Send this article to a friend:

October

15

2019

|

Send this article to a friend: October |

|

Fed QE Not QE Starts at $80 Billion Monthly, Plus TOMO-

The Fed made this shocking announcement today. Fed QE to Total $80 Billion Per Month To StartEmphasis added to highligh key points.

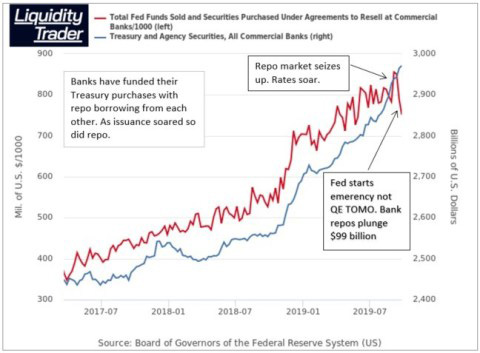

The System is Out of Cash – We Saw It ComingThe financial system has run out of cash. It cannot absorb the humongous pile of paper that the Federal government is issuing every month to fund the massive budget deficit. Without the Fed absorbing the bulk of this paper, interest rates would be going through the roof. We have known for many months that this was coming, as the banks funded virtually all of their Treasury purchases with repo borrowing since 2017. Treasury issuance soared as the budget deficit grew. Dealers and their parent and client banks bought more and more. Repo borrowing soared.

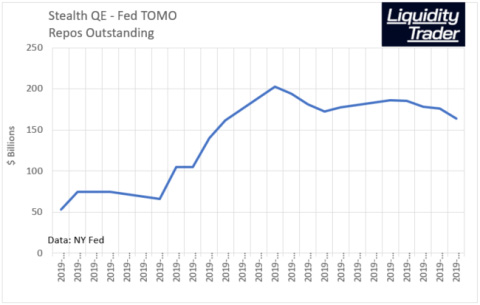

That reached a limit in mid-September. Banks and dealers could no longer borrow repo funds within the Fed’s Fed Funds target range. Private market repo rates soared, so the Fed had to take emergency measures. New Fed QE Started with TOMO The New Fed QE started with Temporary Open Market Operations (TOMO). Those operations initially consisted of overnight repos. These are direct loans to Primary Dealers. The Fed quickly made it clear that it would roll those over as long as necessary. It also added a series of 14 day term repos. On September 30, the total outstanding reached a mind boggling $205 billion. That has dropped back to $164 billion today. That’s because the market is between the huge Treasury coupon settlements which take place around the end of the month, and then again around the 15th.

They Said It Was a One-Off LOL Fedheads, clueless economists, and the craven Wall Street media all made the idiotic excuse that the repo market problems were due to the “one-off” event of corporations needing to withdraw cash from the banks to pay their September 15 quarterly tax obligations at the same time as the Treasury was issuing a large amount of new paper. How the hell can they have the gall to call it a one-off? IT HAPPENS EVERY QUARTER! The Treasury issued $43 billion in net new paper between September 10 and September 17. Compare that with the March quarterly corporate tax period (June doesn’t count because the debt ceiling restricted issuance). Net new issuance in the March tax week was $90 billion! Why didn’t that cause the repo market to seize up? The Banking System Hit the Wall- New Fed QE to the Rescue Because the repo market hadn’t hit the wall yet. Now it has. That’s why the Fed had to intervene, and will need to continue to intervene and buy up most new issuance from now till Kingdom Come. So get ready to see the Lord, folks. But none of us knows what he or she looks like. I suspect there will be plenty of fire and brimstone as we face a reckoning between Fed printing and a market that’s suddenly running away from holding bonds. The Treasury will issue $69 billion in net new paper next week. With the new POMO operations only just beginning to help absorb that, watch for a massive surge in TOMO. That should recede as the new POMO operations get in full swing. TOMO Too Little, Here Comes POMO The Fed knew that it could not support the constant flow of new Treasury issuance by TOMO alone. So here comes the new Fed QE. First TOMO, now massive POMO – Permanent Open Market Operations. It’s QE, regardless of what they call it. With TOMO repos, the Fed merely lends the money to the dealers to buy up the Treasury supply constantly hitting the market. With POMO, the Fed purchases Treasuries directly from Primary Dealers, cashing them out each week. The Dealers can then buy new Treasury issuance in the following weeks, as required. This is exactly what the Fed did with old QE. However, DO NOT CALL THIS QE! Because… Well, just because Jerry, and his cadre of media talking heads, said so. Where Have You Gone Alan Abelson? I understand the Fedheads doing this. It’s propaganda for the masses. But from the fin-journo community, parroting this crap is inexcusable. It’s just another sign that there are no journalists covering Wall Street. Guys who once did, like Pedro da Costa have been drummed out of the business. The Wall Street Journal and CNBC are wholly owned propaganda subsidiaries of the Street. Where have you gone Alan Abelson? Where’s John Crudele? Floyd Norris? Haven’t heard much from Gretchen Morgensen lately. Those who might stir the pot a little dare not. They know which side their bread is buttered on. Regardless Of What They Call It, It Still Quacks Like A Duck But here’s the point. Just because the reason for the QE is different, doesn’t mean that it’s not QE. Whether the purpose is ostensibly “reserve management” as they say now, or to support economic growth, POMO is POMO. And this TOMO and POMO means massive expansion of the Fed balance sheet. And massive expansion of the Fed balance sheet is QE. POMO purchases of Treasuries from dealers pump money directly into Primary Dealer accounts. To the extent that they do not need to buy Treasuries, they direct the excess cash to purchase other financial assets, usually stocks. That’s why Old QE was so bullish. Here’s Why This Time is Different But this time IS different. During Old QE, Federal debt issuance was falling. The dowtrend began in 2010 and continued until 2016. The system was awash in cash. Under New QE, Federal debt issuance is high and rising. There’s no end to that in sight. Under old QE, declining issuance was working in the Fed’s favor. And the market was enamored of bonds. With investors and foreign central banks buying Treasuries heavily, the dealers did not need to be as active in buying and accumulating Treasuries. So they bought stocks. None of that is the case today. Now the Fed is fighting against increasing issuance and a banking system that has run out of cash. Dealers are stuffed to the gills with massive Treasury positions. They’re choking on the stuff. Watch the Treasury Yields for A Crash Signal Just look at soaring Treasury yields over the past few days. The Street is trying to divert your attention to the fact that the monthly 30 year bond offering was at a record low. Meanwhile, the 30 year bond yield has risen from 2.01 to 2.21 over the past 5 days. But nobody is talking about that. The 10 year yield has run up from 1.50 to 1.75. The 10 year note issue auctioned this week is already 13 bp under water. Dealers who bought that issue are choking on it. The 30s are also slightly under water. Nobody’s talking about that. Dealers, banks, and huge leveraged hedged funds are financing their purchases entirely with overnight repo. So they have a problem! They must put up collateral every night. The collateral will soon not cover the loan, if it doesn’t already. Collateral (margin) calls will only bring forth more selling. That is how crashes start. If this spike in bond yields and plunge in prices isn’t stopped in its tracks right here, the financial markets will be in a world of hurt as soon as next week. With dealer and bank Treasury holdings leveraged to the hilt, they cannot afford prices to fall at all. That’s what caused the money market to seize up in the first place. And it’s on the verge of happening again, even with the Fed pumping all this cash into the system. It All Points to One Thing- The House Is on Fire The Fed has pulled out all the stops. It already pumped $205 billion in TOMO into the system in a couple of weeks. Now it will add another $60 billion per month in POMO to the $20 billion in POMO it is already doing. And they promise that this will go on for months. This level of pumping is a sign that the House — Wall Street — is on fire. And it will get worse if the economy weakens. Time will tell on that score. Meanwhile, the Fed’s contraspeak propaganda notwithstanding, this is QE. We just don’t know if it will work this time. I have my doubts. Liquidity Trader readers had the benefit of knowing that the rising tide of Treasury issuance would cause interest rates to rise, and that the Fed would need to restart QE as a result. We stay ahead of the curve by paying attention to the details that matter. Join us today! First Month Free and 90 Days Risk Free If You Join Now!Read Lee Adler’s Liquidity Trader risk free for 90 days! Satisfaction guaranteed or your money back. Subscribe by 3:00 PM ET Friday, October 11, and get the first month free! Free first month, and 90 day risk free trial offer is for first time subscribers only. Quarterly billing will begin on the 31st day of your subscription unless you cancel before that date.

I’ve been publishing The Wall Street Examiner and its predecessor since October 2000. I also provide analysis and charts for David Stockman's Contra Corner which I developed for Mr. Stockman. I’ve had a wide variety of finance related jobs in the past 44 years, including a stint on Wall Street in both analytical and sales capacities. Prior to starting the Wall Street Examiner I worked as a commercial real estate appraiser in Florida for 15 years. I also worked in the residential mortgage and real estate businesses in parts of the 1970s and 80s. I have been charting stocks and markets and doing analytical work since I was a teenager. My perspective is not of the Ivory Tower. It is from having my boots on the ground and in the trenches of the industries that I analyze and write about today.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](../09.19/images/t24_ag_en_usoz_2.jpg)