|

|

Fifty Years of Suppressing Silver

Sophisticated precious metals investors are well-aware of the rampant manipulation of the gold and silver markets. They are also generally aware of the reason for such manipulation. A rapid rise in the price of gold and silver is like an economic “warning siren” - alerting savers that their wealth (i.e. the purchasing power of their currency) is being rapidly eroded by the monetary depravity of bankers. In a world with a “gold standard”, this isn't a problem. With currency which is redeemable in gold (or silver), the value of a currency (i.e. its purchasing power) is anchored by the gold and silver backing it. However, in a world of nothing but “fiat currencies” (i.e. money backed by nothing), a loss of public confidence in paper “money” is the worst nightmare of bankers. This fear can be most easily illustrated by simply looking at the example of Alan Greenspan. In 1966, Greenspan was a respected academic, who wrote a famous essay extolling the virtues of a gold standard, where he simply stated the evils of “fiat money”: “In the absence of a gold standard there is no way to protect savings from confiscation through inflation.” I explained this concept of banker-stealing, in great detail, in a previous commentary – so any readers who are interested in a thorough discussion of this should refer to that piece. A quarter of a century later, after “Easy Al” had sold his soul to the bankers, and become Chairman of the Federal Reserve, he was asked directly what he would do if/when people lost confidence in their “fiat” U.S. dollars. His response to that question is even more famous: “We stand ready to lease gold in ever-increasing amounts.” Several obvious, observations flow from this. Not only are fiat-currencies a tool which bankers use to directly steal our wealth, but this “tool” is, in fact, nothing but a scam by a bunch of con-men – and (like all scams) it collapses as soon as those being scammed “lose confidence” (i.e. understand that they are being 'conned'). What highlights the illegitimate (and ultimately illegal) nature of this scam is that the primary mechanism which the Chairman of the Federal Reserve would (and does) use to “restore confidence” to the world's “reserve currency” is to (illegally) manipulate the gold market. Put another way, because this is a scam, there is no way to directly “restore confidence” to paper currencies. Instead, all the bankers can try to do is to (temporarily) destroy confidence in gold – by suddenly dumping vast quantities onto the market, in order to cause the price to drop. Manipulation of the gold market actually began (on a small scale) in the 1960s, while the U.S. (and the world) was still partially on a gold standard. The U.S. government was “cheating” with its accounting, to hide the obscene amounts of money it was borrowing (and squandering) in its doomed war-effort in Vietnam. Thus, this manipulation is a coordinated scheme by Western bankers which is now nearly 50 years old. Like gold, the silver market has been manipulated for roughly the same amount of time. However, in keeping with silver's modern “identity” as an “industrial metal”, the evolution of silver-manipulation, and the mechanisms used to manipulate the silver market are vastly different from the gold market. To begin with, back in the 1960's when we were officially said to be on a “gold standard”, in fact, it was only silver money which was widely circulated in our economies, in the form of small-denomination coins. In other words, while our monetary systems were anchored by gold, it was silver which was used as money in an “industrial” sense – as an indispensable tool of basic commerce. Indeed, at the same time that the bankers were trying to prop-up the U.S. dollar while on the gold standard (due to their reckless money-printing and debt-creation), these same bankers (and their allies in government) were making their first efforts to defuse a “silver supply crisis” - caused by pricing silver at only a fraction of its true worth. In the 1960s, the U.S. government had kept the price of silver frozen at $1.29/oz. However, whenever an asset is under-priced, there will always be a group of investors who will identify such an under-priced asset – and then accumulate it. Thus, the U.S. (and other governments) were rapidly squandering their entire stockpiles of silver, as they had to dump ever-increasing amounts onto the market to maintain the artificially low price. Ultimately, the bankers capitulated, and the U.S. government ceased its efforts to keep the price of silver frozen at $1.29. However, as is usually the case with any illegitimate scheme, every time the schemers take action to deal with one flaw in their plans, that produces unintended (and undesirable) consequences – which then require further acts of manipulation. Once the price of silver was allowed to rise, very quickly the actual value of the silver contained in our small denomination coins (primarily the 10-cent and 25-cent pieces) greatly exceeded their face-value as legal tender. This created a huge incentive to melt-down these coins and make a very profitable arbitrage trade of “buying” these coins at their face value, and then selling them for their metal-content. The U.S. government responded in two ways (and was quickly copied by the Canadian government). First, it changed the composition of all newly-issued coins – removing all their silver content. U.S. dimes had 90% silver-content up until 1964, while Canadian dimes contained just over 80% silver. The table below provides the evolution of the Canadian dime. History of Composition

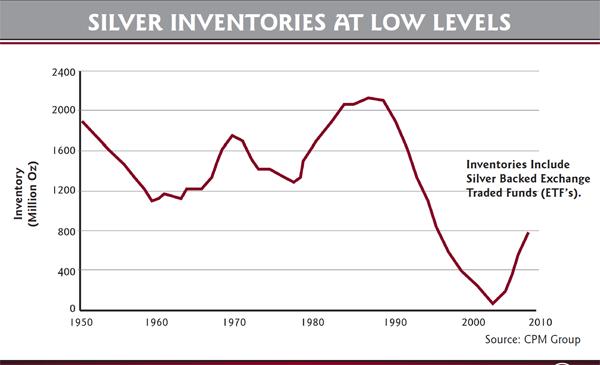

Meanwhile, the U.S.' 1965 Coinage Act made it a crime to melt-down any legal tender coins (in order to profit on their metal-content), and a duplicate measure was passed in Canada. Consider the true dynamics of this measure. First the bankers abolish the gold standard, to allow them to rapidly accelerate the speed at which they steal from us through currency-dilution. This, in turn, requires them to (illegally) manipulate the gold and silver markets – in order to hide the true value of these metals from being expressed in the bankers' diluted paper. The government then makes it a “crime” for its own citizens to make a profit on their own money. In the bankers' scam of money-dilution, only the bankers are allowed to profit on their crimes. It was at this point in history that the bankers were able to largely forget about manipulating the silver market (for many years), and to focus their energies on gold-manipulation – because basic market fundamentals created conditions which depressed the price of silver, with only minimal “assistance” from the bankers (and their servants in government). In this respect, I'm indebted to Adrian Douglas of GATA, for drawing my attention to the true significance of silver as a modern “industrial” metal first, and a monetary metal second. While many media talking-heads erroneously state that “silver is an industrial metal, not a monetary metal”, in fact silver is both an industrial metal and a monetary metal – while gold is almost exclusively a monetary metal. Since few mainstream pundits understand what is “precious” about precious metals (i.e. it is the best money our species has ever devised), they don't understand the simple logic that silver's enormous industrial versatility and importance can't make it less “precious”, but only more so. Indeed, it is Mr. Douglas' position that silver has become too important industrially (i.e. too “precious”) to be widely used again as money. Putting aside that separate issue, clearly the price of silver has been driven in recent decades mostly by its industrial demand. And it is this industrial demand which (with a little help from the bankers) kept the price of silver well below its true value for more than thirty years (until early in this decade). How does industrial demand depress the price of silver? Ironically, it is due to how the brains of bankers functions. If a mining company went to a bank for a loan to build a new silver mine with the sales-pitch that silver was grossly undervalued, and they wanted to produce this valuable commodity in order to capitalize on this investment opportunity, the reaction of the banker is totally predictable. The banker would burst into laughter, and (if he was polite) would warn the mining executives not to let the door hit them on their way out. While bankers see nothing wrong with taking our money which we deposit with them, and gambling it on any and every “investment” which tickles their fancy; these hypocrites would never dream of allowing ordinary people (i.e. non-bankers) to do the same thing with their money. Conversely, if this same mining company approached the bank for a loan, and provided them with statistics on the amount of silver being consumed in various industrial applications (old and new), the bankers would behave in a much different manner. Assuming that the mining company demonstrated that they could mine their silver at a cost below the current price, the banker would happily reach for his cheque-book. This leads us to a fundamental “truth” in the precious metals sector: investment demand (i.e. “speculative” demand) does not stimulate mine production (except in a very belated manner – only after inventories have been exhausted), while industrial demand does stimulate higher levels of mine production, because the bankers will finance new mine-production based upon that level of industrial use. As an aside, it was because gold is not used to a great degree "industrially" that the bankers had to "persuade" the world's largest gold miners to enter into vast "hedging agreements" - which simulated the same market conditions for gold: maximizing production at the lowest, possible price. In a true “equilibrium”, this industrial production and demand would not cause silver to trade at a price well below its fair-market (equilibrium) value. However, the bankers ensured that the silver market could never reach such an equilibrium by continuing to dump their waning stockpiles of silver onto the market. Here I am sure there are a few astute readers who will question my characterization of the “demand model” for silver. They will point out that most of the world's silver is still produced as “byproducts” of other mining. In other words, it is a secondary product of mines which primarily extract gold or copper or lead/zinc. Thus, others will argue that industrial demand for silver could not directly stimulate silver mining, and therefore total silver production. In fact, while that argument has theoretical merit, in practical terms it is incorrect. To begin with, if silver was properly priced, many of the mines where silver is currently produced as a “byproduct” of other metals would instantly become “silver mines” - with the other metals becoming the “byproducts”. Regular readers know that the long-term gold/silver price ratio averages roughly 15:1 (over a period of nearly 5,000 years). Given that silver occurs in the Earth's crust at roughly a 17:1 ratio versus gold, there is obvious, objective validation for such a ratio. In addition, given that most of the world's stockpiles of silver have (literally) been consumed, any rational valuation of silver would have to be at a ratio of 15:1 or less. With the price of gold currently at $1200/oz (and with that price being the result of market-manipulation), clearly the fair-market price for silver would have to be a minimum of $80/oz today. In addition, in mines where silver is currently produced as a “byproduct”, the industrial demand for silver (i.e. the silver “credits”) is still fully considered in determining whether any particular mine will be financed to go into production – but with those decisions also being based upon demand for the other metals. Given that the price of silver has been highly correlated with most of those other metals, my analysis still holds true. However, even in a world where the gross under-pricing of silver means that there are few (official) “primary” silver mines, there are still “mining companies” able to obtain financing only for silver, but based upon polymetallic mines, where silver is officially a byproduct. Silver Wheaton (SLW) is officially classified as a “silver mining company”, however what it is really is a “silver marketing company”. What Silver Wheaton does is to buy-up the future production-streams of silver from other miners (where silver is a mine byproduct), and then as that silver is produced, it sells this silver onto the market at the prevailing “spot” price. Apart from the ingenuity of this business model, what is relevant is that Silver Wheaton goes to a bank for financing, to buy-up the production-stream of a particular mine – and Silver Wheaton obtains that financing based upon industrial demand fundamentals for only silver. Thus, even in a market which has been horribly distorted through manipulation, the principle which I articulated earlier is still applicable: the industrial demand for silver is an important factor in helping the bankers suppress the price of silver. Obviously, the limiting factor in the bankers' game of market-manipulation is the amount of bullion they have to dump onto the market. As I have pointed out on many occasions, between 1990 and 2005, official silver inventories plummeted by approximately 90%. It is simple economics that any good which is grossly under-priced will be grossly over-consumed. Faced with the abrupt end to their silver-manipulation (which would make it much more difficult to continue to manipulate the gold market), the bankers fell back upon their oldest and most-favorite swindle: they sold paper to people, and pretended that the paper represented actual silver – and thus “SLV” was born. This is such an obvious sham that I simply lack the space to go until all of the clearly fraudulent implications of this fund, so I will restrict myself to just a couple of facets. From 2005 to the end of 2008, after silver inventories plummeted by 90% in just 15 years (due to being grossly under-priced), we are supposed to believe that inventories suddenly 'made a U-turn' – and tripled over the course of just four years. Regular readers will be familiar with the following chart, which shows the progression of “official” silver inventories – along with the small caveat attached to the graph. These official inventories include every ounce of ETF-silver, and SLV (by far the largest silver-ETF) was created at the beginning of 2006. As of the beginning of 2009, ETF-holdings represented roughly 2/3 of total “official inventories”. click to enlarge

At the end of 2009, roughly two-thirds of official, global inventories of silver were nothing but an obvious paper-sham. Making this potentially much more egregious, the supposed “custodian” for most of this silver is JP Morgan (JPM), which holds the world's largest “short” position in silver, the most-concentrated position in the history of commodities markets. In what is obviously not a “coincidence” the total size of the global short position has stayed roughly equal to the (supposed) total holdings of “bullion-ETFs”. However, those massive short positions are never audited, meaning that JP Morgan (and the other bullion-banks) have never been able to show they have more than half the silver necessary to cover both their short-positions and “custodian agreements” with the ETFs. What this directly implies is that as of 2009, as much as 2/3 of total global inventories of “silver” was literally nothing but banker-paper – and we can only assume that their massive scheme has expanded in the time that has since elapsed. While industrial demand for silver helped the banksters in their nefarious (and illegal) schemes for many years, it is now industrial demand which is certain to destroy the bullion-banks. While a gold-investor might be capable of being duped into buying banker-paper, and mistakenly believe that the banker-paper is “as good as gold”, you can't use banker-paper to make silver bearings, or silver mirrors, or silver batteries, or silver solar cells, or silver anti-bacterial products. The bankers market-manipulation has progressed from merely dumping the silver which they held, to the much more fraudulent practice of passing off their worthless paper as “bullion”. In doing so, they have eliminated the possibility of the price of silver merely “correcting”. What has become totally inevitable after 50 years of constant manipulation of the silver market is that this market is poised for the most spectacular default in the history of commodities markets – even more so than in the gold market. Companies which require silver to continue the existence of their businesses will be ready to bid-up the price of the commodity to multiples many times greater than an investor merely making a discretionary purchase. We can only assume that when a silver default occurs that it would bankrupt JP Morgan. Keep in mind that while the nominal value of JP Morgan's silver, short position is in the billions of dollars, thanks to the testimony of Jeffrey Christian at the CFTC hearings we know that this short position has been leveraged by somewhere around 100:1. Furthermore, the potential loss on any/every short position is infinite – since there is no “maximum price” which silver could not (theoretically) surpass. Perhaps this is the real explanation of JP Morgan's decision to close its "proprietary trading" unit (and likely create a walled-off subsidiary to replace it)? As the old saying goes, “For every winner in a trade there is a loser.” There must be a few investors out there who would like to get on the “winning side” of a trade with JP Morgan. Disclosure: I hold no position in JP Morgan, SLV, or Silver Wheaton.

It also provides basic coverage of Canadian precious metals mining companies. Canada is the global leader in mining exploration, and Canadian-listed mining companies (on the Toronto Stock Exchange and Venture Exchange) are responsible for the majority of the world's most-promising discoveries. |

|

|

Jeff Nielson is from Canada and is a writer/editor for Bullion Bulls Canada (http://www.bullionbullscanada.com/#content). He has a personal background in law and economics. Bullion Bulls Canada provides general macro-economic and political commentary, since the precious metals markets are among the most complex (and misunderstood) in the world.

Jeff Nielson is from Canada and is a writer/editor for Bullion Bulls Canada (http://www.bullionbullscanada.com/#content). He has a personal background in law and economics. Bullion Bulls Canada provides general macro-economic and political commentary, since the precious metals markets are among the most complex (and misunderstood) in the world.