Send this article to a friend:

July

12

2021

|

Send this article to a friend: July |

|

A Contrarian Investor’s Approach To OPEC’s Oil Spat

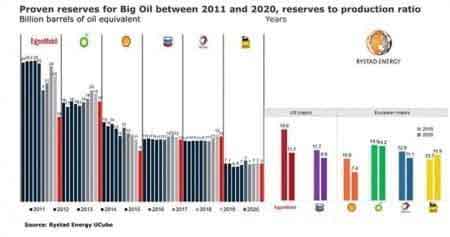

Oil prices have been reeling ever since OPEC+ talks collapsed on Monday due to major disagreements by its members. Major cracks appeared in the ministerial meeting with the United Arab Emirates continuing to block an agreement because it wants to increase its oil production before demand falls as per WSJ. The market fears that the UAE might "want out of OPEC so it can pump 4M bbl/day and make hay while the sun shines," Phil Flynn, market analyst at Price Futures Group, has told MarketWatch. The UAE's objection derailed a proposal to ease existing output curbs in a controlled manner and allow production to rise by 400K bbl/day each month through December leading to a planned OPEC+ meeting being called off with no new suggested date for the next gathering. This, in effect, leaves the organization’s current production limits in place. However, there’s a growing sense that the latest development is not necessarily bullish for oil markets because of the risk that the whole thing might fall apart and become a free for all, meaning a lot more oil potentially gets put on the market. The markets appear spooked, with oil futures charts in deep backwardation; in fact, oil prices for U.S. crude for delivery in December 2021 are currently trading at a $7/bbl premium to oil for delivery in December 2022, the highest spread on record. Meanwhile, data by the U.S. Commodity Futures Trading Commission shows that short positions among producers climbed to the highest since 2007 by mid-June, though they have been declining since then. Those are bearish signals, portending that the market believes that current oil prices are not sustainable. Nevertheless, the contrarian investor might beg to differ. Here are 3 key reasons why now might actually be a prime opportunity to load up on oil and gas stocks: #1. Record Revenues According to the Norwegian energy navel-gazer, U.S. shale producers can expect a record-high hydrocarbon revenue of $195 billion before factoring in hedges in 2021 if WTI futures continue their strong run and average at $60 per barrel this year and natural gas and NGL prices remain steady. The previous record for pre-hedge revenues was $191 billion set in 2019. The estimate includes hydrocarbon sales from all tight oil horizontal wells in the Permian, Bakken, Anadarko, Eagle Ford, and Niobrara. That said, Rystad says corporate cash flows from operations may not reach a record before 2022 due to hedging losses amounting to $10 billion worth of revenue in the current year. The good thing is that hedging losses might not be that high in the coming year because producers are not so keen on using them. Shale companies typically increase production and add to hedges when oil prices railly, in a bid to lock in profits. However, the mad post-pandemic rally has left many wondering whether this can really last and led to many firms backing off from hedging. Indeed, 53 oil producers tracked by Wood Mackenzie have only hedged 32% of expected 2021 production volumes, considerably less than the same time a year ago. And who is to say that oil prices cannot remain elevated. Goldman firmly belongs to the bull camp and sees oil staying between $75-80 per barrel over the next 18 months. That level should help companies deleverage and improve their returns. Goldman has recommended Occidental (NYSE:OXY) (-0.83%), ExxonMobil (NYSE:XOM)(-0.42%), Devon (NYSE:DVN) (0.03%), Hess (NYSE:HES) (0.82%), and Schlumberger(NYSE:SLB) (0.16%), among others. Goldman is not the only oil bull on Wall Street. In early June, John Kilduff of Again Capital predicted that Brent would hit $80 a barrel in summer and WTI to trade in the $75 to $80 range, thanks to robust gasoline demand. #2 Mild Capex Growth Shale drillers have a history of matching their capital spending to the strength of oil and gas prices, but not this time around. Rystad says that whereas hydrocarbon sales, cash from operations, and EBITDA for tight oil producers are all likely to test new record highs if WTI averages at least $60 per barrel this year, capital expenditure will only see muted growth as many producers remain committed to maintaining operational discipline. “From the upstream cash flow perspective, we see reinvestment rates falling to 57% in the Permian and to 46% in other oil regions this year. Corporate reinvestment rates are generally expected to be in the 60-70% range this year due to debt servicing and hedging losses,“ Artem Abramov, head of shale research at Rystad Energy, has said. Rystad says company-by-company research suggests an average industry-wide reinvestment rate of 50% with WTI @$65 WTI; 60% at $55, and 70% at $45 per barrel in 2021 through 2025. In other words, oil and gas companies are likely to keep capex muted even with higher oil prices, meaning a lot of that money is likely to be returned to shareholders in the form of dividends and share buybacks. #3. Supply Crunch Though less frequently discussed seriously compared to Peak Oil Demand, Peak Oil Supply remains a distinct possibility over the next couple of years. In the past, supply-side "peak oil" theories mostly turned out to be wrong mainly because their proponents invariably underestimated the enormity of yet-to-be-discovered resources. In more recent years, demand-side "peak oil" theory has always managed to overestimate the ability of renewable energy sources and electric vehicles to displace fossil fuels. Then, of course, few could have foretold the explosive growth of U.S. shale that added 13 million barrels per day to global supply from just 1-2 million b/d in the space of just a decade. It's ironic that the shale crisis is likely to be responsible for triggering Peak Oil Supply. In an excellent op/ed, vice chairman of IHS Markit Dan Yergin observes that it's almost inevitable that shale output will go in reverse and decline thanks to drastic cutbacks in investment and only later recover at a slow pace. Shale oil wells decline at an exceptionally fast clip and therefore require constant drilling to replenish lost supply. Indeed, Norway-based energy consultancy Rystad Energy recently warned that Big Oil could see its proven reserves run out in less than 15 years, thanks to produced volumes not being fully replaced with new discoveries. According to Rystad, proven oil and gas reserves by the so-called Big Oil companies, namelyExxonMobil (NYSE:XOM) (-0.42%), BP Plc. (NYSE:BP) (-0.15%), Shell (NYSE:RDS.A)(-0.44%), Chevron (NYSE:CVX) (0.26%), Total (NYSE:TOT) (-0.60%), and Eni S.p.A (NYSE:E) (0.29%) are all falling, as produced volumes are not being fully replaced with new discoveries.

Source: Oil and Gas Journal Last year alone, massive impairment charges saw Big Oil's proven reserves drop by 13 billion boe, good for ~15% of its stock levels in the ground, last year. Rystad now says that the remaining reserves are set to run out in less than 15 years unless Big Oil makes more commercial discoveries quickly. The main culprit: Rapidly shrinking exploration investments. Global oil and gas companies cut their capex by a staggering 34% in 2020, in response to shrinking demand and investors growing weary of persistently poor returns by the sector. The trend shows no signs of moderating: First quarter discoveries totaled 1.2 billion boe, the lowest in 7 years with successful wildcats only yielding modest-sized finds as per Rystad. ExxonMobil, whose proven reserves shrank by 7 billion boe in 2020, or 30%, from 2019 levels, was the worst hit after major reductions in Canadian oil sands and US shale gas properties. Shell, meanwhile, saw its proven reserves fall by 20% to 9 billion boe last year; Chevron lost 2 billion boe of proven reserves due to impairment charges while BP lost 1 boe. Only Total and Eni have avoided reductions in proven reserves over the past decade. Yet, policy changes by Biden's administration, as well as fever-pitch climate activism, are likely to make it really hard for Big Oil to go back to its trigger-happy drilling days, meaning U.S. shale could really struggle to return to its halcyon days. By Alex Kimani for Oilprice.com

oilprice.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)