Send this article to a friend:

September

03

2020

|

Send this article to a friend: September |

|

The Fed's Stupidity is Still Well Anchored

A Non-Robust and Painfully Slow Evolution Please consider A Robust Evolution by Richard Clarida. Self-Serving Praise

Three major bubbles of increasing amplitude and three severe recessions is not worthy of self-praise. Phillips Curve Yet Again

The Phillips Curve, an economic model developed by A. W. Phillips, purports that inflation and unemployment have a stable and inverse relationship. Simply put, as unemployment falls, consumer price inflation rises. This has been a fundamental guiding economic theory used by the Fed for decades to set interest rates. Former Fed chairs Janet Yellen and Ben Bernanke were both big Phillips Curve advocates despite the fact the theory never worked even according to Fed studies.

The Phillips Curve isn’t dead, it was never alive to begin with. The Fed may finally grasp the notion that it based decades of policy on a concept that never worked. But to mask over that idea, it gave itself fake praise. Inflation, Uncertainty, and Monetary Policy Please consider this snip from Inflation, Uncertainty, and Monetary Policy by then Fed Chair Janet Yellen on September 26, 2017.

Clarida on Inflation Expectation With that flashback out of the way, let’s return to the more folly from Clarida on inflation expectations.

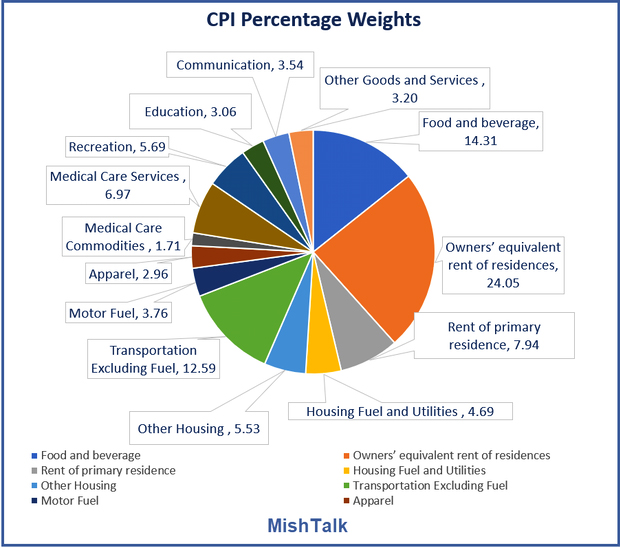

Inflation Expectation Nonsense While finally admitting that the Phillips Curve is useless, the Fed shifted its focus to yet another totally bogus and easily disproved concept. To understand why let's review the CPI makeup.

Inflation Expectations Q&A

Housing, medical care, gasoline, food, auto repairs are all inelastic items. People will buy those those things and more at a steady pace no matter what their inflation expectations might be. Even clothes are mostly inelastic. If someone needs a coat they generally will buy one and they won't buy another even if they expect prices will go up. Yes, people shop sales, but they also don't hold off buying computers even though the price-performance ratio drops every year. CPI a Flawed Measure Moreover, the notion that one can measure inflation by the CPI is itself extremely flawed. Ask anyone buying their own health insurance or paying college tuition about their measure of inflation. Stupidity Still Well Anchored The only thing that’s “well anchored” is the stupidity of the belief that inflation expectations matter. Asset Irony People will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down. People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop. The very things where expectations do matter are the very things the Fed and mainstream media ignore. BIS Deflation Study The BIS did a historical study and found routine deflation was not any problem at all. "Deflation may actually boost output. Lower prices increase real incomes and wealth. And they may also make export goods more competitive,” stated the study. Central banks’ seriously misguided attempts to defeat routine consumer price deflation is what fuels the destructive asset bubbles that eventually collapse. For a discussion of the BIS study, please see Historical Perspective on CPI Deflations: How Damaging are They?

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)