Send this article to a friend:

September

16

2023

|

Send this article to a friend: September |

|

The Permanent Crisis Economy

Fifteen years after the 2008 global financial and economic meltdown, many say that America has recovered well. Gross domestic product, through the first quarter of 2023, was 28 percent higher than just before the crisis, buoyed by personal consumption, which has soared 35 percent. As of May, the economy boasted 17.6 million more private-sector jobs than prior to its 2007 precrisis peak, a 15 percent gain. After accounting for inflation, average weekly earnings are up 9 percent, helping to break the stagnation in pay that lasted for decades before 2008. Despite the 2020 Covid-19 shock, the broadest stock-market measure, the S&P 500 index, is nearly three times its pre-2008 high. The national housing market—the casus belli of the 2008 crash—is 61 percent above its precrisis 2006 peak. This spring, regulators stopped a run on regional banks before the worry spread to the broader economy; the tools that Congress forged to manage risk after the 2008 panic seem to be working. But while a building may look sturdy from the outside, what holds it up is what matters. Over the past decade and a half, politicians from both parties, with Federal Reserve help, doubled down on their pre-2008 economic strategy: they rebuilt the American economy on cheap debt. That money hasn’t funded productive assets—private investment in industry and public investment in infrastructure—that would generate real wealth. Instead, it has stoked consumer spending and puffed up paper-asset values. When the money had nowhere else to go, starting in 2021, it showed up as spiking inflation; more money chasing the same amount of goods and services pushed prices up. What happens next? If it was hard to deflate the last debt-fueled bubble—in fact, we never really did so—letting the air out of this one will be excruciating. The longer we delay, though, the more likely that markets will do it for us, despite the government’s bipartisan efforts to keep the party going. It’s tempting to think that 2008 changed everything. As the Lehman Brothers investment bank cratered that September 14, unleashing the biggest financial crisis the world had seen, George W. Bush was still president and Donald Trump was a reality-TV star. Socialism was hardly even a fringe movement in America, and standard-bearers of both parties regularly ran for, and won, office on similar platforms of low taxes, slimmer government, and free markets. Another bipartisan consensus emerged after 2008 but was very different: that the banking system fell because of greedy bankers, enabled by unregulated markets run amok. Avaricious bankers had tricked investors and regulators by inventing derivatives, such as credit-default swaps and collateralized debt obligations, that nobody could understand. These derivatives supposedly reduced risk; instead, they magnified it, hiding trillions of dollars in debt. Bankers tricked home buyers, too, particularly poorer ones, into dangerous mortgage contracts, with low initial “teaser” interest rates that almost immediately reset to much higher levels, prompting default and foreclosure. That fall, presidential candidates John McCain and Barack Obama blamed the meltdown on “lax regulation” and “regulatory agencies that weren’t doing their job,” respectively, and the parties began accusing each other of being in Wall Street’s thrall. Lots of this really happened. Outright fraud, as well as sloppiness in verifying mortgage borrowers’ income and assets and investigating the financial alchemy behind derivatives, was rampant. Elected officials across the political spectrum were lavishly funded by donors with Park Avenue zip codes. It’s not so surprising, then, that in the aftermath, the parties would embrace an angrier, less establishmentarian politics and reject free markets. Trump slayed the traditional market-oriented Republican Party to become a once and possibly future populist president; immoderate progressive politicians like Alexandria Ocasio-Cortez suddenly commanded outsize attention. No prominent official from either party would unequivocally praise free markets today. The crisis brought thousands of pages of new financial regulations, mostly via the Dodd-Frank Act, which President Obama signed in 2010. Since derivatives and too-easy mortgages helped cause the financial crisis, Dodd-Frank granted existing regulators more authority over derivatives, and it gave the new Consumer Financial Protection Bureau dominion over mortgages. It’s now much harder for financial institutions to offer unsophisticated home buyers mortgages that they could never repay or to conceal trillions of dollars in derivatives risk. Anger over the financial crisis’s massive bailouts also drove new regulations. Occupy Wall Street, the Tea Party, Elizabeth Warren, Ted Cruz—post-2008 politics reflected the public’s outrage over the trillions of dollars in taxpayer aid that Wall Street received that year, which included direct rescues of tottering institutions like Bank of America, as well as the Bush administration’s invention of the Troubled Assets Relief Program, or TARP, to inject capital into supposedly healthy, but weakened, financial institutions. To deter future bailouts, Dodd-Frank empowered regulators to force the largest financial institutions to compose “living wills,” which would run simulations of orderly failures that avoid using taxpayer funds. Regulators also won a new “orderly liquidation authority” to seize struggling financial behemoths and wind them down, without bailouts. Dodd-Frank was a way for technocratic Democrats like Obama to quell popular discontent without resorting to a broader populism. As late as 2015, a half-decade after Dodd-Frank and safely through most of his second term, Obama was boasting in his State of the Union address that “we have new tools to stop taxpayer-funded bailouts.”  A bipartisan consensus emerged after 2008 that the banking system collapsed because of greedy bankers and unregulated markets—but the deeper problem was America’s addiction to debt, which is worse than ever in 2023. (SANG TAN/AP PHOTO) A bipartisan consensus emerged after 2008 that the banking system collapsed because of greedy bankers and unregulated markets—but the deeper problem was America’s addiction to debt, which is worse than ever in 2023. (SANG TAN/AP PHOTO)

This approach was always facile. The 2008 crisis wasn’t just about sleazy mortgages or complex derivatives but, more fundamentally, about excessive debt. Over the three decades leading up to 2007, total debt in the American economy—encompassing government, business, and household borrowers—surged by nearly two and a half times, after accounting for inflation (as do all the figures I cite), to $47.4 trillion. (These numbers also outpaced population, which expanded 37 percent over this period.) Mortgage debt swelled the most: from $2.9 trillion to $15 trillion in 2007. This debt frenzy was a by-product of solving one problem, only to cause another. In the early 1980s, then–Federal Reserve chairman Paul Volcker ended the plague of the late 1970s: inflation, which reached a high of 14 percent in 1980. Between 1980 and 1983, to suppress inflation, the Fed nearly doubled the country’s base interest rate, to 19 percent, making it much tougher for people and businesses to borrow and lend, until the economy slowed enough so that demand for goods and services eased, and prices fell. After that, until 2022, inflation never topped 5 percent annually, save for one year. Such low inflation made lenders confident that their loans wouldn’t get repaid in less valuable dollars. So they offered debt galore.

Expectations of low inflation were especially important in the mortgage market because most mortgages carry 30-year terms at fixed interest rates. Were inflation to rise, borrowers would repay what they owed in cheaper dollars, causing the lender to lose money. Mortgage debt soared because it was implicit government policy—or, at least, it became such, once elected officials and regulators realized that it solved many problems, at least in the short run. For several decades, the U.S. economy had experienced massive dislocations, including the loss of nearly a quarter of its manufacturing jobs—4.3 million positions—to cheaper global locales and improved automation. During this period, too, labor productivity (economic output per worker) grew only 1.9 percent annually, down from 2.6 percent annually in the three decades after World War II. That sluggishness wasn’t workers’ fault; investors weren’t allocating their capital to the most productive uses. But workers still suffered from it. Between 1977 and 2007, the average weekly earnings of nonsupervisory employees shrank 9 percent. The political answer to cheap global labor and automation was to replace earnings income with paper wealth. Ever-cheaper mortgage debt propelled home prices upward, so people could extract home equity as a substitute for income. Higher house values and home-equity loans made homeowners feel wealthier. Everyone got on board: Republicans liked the idea of ownership of private assets; Democrats liked the mortgage subsidies from quasi-government mortgage guarantors Fannie Mae and Freddie Mac—a successful example, it seemed, of government intervention in markets. This motive was reinforced in 2000, when the dot-com stock-market bubble burst, followed a year later by the devastating 9/11 terror attacks. The NASDAQ tech-index market had plummeted from 5,000 in early 2000 to barely 1,210 by the fall of 2002. This collapse destroyed paper wealth and real jobs, funded through venture capital. The Federal Reserve, nervous about a deep recession, cut the main interest rate from 6.5 percent in mid-2000 to 1 percent, and kept it there through 2004, even as the economy began to recover. “The [Alan] Greenspan Fed attempted to compensate for the lack of speculative activity in the stock market [and] make residential real estate more attractive,” says James Grant of the venerable Grant’s Interest Rate Observer, by keeping the Fed funds rate “very, very low.” (The funds rate is what large financial institutions charge to lend to one another; this rate, in turn, indirectly determines private-sector interest rates for borrowing, such as mortgages, credit cards, and corporate bonds.) This policy “instigated a great program of borrowing and lending,” on top of what was already a great program of borrowing and lending. Thomas Hoenig, a Mercatus Center scholar, former Federal Reserve Bank of Kansas City president, and former member of the Federal Open Market Committee, which sets interest rates, agrees. The Fed’s early-2000s actions “accelerated artificial demand in the housing market,” he says. Individuals being able to borrow excessively generated “just an enormous amount of stimulus.” The Fed began raising rates in 2004, but it took four more years for the full crisis to occur. The housing market and the stock market peaked in 2006 and 2007, in turn. Another year would reveal the full extent of the financial industry’s potential losses on all of the cheap debt—and flimsy derivatives based on that debt—that it had issued. By 2007, interest rates weren’t even that high: the Fed had raised its main rate to just above 5 percent, historically normal. But the United States had become so debt-dependent that it could no longer stand normal interest rates. Everything exploded.  Charts by Alberto Mena Charts by Alberto Mena

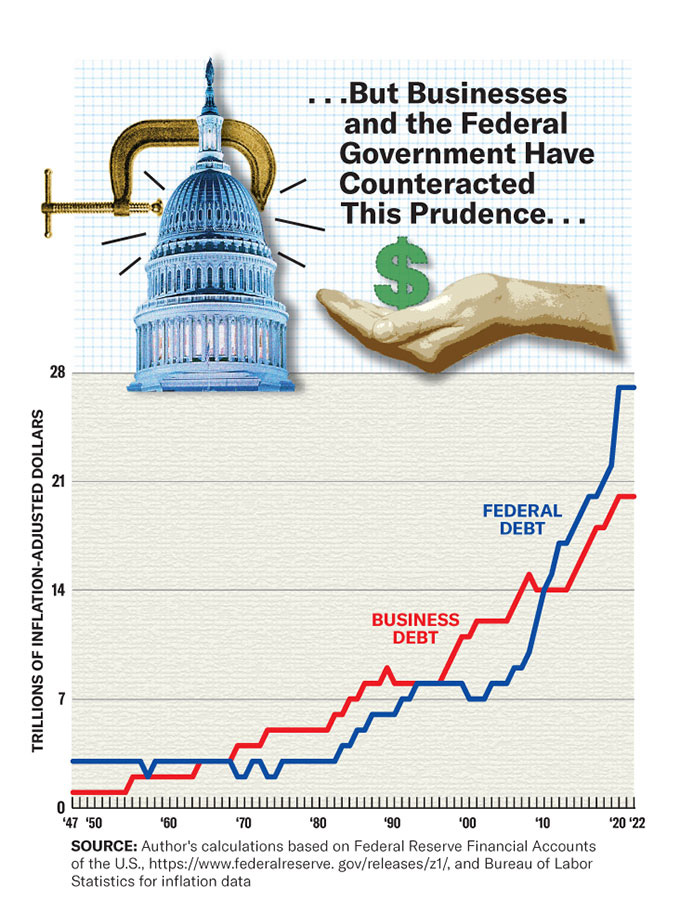

If you look only at explicit levels of mortgage debt since the crisis, you might think that the post-2008 regulations worked and that the source of the last disaster has been neutralized. Mortgage-lending terms have gotten tighter, and mortgage debt has steadily shrunk. As of 2022, at $12.5 trillion, it remained 17 percent below its highest levels. The massive pandemic boom in house prices—up 43 percent between early 2020 and mid-2022—wasn’t due to a loosening of lending standards but to wealthier people using their lockdown savings and newfound freedom from five-day-a-week commutes to move far from historical job centers, bidding up the price of traditionally cheaper real estate. Except that’s not the full story, or even most of it. As Americans stopped incurring unsustainable amounts of mortgage debt, Washington’s central planners stepped in to encourage them to incur other types of debt. In late 2008, spooked by the financial crisis, the Fed lowered interest rates, just as it did when the dot-com bubble burst. This time, it cut them to never-before-breached levels of near zero—less than a quarter of 1 percent—and kept them there until 2015, the longest period of low interest rates in history. It then started gingerly raising rates again. But even pre-pandemic, with unemployment at historical lows, the economy proved too fragile to withstand interest rates barely above 2 percent. Scared by 2019 market turbulence caused by its modest rate increases, the Fed started cutting rates again. The massive economic destruction from pandemic lockdowns had it again pushing rates toward zero, until early 2022. Other than for a short period, then, the American economy ran on near-zero interest rates for more than a decade after the financial crisis. What resulted? Americans ramped up on non-mortgage debt, borrowing for cars and for college, for instance. Accounting for a 30 percent rise in household debt, other than mortgages, since 2007, total household debt—including mortgages—stands at $19 trillion, less than 7 percent below its 2007 peak. And households have been conservative, compared with businesses. Nonfinancial firms now owe $19.9 trillion, 39 percent more than in 2007. Cheap financing in corporate bond markets encouraged firms to borrow to buy back their own stock; such corporate stock purchases inflated stock-market values. Riskier firms raised funds in “junk bond” markets to expand, or to buy other companies. Businesses and households together now owe $38.8 trillion, 12 percent more than in 2007. Given that businesses have more than made up for households’ mortgage prudence, the American private sector hasn’t kicked the debt habit—not by a long shot. That’s bad enough, as we have seen with the Fed raising rates over the past year to curb inflation, but much of this new debt differs from mortgage debt in a critical way: it comes due much more frequently than do 30-year mortgage loans, and thus must be refinanced at (now) higher interest rates more frequently. Auto loans, commercial real-estate loans, and junk bonds are far more sensitive to rising rates than are mortgages. To put the current situation in perspective, think of what higher interest rates, over four years, did to the economy between 2004 and 2008, when just a sliver of the mortgage market held floating-rate loans. Back then, moreover, businesses didn’t owe mountains of money; other than mortgages, neither did households. Commercial real-estate loans are a particular risk today. The Wall Street Journalestimates that $1.5 trillion in such loans comes due in the next three years. The work-from-home trend that has lasted long after the end of pandemic lockdowns makes the assets backing much of that debt—office buildings—worth less. Nearly 90 percent of such loans are “interest only,” meaning that the borrowers never pay down any principal during the loan’s term; they just keep refinancing it. As office-building prices fall and interest rates rise, owners must not only refinance maturing debt at a higher interest rate but also make a large cash payment to the lender to account for the lower value of the building. It’s true that nobody could have predicted the scale and persistence of the work-from-home phenomenon. But it’s also true that borrowers and lenders alike structured these loans to be vulnerable to any risk, even a mild recession. The biggest worry for the American economy in 2023, though, isn’t private-sector borrowing. It’s that the government has been on a 15-year borrowing spree. Through the Obama, Trump, and Biden administrations, Congress has approved record levels of deficit spending, paid not through tax collections but via Treasury debt. In 2007, the government owed $8.6 trillion in today’s dollars. As of the end of 2022, it owed more than triple that, $26.9 trillion, including $4.8 trillion in pandemic-era borrowing. Much of this was printed by the Fed: its balance sheet went from $1.3 trillion just before the financial crisis to a high of $8.9 trillion in 2022, as it conjured zeros on computer screens to buy Treasury debt, thus financing federal deficits. If the federal government spent this vast sum on productive assets—world-class physical infrastructure, say, or measurable improvements in education and skill levels—a resulting GDP boost might have helped repay that borrowing. Instead, much of the money funded direct cash transfers—in other words, money taken from future taxpayers to make payments to current households. It would be far less damaging, too, if the government had limited pandemic payouts to those genuinely needing help: workers whose jobs had vaporized or who had lost a substantial portion of their income. But the funds went to nearly everyone. The result: $3 trillion in excess private-sector savings, the Mercatus Center’s Hoenig estimates—money with nowhere productive to go. Paper-asset markets absorbed some of it. As Grant recalls, in 2002, after the dot-com collapse, Scott McNealy, then-CEO of computer giant Sun Microsystems, lamented that the tech bubble had expanded so much that investors thought it made sense to buy his company’s stock at ten times its revenues. For such a valuation to pay off for investors, McNealy observed, “I have to pay 100 percent of revenues for 10 straight years [to investors] in dividends,” assuming no employee salaries, no rent costs, and no tax payments. “Do you realize how ridiculous those basic assumptions are?” This May, however, Grant notes, NVIDIA, one of today’s tech darlings, traded at nearly 40 times its revenues. Cryptocurrencies, of course, have no revenues at all—and though they have lost more than two-thirds of their value since late 2021, they still store tens of billions of dollars in supposed wealth. The borrowed money also fired consumer spending. Americans no longer had to borrow equity from their homes to keep up, or even increase, their day-to-day spending; the government did it for them.

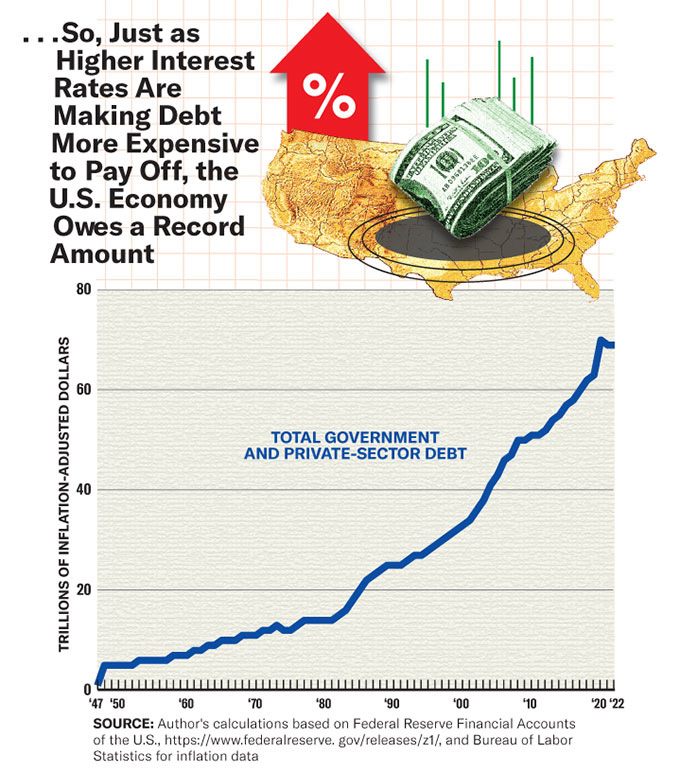

Fifteen years on from 2008, then, it’s hard to say that we’ve learned our lesson from the global financial crisis. Total debt in the economy is 45 percent higher than back then, at 68.9 trillion, 3.4 times GDP. In 2008, it was “only” three times GDP. If excess debt is a recipe for a financial crisis, as in 2008, what do today’s record debt levels mean for the financial system, as interest rates rise again? Since mid-2022, the Fed’s effort to reduce inflation has brought interest rates from near zero to above 5 percent. More borrowers thus struggle to pay their debts, as they reset at higher interest rates. The institutions that lend that money—banks or other large investors—suffer losses. But even debt issued at long-term low interest rates, with a borrower certain to repay, is no sure thing. The federal government will keep paying its long-term debt, despite higher interest rates; it can simply print money to do so. But the government will repay that debt in cheaper dollars, as inflation bites, and at interest rates lower than what lenders could command in the current market. Lenders, including large financial institutions, face losses on that debt. These can be massive: Silicon Valley Bank, with its $210 billion in assets, failed in early 2023 largely because it had invested its depositors’ money in plain old Treasury bonds, which lost value as rates rose. Indeed, what Hoenig terms a “mini-financial crisis” this spring shows that post-2008 regulations have not made the financial system sufficiently secure. It’s axiomatic that when interest rates rise, the tens of trillions of dollars of government and private-sector debt previously issued at much lower interest rates are worth less, and that those losses harm the financial system. With a rise in interest rates of a factor of 20 over the past year, says Hoenig, losses on money lent at lower interest rates “are pretty dramatic,” even if so far “unrecognized” because most of the creditor financial institutions haven’t yet had to sell those loans or bonds at fire-sale prices. So far, three midsize institutions—Silicon Valley, Signature Bank, and First Republic Bank—have fallen to the rising rates. The three midsize bank failures underscore another reality: post-2008 financial regulations haven’t ended bailouts. Regulators did not use their Dodd-Frank-established “orderly liquidation authority” to wind down any of the three banks and ensure that investors—including depositors above the FDIC’s quarter-million-dollar threshold—took the losses that they had risked. In fact, they offered an extraordinary bailout to large depositors in two of the cases—Silicon Valley and Signature. In the third case, the government offered guarantees to engineer a sale of First Republic to JPMorgan Chase, already the nation’s largest bank. After all those thousands of pages of new regulations, the government is thus still afraid to let even one midsize bank fail through the orderly liquidation authority it devised. Such a failure, it apparently believes, could damage confidence in all other such firms—that is, the entire financial system.

Our biggest post-2008 mistake, though, is neglecting to heed the real lesson of the financial crisis: it’s not free markets that failed, but central planning. The government, through low interest rates and subsidies for mortgages, tried to load the economy up with debt before 2008 to hide more serious problems. Markets, by withdrawing investments in the 2008 panic, tried to show that this strategy was untenable. What we should have done back then was slowly wean the economy from its debt addiction and use what limited debt we did issue to make the economy more productive. Excessive borrowing since the crisis has done nothing to boost productivity. It has grown at just 1.5 percent annually since 2008 and was negative in 2022, for only the second time in four decades. “Real productivity in the economy has slowed,” says Hoenig. “Wealth is only created through increases in productivity. That’s the only way you solve this in the long run.” We’ve likely seen only the first of the financial and economic dislocations caused by higher interest rates, and the Fed will face pressure to reverse course, lowering rates again at the first sign of recession. “Pressure to print money is going to be enormous,” says Hoenig. Only one countervailing force may keep the Fed from surrendering to that pressure: persistent high inflation. Fed officials seem to realize, even if the politicians haven’t yet, that the U.S. has hit the limits of printing and borrowing money to juice the economy. As Americans run out of even spurious investment choices for that largesse—NFTs, anyone?—excess money just inflates the prices of goods and services. Printing money does not create more wealth. We would be wise to heed this market signal. The government, suggests Grant, should “recognize that interest rates are prices, perhaps the most consequential prices in the market economy,” and let the market itself, rather than the government, set them. That is, banks could decide at what interest rate to lend to one another, based on market conditions, without federal interference. Hoenig, by contrast, is more technocratic than libertarian: both parties in Congress should cooperate, “moderate” federal spending, invest in productive assets, and ensure, through normalized interest rates, that the private sector invests in productive assets, as well. “It’s going to take at least a decade to bring it back into balance,” he maintains. “Economic resources can be allocated” more efficiently, and “spending and savings can be rebalanced.” Simple!

|

Send this article to a friend:

|

|

|

We’re still living in 2008.

We’re still living in 2008.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)