Send this article to a friend:

June

08

2023

|

Send this article to a friend: June |

|

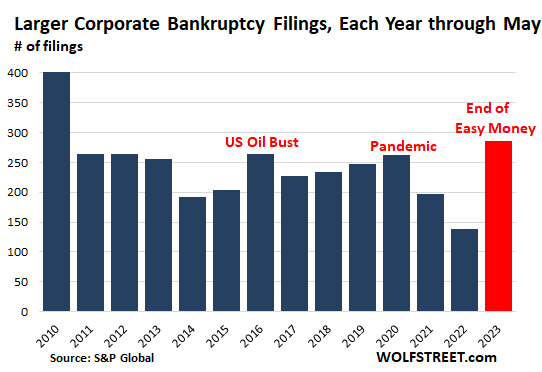

The End of Easy Money: Bankruptcy Filings Pile Up at Fastest Rate since 2010

It’s turning into a banner year for corporate bankruptcy filings, after years of Easy Money that caused all kinds of excesses, fueled by yield-chasing investors, in an environment where the Fed had repressed yields with all its might. Those yield-chasing investors kept even the most over-indebted zombies supplied with ever-more fresh money. But that era has ended. Interest rates are much higher, and investors are getting a little more prudent, and Easy Money is gone. At the peak of the Fed’s yield repression in mid-2021, “BB”-rated companies – so these companies are “junk” rated – could borrow at around 3% (my cheat sheet for corporate credit rating scales by ratings agency). Companies are junk rated because they have too much debt and inadequate cash flow to service that debt. In other words, investors risked life and limb to earn 3%, and now these investors are asked to surrender life and limb, so to speak. But that’s how it goes with yield-chasing. These “BB” junk bond yields have risen to nearly 7%. This means these companies that had trouble producing enough cash flow to service their 3% or 5% debt, have to refinance this debt when it comes due, or add new debt, at 7%. That 7% may still be low, considering inflation running around near that neighborhood, but it puts a lot more strain on those companies. So lots of overindebted junk-rated companies will restructure their debts in bankruptcy court at the expense of stockholders, bondholders, and holders of their leveraged loans. That’s how it’s supposed to work. That’s how the corporate-debt burden gets lifted off the economy. And it’s starting to work that way. S&P Global has released its May bankruptcy statistics for companies that are publicly traded with at least $2 million in assets or liabilities listed in their bankruptcy filings, and private companies with publicly traded debt (such as bonds) with at least $10 million in assets or liabilities listed in their bankruptcy filings. In May, 54 of these types of companies filed for bankruptcy, including notably, among the big ones:

The May filings brought the five-month total to 286 bankruptcy filings, the most since 2010, more than double the filings for the same period in 2022 (138). And it even outran the 262 filings in the same period in 2020 when some companies faced enormous stress. When the oil bust exacted its pound of flesh in 2016, and oil and gas drillers collapsed one after the other, S&P Global recorded 265 filings, but concentrated in oil and gas. To get a higher number of filings than in the first five months of 2023, we have to go back to 2010, when 402 companies filed for bankruptcy during the first five months.

Among the biggest bankruptcies included in this illustrious list so far this year that made it into my pantheon of Imploded Stocks were:

The problem today is not a collapse in prices – such as the price of oil during the Oil Bust of 2016 when crude oil grade WTI collapsed below $20 a barrel that took dozens of frackers down; WTI is at $72 a barrel today! And the problem today is not a collapse in demand such as it hit some industries in 2020 or during the Great Recession. This economy is marked by rising prices and resilient demand. The problem now is that the debt got a lot more expensive, and that investors thinking of buying this debt have gotten a little more prudent. The problem is the End of Easy Money. Once companies get hooked on Easy Money by having piles of debt, it’s tough to get by without Easy Money. In a way, the economy is normalizing with rates that were fairly typical before the era of QE. But companies that only made it this far thanks to Easy Money are now getting hung out to dry. Bankruptcy filings will whittle down the corporate debt overhang. Many companies will emerge from bankruptcy with less debt, and they’ll be nimbler and more able to thrive. Others will be sold off in bits and pieces, making room for appropriately managed companies not encumbered by these issues. There is a cleansing aspect to this part of the credit cycle that needs to be allowed to do its job to get rid of the excesses and the deadwood at the expense of investors. This cleansing process that has now just started is long overdue. Hilariously, the end of Easy Money is now called credit crunch. Which should be the name of a candy bar (Credit Crunch®) offered to the crybabies on Wall Street as consolation when they start clamoring for rate cuts. Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)