Send this article to a friend:

October

23

2019

|

Send this article to a friend: October |

|

Quick Recap of the Fed’s Foundering Follies and Our Descent

And, then, all of that pumping of of new fiat money into the monetary system was still not enough, so the overnight and term repos (essentially loans) had to continue. Then, because all of those operations together are still not enough, the Fed promised the repos will continue, “at least,” through January, 2020, and the creation of new money injected into the banks will continue, “at least,” into April. But there is no problem here, and the Fed assures us none of this is QE, even though the aggregate of all of that is easily as big as any previous rounds of QE. By the end of the Fed’s already slated actions, it is estimated the Fed will have injected, at least, $850 billion dollars into the economy! In all, a tremendous amount of churn out the flood gates in just one month as the Fed opened its unlimited reservoir to pour a river of money into the banks and economy to save the rich. It leapt back into doing that so quickly it couldn’t even wait until its regularly scheduled October meeting to make a studied decision. The immediacy says this was clearly an emergency, reactionary decision. But that is not QE4ever! Not according to the Fed. You see, it cannot be called QE because a return to QE would be admission of catastrophic economic failure precipitating from of the Fed’s quantitative tightening regime, which I labeled “The Fed’s Great Recovery Rewind,” having seen where it would take us before any of the above madness and mayhem. It also cannot be called QE because, as pointed out in my latest QE4ever article, that would be illegal since QE forever is the same thing as monetizing the national debt, expressly forbade by congress. How it all came down The fix is in, and exactly in the manner I have stated for years it would happen. (I’m not suggesting I’m the only one to see how this would play out, as others also saw by similarly conceived routes the USS Fed was headed for the rocks long ago.) Here is the course I laid out by which the ship would hit the rocks:

In other words, we’ll be far down the road of economic collapse before the Fed gets that all figured out. Powell, himself has said,

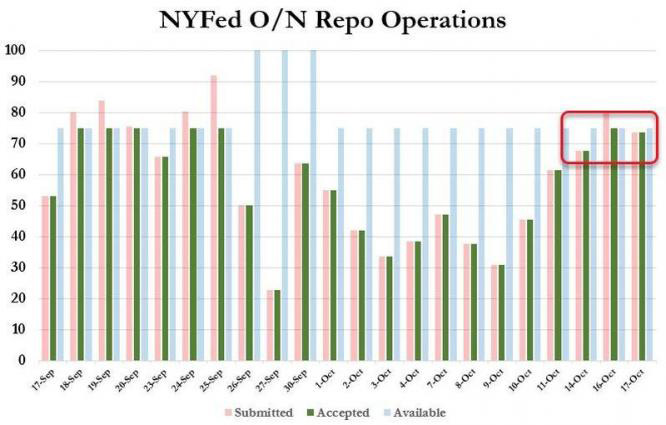

Since the Fed’s data, itself, almost always lags any changes in the actual economy by, at least, a month, and since the Fed is still saying all of its changes will be data dependent, and since the Fed says its policy changes have a “long and variable” lag before they start to change the actual economy, it will be a long time before the Fed knows how effective any of its present actions are. Only at that point will the Fed be leaping in with the solution it should have deployed immediately when its recovery started to fail (if it wanted to temporarily prop the economy up again via its familiar means). Right now we are at step #5. Never was there any chance the Fed’s recovery plan would lead to anything lasting. The latest signs of continued descent into recessionHere is the situation as the Fed now starts the non-QE of step #5, which is actually going to become QE4ever because the Fed has no exit plan, and all economic matters are still turning worse: Repo operations have continued unabated:

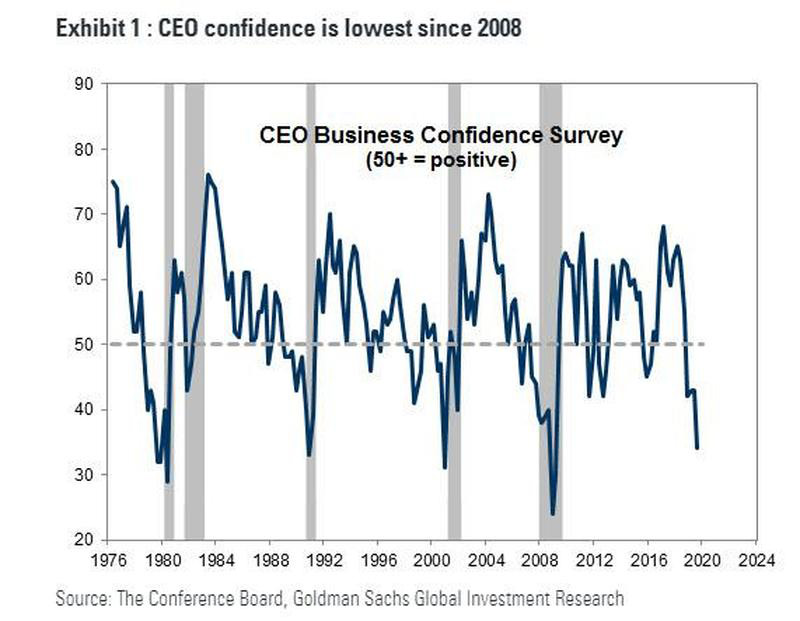

Retail sales and industry decline: September’s retail sales fell 0.3% month on month. That was not just brick-and-mortar. Online sales, as a part of that, also declined 0.1%. Business inventories have been slowly but steadily building since 2017, which gradually suppresses wholesale purchases from manufacturers then backs up to production decreases. Not too surprisingly, then, industrial production fell 0.4% month on month in September, double the amount that was anticipated by economists. CEO confidence falls precipitously:

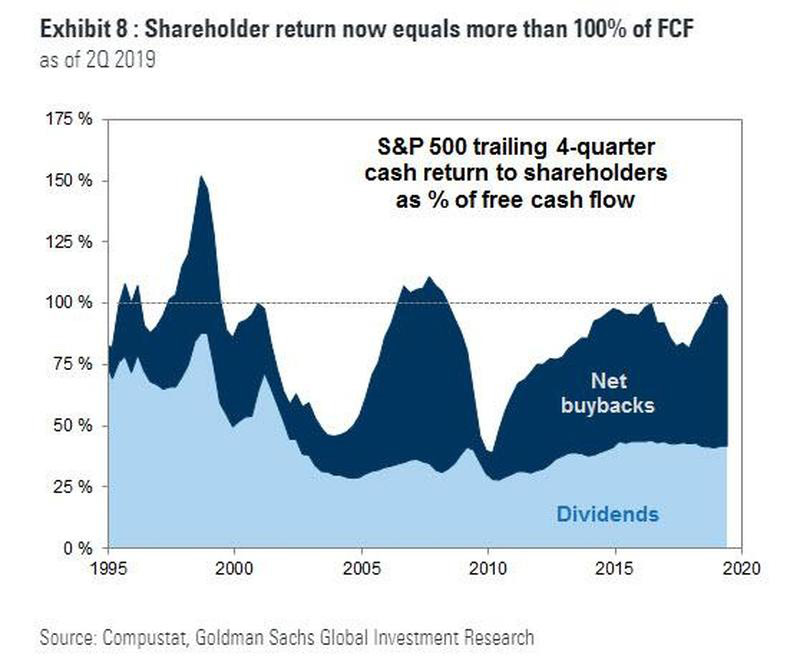

Who knows better than CEOs whether they have anything to be confident about? Sure, market traders claimed last week that corporations were doing well on earnings because traders have their books to sell. It’s a simple and deceptive as that. They could only claim earnings were fine, however, because, as has happened every quarter this year, earnings expectations were lowered even more than they had been lowered in previous quarters. That leaves one to wonder if buybacks have soared to record levels again because CEOs and corporate board members are using corporate cash to buy themselves out as quickly as possible:

The housing decline declines again: I had last noted in a previous article that housing was the only economic indicator that had moved out of sync with my recession predictions. The rest were aligning in lockstep. Well, August’s upward spike turned out the next week to be a mere blip as the downward path has resumed:

Housing starts fell 9.4% in September month on month, but that was still 1.6% above September, 2018. Housing completions, however, fell 9.7% in September, month on month, and were dropped 1% below September, 2018. Those are just the indicators that have shifted since my earlier October article, “The Relentless Road to Recession.” GDP pushing recession under heavy trade suppressionNotice how close we came to recession in the fourth quarter of last year, as reported in January of 2019, and notice how rapidly the fourth quarter plunged from the third: source: tradingeconomics.com The same rapid plunge could happen in the third quarter of this year, which will be reported October 29, and we still have one quarter to go in the year with not a lot of reasons in all the stats I’ve been showing throughout the third quarter to believe things have any chance of heading up. Even the partial trade deal that is presently in the works — which won’t be signed until, at earliest and if at all, the middle of November — only locks in place the tariffs that already exist. It is nothing more than an agreement to stop escalating tariffs. Again, it is not an agreement to back the trade war down, but merely to stop escalation that is already scheduled for December. Therefore, it won’t bring any relief to the above picture of declining GDP, except in pork and soybean sales. In fact, the International Monetary Fund estimated its effect this way, saying it …

In other words, without the deal, global GDP growth is expected to fall another 0.8%. With it, damage will by slightly mitigated to where global growth will only fall another 0.6% due to trade wars. The US is impacted more directly by the trade war with China than the rest of the world, so larger declines in either case should be expected. That means you can knock, at minimum, another 0.6% off the above US GDP growth chart in the months ahead just from the continuing US trade wars, and that is the best-case scenario if this agreement gets signed in November. I think this no-deal trade deal has a better chance of being signed than any past promises; but it is still a deal without hope. Trump may be feeling some desperation to mitigate economic damages as we go into the election year, and Krazy Kudlow is telling him he needs to sign:

But it’s still a nothing deal that merely keeps trade from worsening. Meanwhile, new tariffs just went into place last week between Europe and the US, and trade with China will continue to worsen from tariffs already in place that are still working their way down the long Silk Road to the consumer. With recession advancing relentlessly now from every quarter and the central bank’s recovery broken on the rocks and floating away like flotsam in the ebbing tide, I continue looking deeper into the ongoing words of all central bankers regarding their joint efforts to create a vast, global solution to a now fully global and growing problem in my next Patron Post. It’s not too late to sign up to get access to this ongoing saga of the central banksters’ big plans in their own words, which has been my theme throughout 2019. Liked it? Take a second to support David Haggith on Patreon!

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](../09.19/images/t24_ag_en_usoz_2.jpg)