Send this article to a friend:

September

12

2023

|

Send this article to a friend: September |

|

Mountains and Mountains of Debt Are Crashing

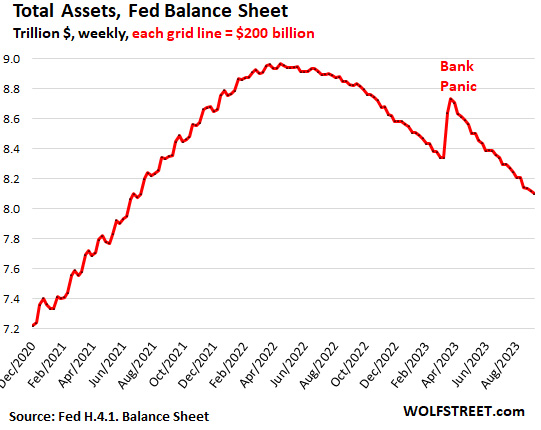

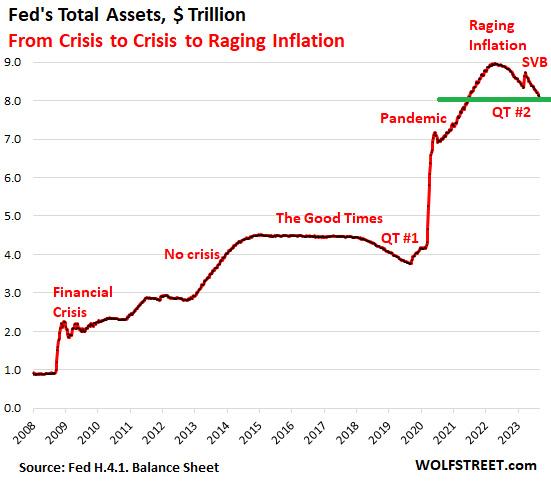

Defaults on loans with banks that are not in the top-100 for size have already risen to the highest record ever! Even if the Fed stops hiking interest rates (which is unlikely with recent hints that inflation may be back on the rise), the Fed still plans to continue quantitative tightening (QT) for a long time, just as it believed it could do in 2019 … and failed at spectacularly. You don’t hear anyone in the mainstream financial media talking about that as they all act like the only kind of Fed tightening that matters is interest hikes. Those will end and the problems are over (they pretend). We can see how far the Fed has gotten with its balance-sheet reduction and how far it has to go here: Oops. My mistake. That’s just unwinding the expansion of its balance sheet that happened in the slow part of the Covid years. It completely misses the absolute wall of quantitative easing (QE) the Fed piled up in the first year of Covid (2020). Here’s the full picture, going all the way back to the Fed’s start of experimental QE:

The Fed originally said it planned to unwind most of that balance-sheet expansion that the Fed forced into the nation’s money supply at its roots since the Great Recession. You can see how far the Fed got when it tried to take the first pile-up of monetary expansion down from 2018 to the end of summer in 2019 at a more gradual rate than the present. It suddenly had to ramp up money supply to try to stop the huge crisis it created in interbank lending called the “Repo Crisis” or “Repocalypse.” Next, you can also see how far it got when it attempted to reduce its wall of QE, which it has said was just temporary help, back in early 2020. It managed a mere blip downward before the Fed promised and immediately delivered repetitive doses of more QE with the government’s help in distributing it. Back in 2019, the Fed’s efforts to recover from the Repocalypse kept becoming more extreme in larger and larger amounts of low-interest overnight loans to banks that proved to be anything but overnight in that the Fed had to endlessly roll them over and increase them to try to keep interbank lending from collapsing entirely. I stated from the first week of that crisis they would never be “overnight loans” for that reason, and that it would have to replace the bonds it had rolled off its balance sheet under that first and failing bout of QT. It turned out that the Fed’s overnight loans did, indeed, get bigger and higher as it piled money back into its balance sheet without resolving the problem at all. Then Covid -19 hit in 2020, and effectively gave the Fed permission to give up any pretense that it would go back to QT. It slammed the door on the Repocalypse immediately by going back into the biggest quantitative easing in US history (which isn’t an exaggeration; it’s an understatement). We are now at the point where the Fed has reduced its monetary/balance-sheet expansion by almost as much as it did back in 2018-2019. As a percentage of the total heap, however, it’s only about half as much; but in total dollars, it’s about the same. We already got one clue of what happens within banks and between banks with this level of tightening liquidity in banks when we had a banking collapse last March and April. That happened because the Fed’s QT hugely lowered the value of bonds (including Treasuries) that banks held in their balance sheet. As another story tells today, the drop in value in bank balance sheets is returning to where it was before all of the Fed’s emergency bank salvation efforts last spring. So, we are getting back to that problem zone, which we left for a little while when the Fed’s and FDIC’s emergency intervention took a lot of bonds out of the market so that bond yields settled back down for awhile; but they have been rising since then. The Fed will have to do about five times as much QT as it already has just to get back down to where it was pre-Covid when its last QT (the 2018-2019 batch) failed miserably and forced the Fed to do a face-plant on its promises by reverting to all-out QE, which it lamented as having hurt public trust in the Fed. A good part of the Fed’s QT consists of US Treasuries that the Fed promised it would roll off for years because it originally argued those purchases were merely a necessity of monetary policy, not a situation of the Fed financing the government … because thatwould be illegal. The proof that it was not “monetizing” the government debt, as such “money-printing” financing is called, would come in the Fed’s eventual unwinding of all of its QE because that would eventually force the government to find private/corporate financing for all of its debt. Part of the argument against the Fed during the face-plant was that its failure at pulling off QT proved the Fed had, in deed, monetized the US debt, as some of us were saying would prove to be the case all along on the basis that you cannot rebuild an economy on mountains of hot-air money and then suck out all the hot-air without collapsing the ballon economy you created. You see, if the “temporary” measure becomes permanent on the Fed’s balance sheet, that destroys that argument entirely because “permanent” means the Fed is having to continually roll over the government debt it has sopped up, leaving the Fed in a position of being the endless financier and carrier of the government debt. It looks like the Fed will end up stuck with monetizing the Federal debt, but how far down the perilous slope of demonetization will it attempt to go before it realizes that and chooses to risk accusations that it did what is outright illegal by financing the government with money created out of thin air — third-world style? I don’t know about you, but I haven’t heard any whispers from the Fed about stopping its QT. I don’t think it wants to hear those arguments again. So, when you hear that we are not going into a recession (an argument last week by Goldman Sachs that I rebutted in my last “Daily Doom”) due to the Fed’s tightening (a “soft landing”), don’t forget that the end of rate hikes is not the end of tightening! There is still that whole mountain of debt that the Fed legally has to roll off and hopes that it can roll off before the Fed gets down to a balance sheet that won’t bring accusations that it merely “saved the economy” by hosing up government debt so the government could get cheap loans to keep the charade of a debt-based economy going. We don’t know when the Fed will stop QT, but we have every reason all of that massive amount of QT that still has to come down will create havoc in the banking system as it slides. We have reason because we already saw this show up last March. We are further down the QT slope than we were then. Given the problems that a smaller drop already created for banks this year and the Repo problem when the Fed attempted a drop of about this amount (in total dollars) with its first failed attempt of QT, why would anyone believe going much deeper will go so much better? It makes no sense to conclude that. It’s just a wish that runs opposite of everything we’ve already seen about Fed QT. But denial is like that. So, when I say the Fed will tighten us into a severe recession, I am not making that assessment based on the current jobs market and current problems in the economy or even current inflation, not that those don’t also count. I am not even making just based on the level of interest increases we may have to hit before inflation is tamed. I am also making it based on what the Fed says it is still going to do with government bonds for many months, if not years, to come and how disastrous all attempts to do that have proven to be, forcing the Fed back to QE to save us from the death it sends cascading our way with each attempt. We can say, “Been there done that, and it wasn’t pretty. Did it again, and it resulted in major bank failures.” Now think about my opening statement in light of the above: Defaults on loans with banks that are not in the top-100 for size have already risen to the highest record ever! And we’re just getting started. The highest customer loan default levels ever are already happening in the small-to-mid-size sector of banking at a time when these banks have a huge amount of reduction yet to come in the value of their reserves as the Fed continues for years to come to keep rolling off bonds, which raises interest rates and reduces the value of the bank’s existing bonds. This statement about record defaults comes from an article titled “A massive credit card debt catastrophe is coming. Even though we are not yet in a recession, banks are already perilously close to collapse.” Now you can see why they are perilously close to collapse. Then pile on this little fact: As another story says today (buried in a larger story), the auction of three-year US Treasury notes on Monday drew the highest yield since 2007! Whoopee! Yields are soaring again, and the Treasury has greater and greater auctions in store due to the combined effect of Bidenflation deficit spending and refinancing the years of previous debt that now bears greater interest … all while the Fed plans to continue to roll off a whole lot more Treasury debt than it already has. MUCH more fun to come. Then consider this little headline that you can find below: “Usage of the Fed's emergency bank funding facility jumped by $328 million last week.” Whoa! I wonder what that was all about. We know how those types of things tend to pop up, as in the Repocalypse and as in last March’s bank busts, and suddenly turn out to be more than they initially seemed. You ain’t seen nothin’ yet! (Everyone can see the articles referenced above and the related articles highlighted below for free today, so please share!) The Daily Doom is a reader-supported publication. To receive new posts and support my continued work, consider becoming a free or paid subscriber — the latter being particularly helpful.

|

Send this article to a friend:

|

|

|

Seeing the Great Recession Before it Hit

Seeing the Great Recession Before it Hit![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)