Send this article to a friend:

October

03

2018

|

Send this article to a friend: October |

|

Are We Insured?

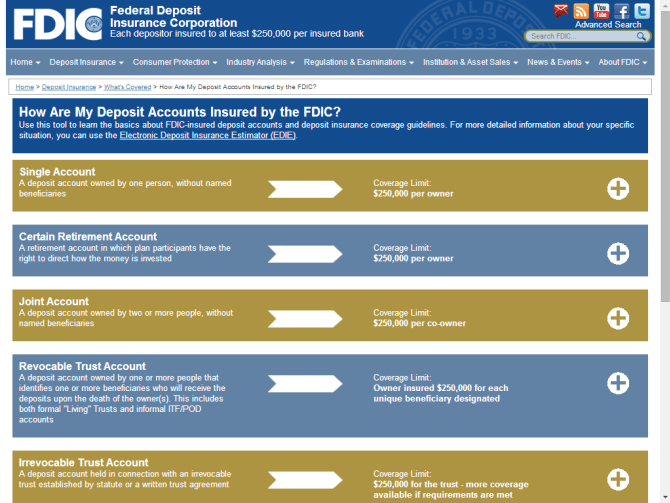

Is your bank account ‘F.D.I.C.’ (Federal Deposit Insurance Corporation) Insured? Ah, the piece of mind knowing that your account is protected up to $250,000 in the event of a bank default? WARNING: A Sophism is a lie that has been told over and over until you accept it as truth. *Note: Safety Deposit Boxes are NOT insured*. https://www.fdic.gov/deposit/covered/categories.html

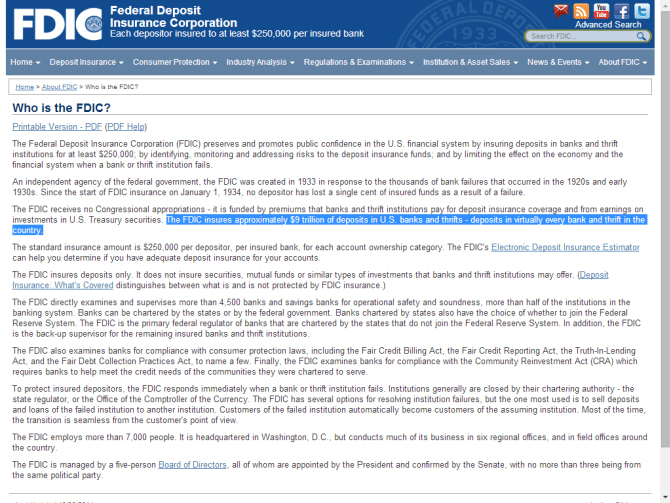

Fact: The FDIC insures approximately $9 trillion of deposits in U.S. banks and thrifts – deposits in virtually every bank and thrift in the country. https://www.fdic.gov/about/learn/symbol/

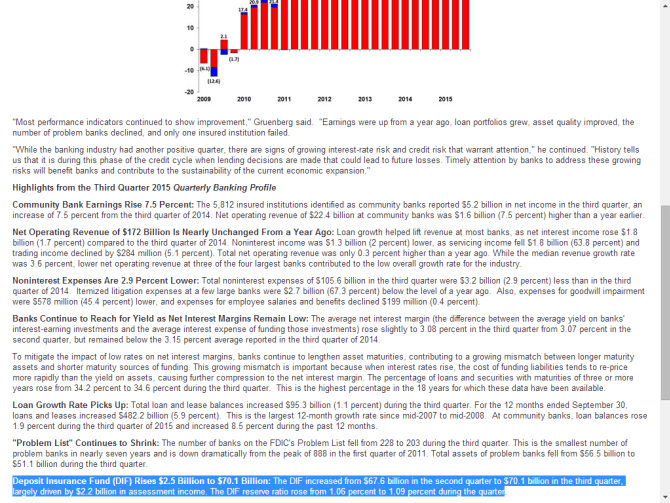

Fact: The FDIC has a fund account called the Deposit Insurance Fund (DIF) which is to insure $9 Trillion in deposits, currently at a ratio of 1.09. “Deposit Insurance Fund DIF Rises $2.5 Billion to $70.1 Billion:The DIF increased from $67.6 billion in the second quarter to $70.1 billion in the third quarter, largely driven by $2.2 billion in assessment income. The DIF reserve ratio rose from 1.06 percent to 1.09 percent during the quarter”. *The Reserve Ratio is known as Fractional Reserve Banking* https://www.fdic.gov/news/news/press/2015/pr15092.html

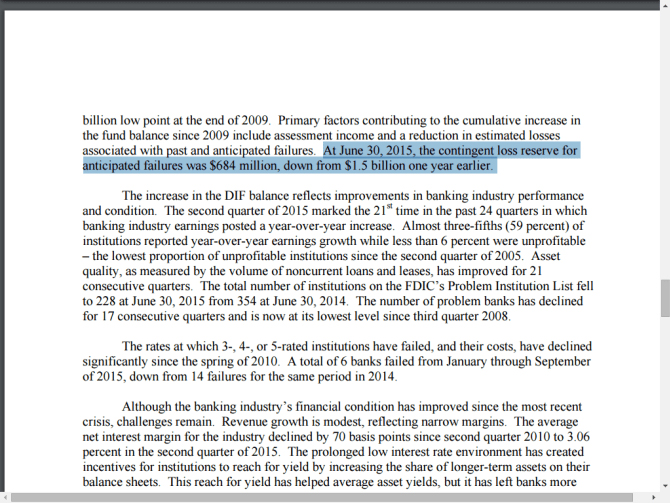

Fact: In the event the $70.1 billion can’t cover the $9 Trillion in deposits there are emergency funds. “At June 30, 2015, the contingent loss reserve for anticipated failures was $684 million, down from $1.5 billion one year earlier”. https://www.fdic.gov/news/board/2015/2015-10-22_notice_sum_b_mem.pdf (Page 5 of 7)

Fact: In the event the $70.1 Billion from the ‘DIF’ and the $684 Million in the Contingent Loss Reserve of the FDIC are all exhausted to cover the $9 Trillion, the Financial Stability Oversight Council would intervene. The Financial Stability Oversight Council would intervene and auction, pledge, and or assign the assets of the defaulting banks, which is 15.9 Trillion. The question one has to ask is how long will it take to convey from the Grantor (Seller) to the Grantee (Receiver)? https://www.treasury.gov/initiatives/fsoc/about/Pages/FSOC-Member-Agencies.aspx

https://www5.fdic.gov/idasp/index.asp

Which leads the reader to consider Captial Controls, which places a restriction on the amount you can withdrawal monthly from the bank irrespective of your financial obligations or tenure with your bank.

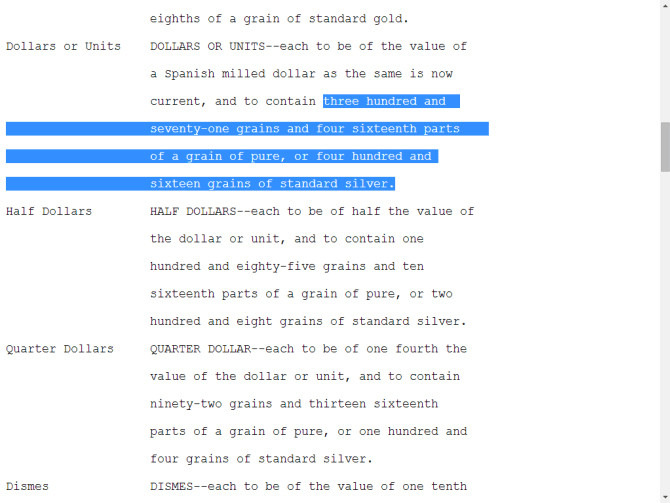

If you elect to call the FDIC (877.275.3342) or the U.S. Treasury (202.622.2000) do inquire about the definition of a dollar. Per the 1792 Coinage Act is 371.25 Grains of Silver. Which has never been repealed, and is still edict, law! http://www.constitution.org/uslaw/coinage1792.txt

What can you do?

* Note: The purpose of insurance is to make a person whole after their loss. I engaged in the following dialog more than once between different representatives for the FDIC to construct this blog. This is in no way to insult their intelligence, nor is this an attempt to ridicule them. In their defense, they were professional and attempted their very best to address all of my concerns. However, I caution and ask you to do your own independent research. Copy and paste the URL’s provided and ask the questions I inquired with the representatives (see narrative below). The purpose of this article is to enable the reader to think critically and independently. Most important to question and refute a sophism. Me: Can you confirm that the FDIC insures bank accounts up to $250,000? FDIC: That is correct. Me: Can you please define a dollar? FDIC: The Treasury determines what defines a dollar. Me: Actually, that is incorrect. The ‘1792 Coinage Act’ defines a dollar as 371.25 grains of Silver, which is .77344 of a troy ounce. FDIC: Silent Me: How can the ‘FDIC’ insure 250,000 units of something when it cannot provide the definition of 1 unit? FDIC: That is something you will have to ask the Treasury and Federal Reserve, and the Bureau of Engraving and Printing. Me: 1792 Coinage has never been repealed. So if I deposit 250,000 Morgan Dollars, which is the definition of dollar, into my account are they insured? And I am not referring to Safety Deposit box because that is not ‘FDIC’ insured. FDIC: No sir, the banks hold paper money. Me: Money is physical Gold, physical Silver per ‘Article 1 Section 10 of the Constitution’. Furthermore, the composition of a ‘Federal Reserve Note’ is 75% Cotton and 25% linen, so it’s not paper. Are you not aware that the Bureau of Engraving and Printing’ cannot print the word money on the obverse or reverse of the note because it will make it Unconstitutional per Article 1 Sec 10? FDIC: Sir, that is not in my scope of practice you will have to call the Treasury. Me: Out of curiosity how often do you receive calls such as mine? FDIC: Sir, I in all the years I have worked here I have never received a call such as yours. (Second Conversation: FDIC noted about once a week). Me: As a citizen, I am truly concerned that I can articulate the above and took the initiative to correspond with you (FDIC) as a concerned citizen and yet calls such as mine do not take place. Sir, the saddest part is that I was not born a U.S. citizen. I thank you for your time. In producing this article, I had this exact narrative with more than one representative from the FDIC. Please share your responses in the comments section below. If you found this article to be beneficial please share with your friends and family. We encourage and invite you to join us by subscribing to our blog. We are committed to providing factual articles that will make you think critically and independently. Proven & Probable With Regards, I am, Maurice Jackson The featured image was made possible because of: Joshua Holden – Liberty.me

| ||||||||||||

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)