Send this article to a friend:

October

23

2018

|

Send this article to a friend: October |

|

Mining Stocks Have Not Been Cheaper In The Last 78 Years

In relation to the price of gold and silver, the mining stocks generically (i.e. the various mining stock indices like the HUI or GDX) have rarely traded at cheaper levels than where they are trading now:

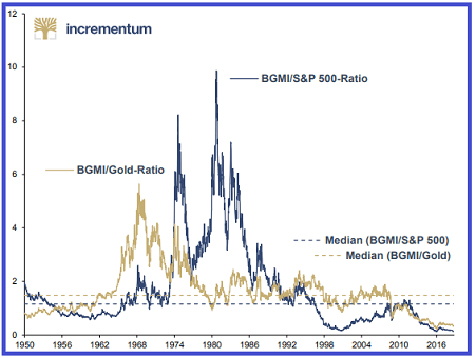

The chart above, sourced from Incrementum (the October 2018 chartbook update to the “In Gold We Trust” 2018 report), shows the ratio of Barron’s Gold Mining Stock Index (BGMI) to the price of gold (gold line) and the S&P 500 (blue line) going back to 1950. As you can see, gold mining stocks are trading at their lowest level relative to gold and the broad stock market in 78 years. The two dotted lines show the median level for each ratio since 1950. As you can see, mining stocks do not spend much time below the median ratio. I strongly believe that the chart reflects a high probability of a major move higher in precious metals and mining stocks that is percolating, if not imminent. Certainly the global economic, financial and geo-political risk fundamentals support this assertion. Unless the precious metals mining business is going away, that chart implies that now is one of the best times since World War Two to buy mining shares. Not surprisingly, industry insiders must agree with that assertion, as mining stock acquisition deal-flow has picked up considerably in the last few months. Most of the deals have been concentrated in the junior mining stocks. But Barrick’s acquisition of Randgold, announced September 24th, is the largest precious metals merger in history. I strongly believe Barrick bought Randgold out of desperation to replace its rapidly depleting gold reserves. Fundamentals aside, I believe gold is technically set-up to make a big move:

The chart above shows GLD (used a proxy for the price of gold) from late 2004 to the present on a weekly basis. I’ve sketched a trendline that goes back to 2004. 2004 is when gold finally pushed through $400 for good. It was right before that event that Robert Prechter, of Elliot Wave fame, predicted that gold would fall to $50. While I’m not a big fan of analysis based on lines drawn on charts, this particular tend-line has held intact since gold bottomed in December 2015. Notwithstanding chart analysis, the COT technicals have never been more bullish. This assertion assumes, of course, that the track record of hedge funds being wrong when positioned long or short at an extreme level remains intact.

investmentresearchdynamics.com

|

Send this article to a friend:

|

|

|

It’s important to keep in mind that the mining stocks have been sold to levels well-below their intrinsic value – in the case of larger-cap producing miners. Or their “optionality” value – in the case of junior mining companies with projects that have a good chance eventually of converting their deposits into mines. “Optionality” value is based on the idea that junior exploration companies with projects that have strong mineralization or a compliant resource have an implied value based on the varying degrees of probability that their projects will eventually be developed into a producing mine.

It’s important to keep in mind that the mining stocks have been sold to levels well-below their intrinsic value – in the case of larger-cap producing miners. Or their “optionality” value – in the case of junior mining companies with projects that have a good chance eventually of converting their deposits into mines. “Optionality” value is based on the idea that junior exploration companies with projects that have strong mineralization or a compliant resource have an implied value based on the varying degrees of probability that their projects will eventually be developed into a producing mine.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)