Send this article to a friend:

September

20

2019

|

Send this article to a friend: September |

|

The Fed & The Stability/Instability Paradox

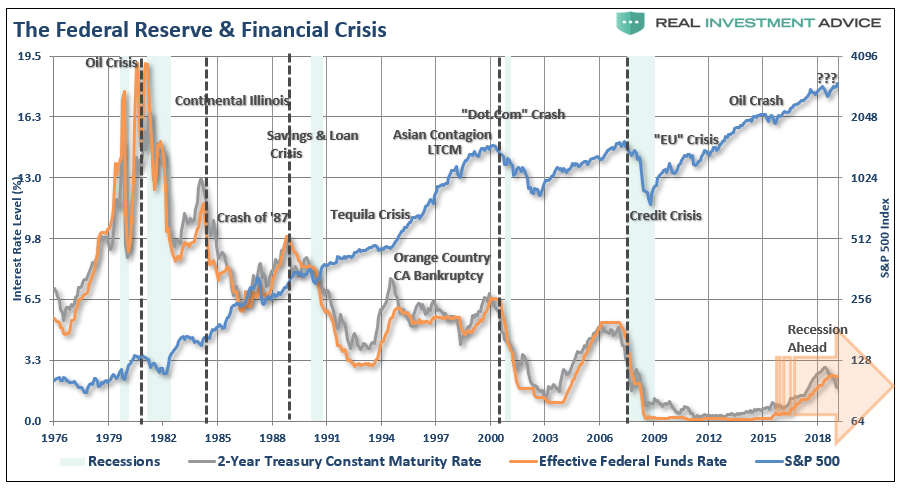

Well, this certainly seems to be the path that the Federal Reserve, and global Central Banks, have decided take. Yesterday, the Fed lowered interest rates by a quarter-point and maintained their “dovish” stance but suggested they are open to “allowing the balance sheet to grow.” While this isn’t anything more than just stopping Q.T. entirely, the markets took this as a sign that Q.E. is just around the corner. That expectation is likely misguided as the Fed seems completely unconcerned of any recessionary impact in the near-term. However, such has always been the case, historically speaking, just before the onset of a recession. This is because the Fed, and economists in general, make predictions based on lagging data which is subject to large future revisions. Regardless, the outcome of the Fed’s monetary policies has always been, without exception, either poor, or disastrous.

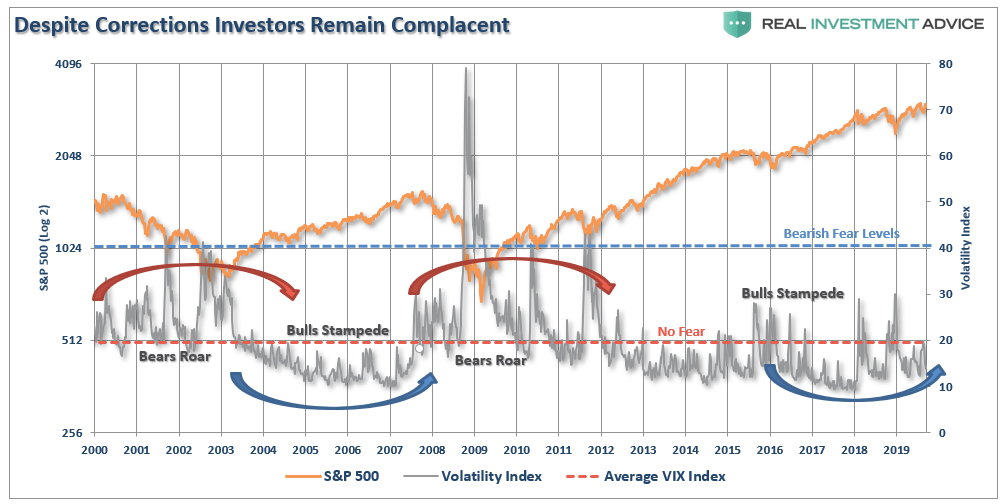

The idea of pushing limits to extremes also applies to stock market investors. As we pointed out on Tuesday, the risks of a liquidity-driven event have increased markedly in recent months. Yet, despite the apparent risk, investors have virtually “no fear.” (Bullish advances are supported by extremely low levels of volatility below the long-term average of 19.)

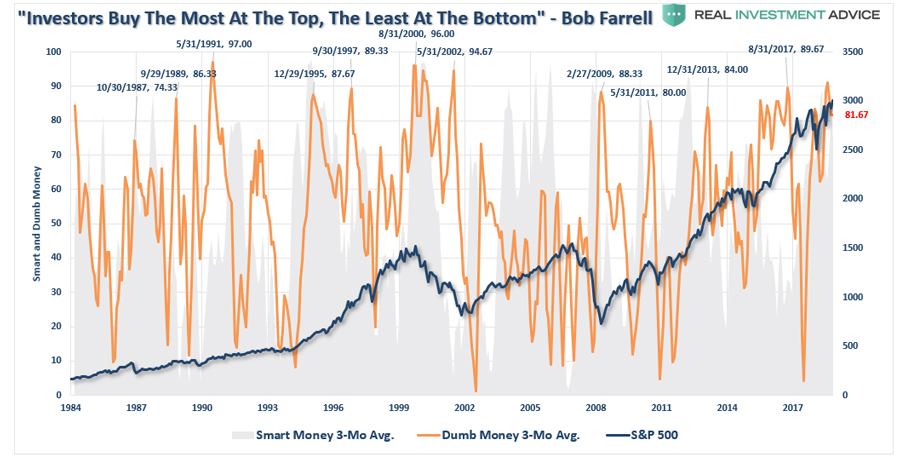

In the “rush to be bullish” this a point often missed. When markets are hitting “record levels,” it is when investors get “the most bullish.” That is the case currently with retail investors “all in.”

Conversely, they are the most “bearish” at the lows. It is just human nature.

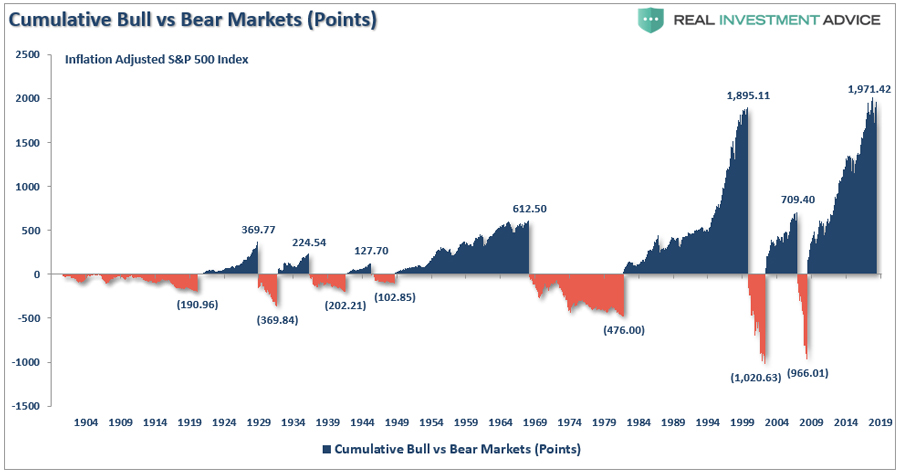

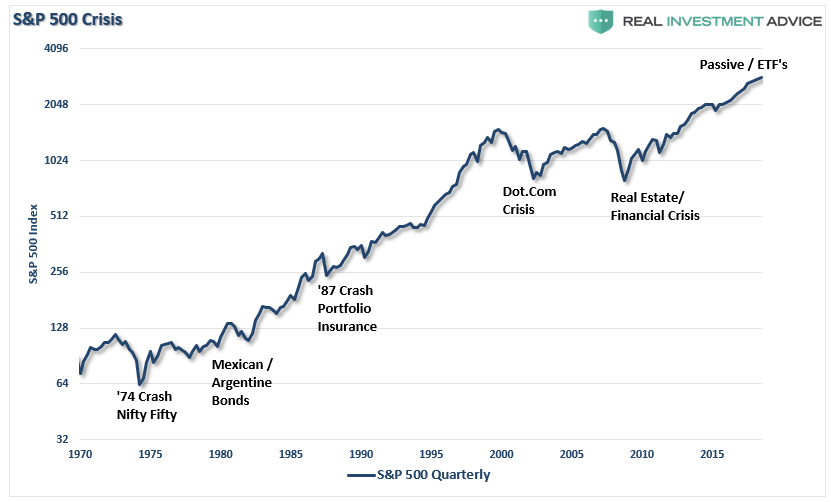

The point here is that “all things do come to an end.” The further from the “mean” something has gotten, the greater the reversion is going to be. The two charts below illustrate this point clearly.

Bull markets, with regularity, are almost entirely wiped out by the subsequent bear market. Despite the best of intentions, market participants never act rationally. Neither do consumers. The Instability Of Stability This is the problem facing the Fed. Currently, investors have been led to believe that no matter what happens, the Fed can bail out the markets and keep the bull market going for a while longer. Or rather, as Dr. Irving Fisher once uttered:

Interestingly, the Fed is dependent on both market participants, and consumers, believing in this idea. As we have noted previously, with the entirety of the financial ecosystem now more heavily levered than ever, due to the Fed’s profligate measures of suppressing interest rates and flooding the system with excessive levels of liquidity, the “instability of stability” is now the most significant risk. The “stability/instability paradox” assumes that all players are rational and such rationality implies an avoidance of complete destruction. In other words, all players will act rationally, and no one will push “the big red button.” The Fed is highly dependent on this assumption as it provides the “room” needed, after more than 10-years of the most unprecedented monetary policy program in U.S. history, to try and navigate the risks that have built up in the system. Simply, the Fed is dependent on “everyone acting rationally.” Unfortunately, that has never been the case. The behavioral biases of individuals is one of the most serious risks facing the Fed. Throughout history, as noted above, the Fed’s actions have repeatedly led to negative outcomes despite the best of intentions.

As noted Tuesday, the risk to this entire house of cards is a credit-related event.

Risk concentration always seems rational at the beginning, and the initial successes of the trends it creates can be self-reinforcing. That is, until suddenly, and often without warning, it all goes “pear\-shaped.” In November and December of last year, it was the uniformity of the price moves which revealed the fallacy “passive investing” as investors headed for the door all at the same time. While, that rout was quickly forgotten as markets stormed back to all-time highs, on “hopes” of Central Bank liquidity and “trade deals.” The difference today, versus then, are the warning signs of deterioration in areas which pose a direct threat to everyone “acting rationally.”

Risk is clearly elevated as the Fed is cutting rates despite the “economic data” not supporting it. This is clearly meant to keep everyone acting rationally for now. The problem comes when they don’t. The Single Biggest Risk To Your Money All of this underscores the single biggest risk to your investment portfolio. In extremely long bull market cycles, investors become “willfully blind,” to the underlying inherent risks. Or rather, it is the “hubris” of investors they are now “smarter than the market.” Yet, the list of concerns remains despite being completely ignored by investors and the mainstream media.

For now, none of that matters as the Fed seems to have everything under control. The more the market rises, the more reinforced the belief “this time is different” becomes. Yes, our investment portfolios remain invested on the long-side for now. (Although we continue to carry slightly higher levels of cash and hedges.) However, that will change, and rapidly so, at the first sign of the “instability of stability.” Unfortunately, by the time the Fed realizes what they have done, it has always been too late.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](images/t24_ag_en_usoz_2.jpg)