation.2 for the details. However, in this chapter let us clearly establish that changes in the growth of the US monetary base went hand in hand with movements in the federal funds rate, just as any economics textbook would suggest. We provide this data in figure 3:

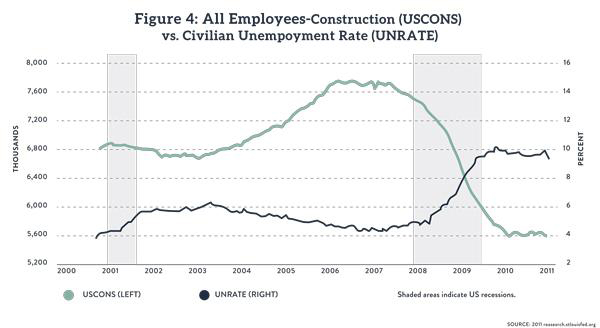

Look at how the two lines in figure 3 are (almost) mirror images of each other. Specifically, when monetary base growth is high, the federal funds rate is low. And vice versa, when the growth in the monetary base slows, the fed funds rate shoots up. There is nothing mysterious about this. To repeat, this is the standard explanation given in economics textbooks—not just Austrian texts—to explain how a central bank “sets” interest rates. When the central bank wants to cut rates, it buys more assets and floods the market with more base money. And when the central bank wants to raise rates, it slows the pace of monetary inflation (or even reverses course entirely and shrinks the monetary base). Recall from chapter 5 that the “monetary base” consists of paper currency and member banks’ deposits at the Fed. Therefore, the Federal Reserve has absolute control over the monetary base; those rascally Asians who have the gall to live below their means can’t directly increase the US monetary base. As figure 3 shows, when US interest rates fell sharply in the early 2000s, this occurred during a period of rapid growth in the monetary base. If the Fed didn’t want interest rates falling so low in the early 2000s, it shouldn’t have engaged in so much monetary inflation. Link #3: Evidence That the Housing Bubble Led to “Real” Problems in the Labor Market Last, there are some economists—such as Scott Sumner, whose views on NGDP targeting we critique in chapter 15—who argue that the Austrians are wrong for thinking that the housing bubble had anything to do with the Great Recession. (See the articles in endnote 1 for more details on Sumner’s perspective.) In this last section, we provide two additional charts to show that the Austrian explanation holds up just fine in this regard. First, in figure 4 we plot total construction employment against the civilian unemployment rate:

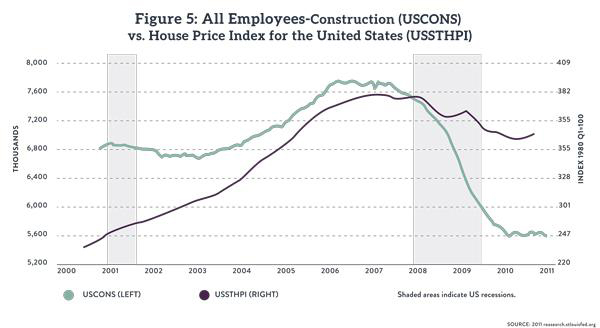

As with the previous charts, this one too is exactly the kind of picture Austrians would expect to see. Total construction employment surged from about 6.7 million in 2003 up to 7.7 million by 2006, but then began falling fast in mid-2007. This movement in construction employment was the mirror image of the national unemployment rate, which dropped from some 6 percent in 2003 to the low 4s in early 2007. After that, it began rising sharply, mirroring the crash in construction employment, hitting 10 percent in mid-2009. Finally, let us plot the movement in total construction employment against an index of home prices:

As the chart makes clear, the movement in total construction employment seems intimately related to the bubble in house prices. They both rose together from 2003, they both tapered off going into 2007, and they both began plummeting going into 2008. Conclusion In this chapter, we have applied the generic Austrian theory of the business cycle to the specific case of the US housing bubble and the ensuing financial crisis/Great Recession. Specifically, we showed that interest rates—including not just short-term rates but also thirty-year mortgage rates—fell to historically low levels just as the housing bubble accelerated into high gear. We then showed that the fall and rise in interest rates corresponded with an increase and slowdown in the Fed’s monetary inflation, just as any econ textbook would suggest. Finally, we showed that the movement in home prices behaved as would be expected with respect to total construction employment and that this in turn tied up in the obvious way with the national unemployment rate. We have thus shown empirical evidence for each crucial link in the standard Austrian story of how “easy money” can fuel an unsustainable boom, which leads to an inevitable bust. In closing, we should note that the Austrians didn’t merely explain the Fed’s role in the housing crash after the fact. On the contrary, in September 2003—five years before the financial crisis—Ron Paul testified before the House Financial Services Committee,3 arguing that federal subsidies to housing, through such entities as Fannie Mae and Freddie Mac, were merely setting the country up for a housing crash. He also mentioned that the Fed’s inflation would merely postpone the day of reckoning and make it that much more painful. In the following year, 2004, Mark Thornton wrote a prescient article for Mises.org entitled “Housing: Too Good to Be True,”4 in which he warned:

Because Austrians tend to downplay the ability of economics to provide numerical predictions, its critics often mock the school as unscientific and useless for the investor. But the experience of the US housing bubble and bust shows that the Austrians, armed with Mises’s theory of the business cycle, gave far better guidance than, say, Ben Bernanke.

Robert P. Murphy is a Senior Fellow with the Mises Institute. He is the author of many books. His latest is Contra Krugman: Smashing the Errors of America's Most Famous Keynesian. His other works include Chaos Theory, Lessons for the Young Economist, and Choice: Cooperation, Enterprise, and Human Action(Independent Institute, 2015) which is a modern distillation of the essentials of Mises's thought for the layperson. Murphy is cohost, with Tom Woods, of the popular podcast Contra Krugman, which is a weekly refutation of Paul Krugman's New York Times column. He is also host of The Bob Murphy Show.

|

Send this article to a friend:

|

|

|

[This article is part of the

[This article is part of the

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)