Send this article to a friend:

July

13

2020

|

Send this article to a friend: July |

|

The Fed Is Trapped In QE As Interest Rates Can’t Rise Ever Again.

As we discussed previously, Jeremy Siegel already declared the end to the 40-year bond bull market.

However, this is not a new sentiment, but it has existed since I started calling for rates to fall below 1% as far back as 2013. The reasoning then, and is the same today, is the linkage between the debt and economic growth.

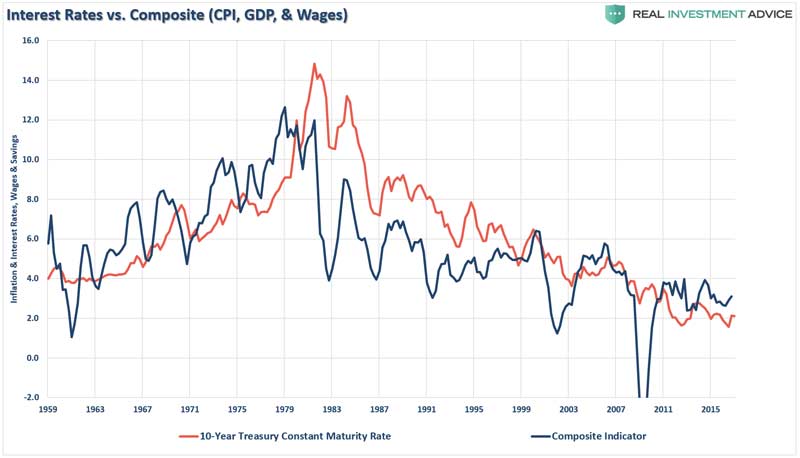

It’s The Economy Stupid Interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship between the composite index compared to the level of the 10-year Treasury rate is below.

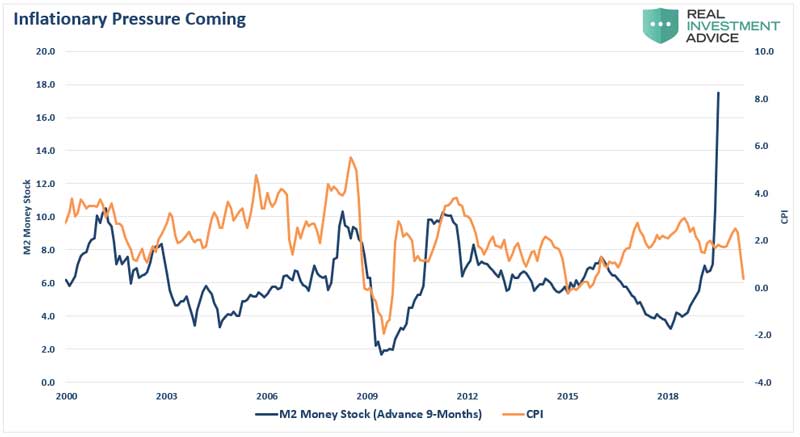

As shown, the level of interest rates correlates to the strength of economic growth and inflation. Since wage growth allows individuals to consume, which makes up roughly 70% of economic growth, the demand for borrowing is a function of the need for consumption. But therein lies the trap – inflation. The Fed Inflation Trap While “deflation” is the overarching threat longer-term, the Fed is also potentially confronted by a shorter-term “inflationary” threat. The “unlimited QE” bazooka is dependent on the Fed needing to monetize the deficit to support economic growth. However, if the goals of full employment and economic growth quickly come to fruition, the Fed will face an “inflationary surge.”

Should such an outcome occur, it will push the Fed into a very tight corner. The surge in inflation will limit the ability to continue “unlimited QE” without further exacerbating inflation. Unfortunately, if they don’t “monetize” the deficit through the “QE” program, interest rates will surge as the Treasury issues more debt. It’s a no-win situation for the Fed. The Worst Thing Ever If interest rates rise for any reason, such is when the “wheels come off the cart.”

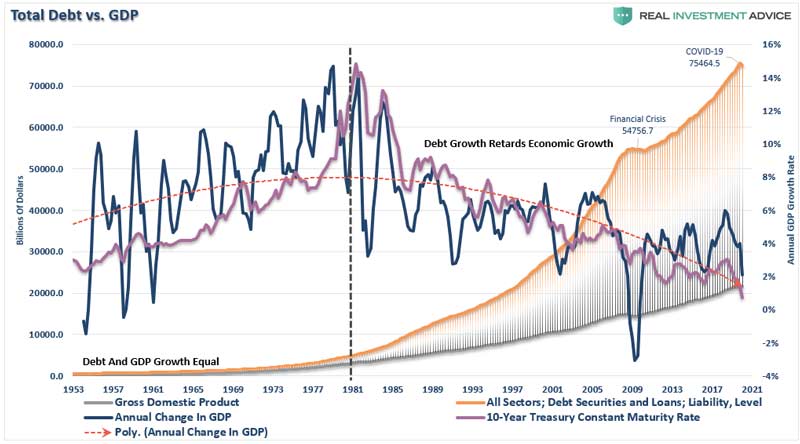

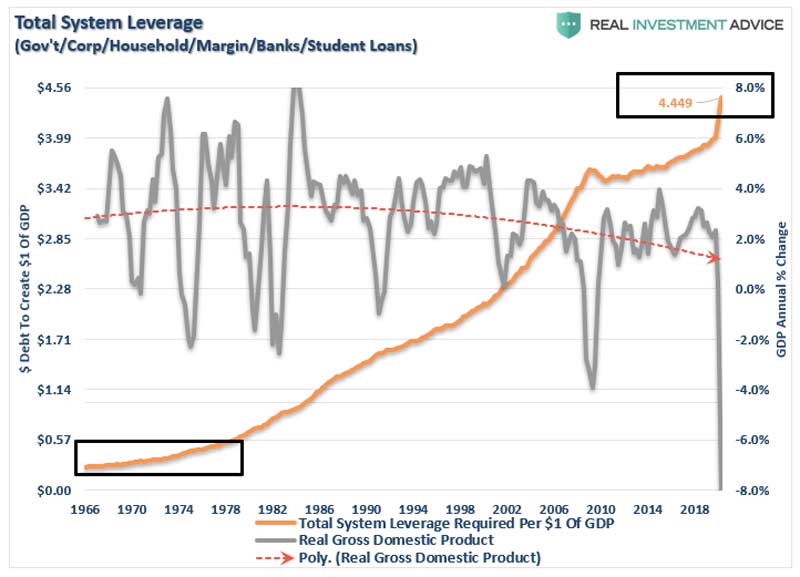

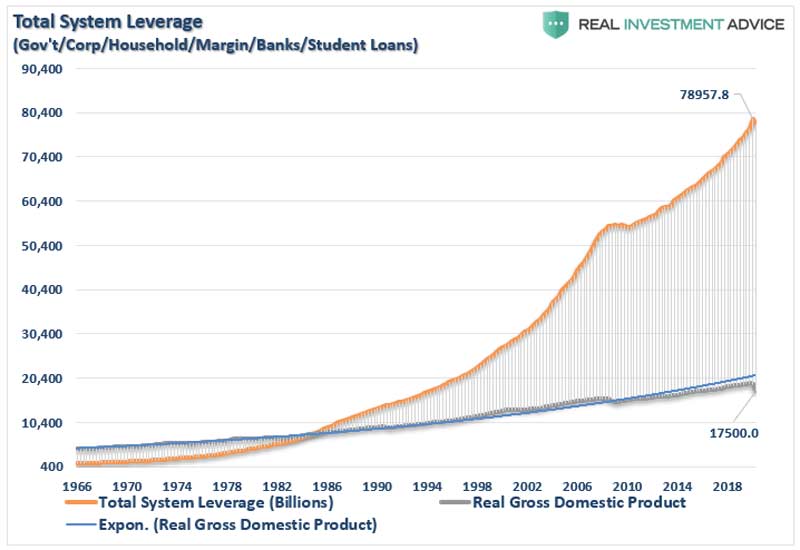

I could go on, but you get the idea. Putting It In Pictures The ramifications of rising interest rates apply to every aspect of the economy. As rates rise, so do rates on credit card payments, auto loans, business loans, capital expenditures, leases, etc., while corporate profitability is reduced. Currently, the economy requires in excess of $4.00 in debt to manufacture $1.00 of economic growth. Given the dependence on debt to fund growth, higher interest rates would be inherently destructive.

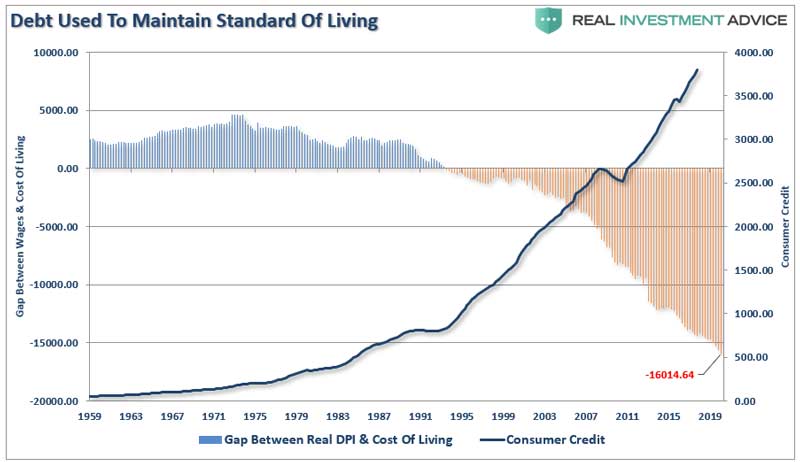

More importantly, consumers have sunk themselves deeper into debt as well. Currently, the gap between wages and the costs of supporting the required “standard of living” is at a record. With a requirement of over $16,000 in debt to maintain living standards, there is little ability to absorb higher rates before it drastically curbs consumption.

The Fed Has No Choice Given the amount of debt currently required to sustain current economic growth, the Fed has no choice but to continue monetization of the Federal debt indefinitely. Such leaves only TWO possible outcomes from here, both of them are not good

The Fed’s Trapped At Zero The debt problem exposes the Fed’s risk and why they are now forever trapped at the zero-bound. The Fed has stated interest rates will remain low until “such time as the dual mandates of full employment and price stability achieved.” Given economic stability was not achieved in the last decade, it is highly unlikely a more than doubling of the Fed’s balance sheet will improve future outcomes. Unfortunately, given we now have a decade of experience of watching the “wealth gap” worsen under the Federal Reserve’s policies, the next decade will only see the “gap” widen. We now know that surging debt and deficits inhibit organic growth. The massive debt levels added to the backs of taxpayers will only ensure the Fed remains trapped at the zero-bound.

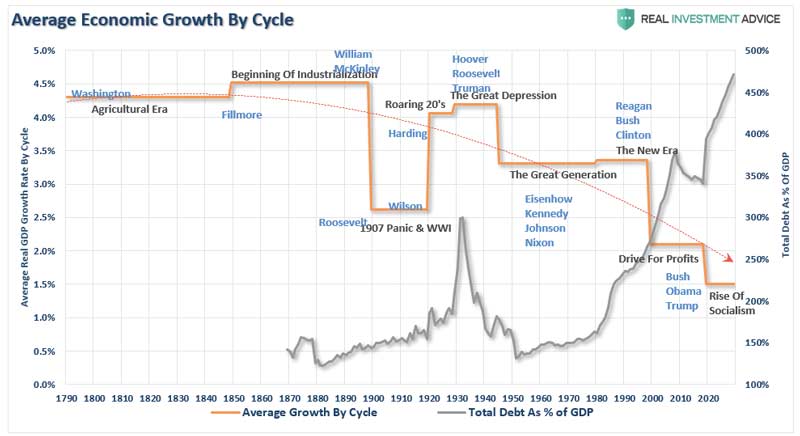

Rates Can’t Rise Ever However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter. Since interest rates affect “payments,” increases in rates quickly negatively impact consumption, housing, and investment, which ultimately deters economic growth. Given the current demographic, debt, pension, and valuation headwinds, the future growth rates will be low over the next couple of decades. Even the Fed’s own “long-run” economic growth rates currently run below 2%. The catalysts needed to create the type of economic growth required to drive interest rates substantially higher, as we saw before 1980, are not available today. Nor will they be in the future. Ultimately, the Federal Reserve, and the Administration, will have to face hard choices to extricate the economy from the current “liquidity trap.” However, history shows that political leadership ever makes the choices, until the choices are forced upon them. You don’t have to look much further than Japan for a clear example of what I mean.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)