The Coming Crisis

Darryl Robert Schoon

“Deep down in our hearts, we know that we have bankrupted America and that we have given our children a legacy of bankruptcy. We have defrauded our country to get ourselves elected.” – Senator John C. Danforth (MO-R), April 22, 1992

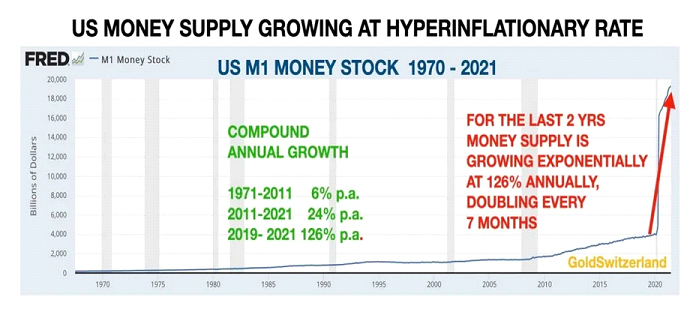

The debate on raising the debt limit was akin to deciding whether a patient should continue a fatal regimen of steroids, i.e., excessive money printing. Since the 2008 financial crisis, only excessive money printing—free credit to banks at 0.0 to 0.25 % interest and unprecedented infusions of cash (over four trillion dollars in quantitative easing)—has kept the US economy alive.

The cost of doing so, however, is not measured by the cost of credit or cash debited on the Fed’s ballooning balance sheet. Like steroids, excessive money printing is eventually fatal as the requisite balance between credit and debt becomes so distorted capital markets can no longer function.

Eight years after the 2008 financial crisis, in 2016 the Fed attempted to reduce its excessive money printing but soon found that even small increases in the cost of credit caused the US economy to slow—and, at slow speed, capital markets, like bicycles, perform poorly.

In 2020, because of covid-lockdowns, the Fed reverted to extreme monetary measures, e.g. zero percent interest rates and exponentially expanding the money supply, to keep the economy from again collapsing.

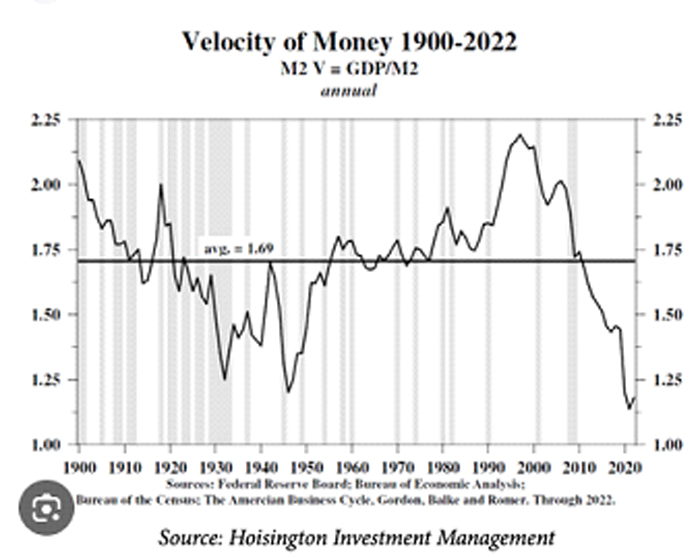

Such extreme measures were necessary to prevent the economy from succumbing to a severe deflationary contraction. The velocity of money, a measure of economic activity, had plunged to levels even lower than during the 1930’s Great Depression.

The historic expansion of the money supply in 2020 reawakened inflationary forces; and the Fed raised interest rates to prevent rapidly expanding inflation from turning into hyper-inflation, a monetary phenomenon responsible for the collapse of economies and governments since the invention of fiat money in 1024, see Ralph Terry Foster’s Fiat Paper Money: The History and Evolution of Our Currency.

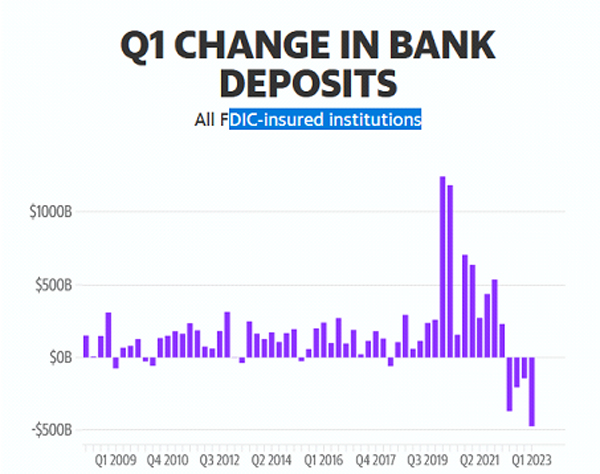

In 2022, because of the Fed’s rising interest rates, speculative bubbles in stocks, bonds, cryptocurrencies and real estate, inflated by the Fed’s excessive money-printing, began to collapse as did commercial banks, e.g., Silicon Valley Bank, Signature Bank and First Republic Bank, when the debate on raising the debt-limit began.

The subsequent decision to raise the debt limit was not so much a sign of increasingly rare cooperation between Republicans and Democrats as it was the unspoken acknowledgement by both parties that the economic tides threatening America had become exceptionally treacherous.

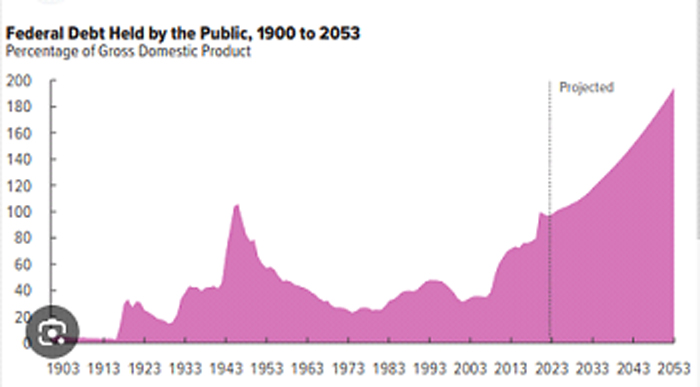

Both parties knew the patient—aged and bloated, encumbered with aggregate levels of debt incapable of ever being repaid and technically bankrupt—was incapable of withstanding more endogenous shocks, i.e., more bank failures, let alone a catastrophic exogenous shock, i.e., the political inability to pay its bills; and, accordingly, politicians voted to allow the financially fatal regimen of monetary steroids to continue.

How We Got Here

“The central bank is an institution of the most-deadly hostility existing against the Principles and form of our Constitution. I am an Enemy to all banks discounting bills or notes for anything but Coin [gold and silver coins]. If the American People allow private banks to control the issuance of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the People of all their Property until their Children will wake up homeless on the continent their Fathers conquered.” – Thomas Jefferson, 1814

In 1913, almost one hundred years after Thomas Jefferson wrote those words, the US allowed The Federal Reserve Bank, a central bank, to replace the US Treasury as the issuer of the US dollar. The US dollar became a conveyance of debt and United States of America, a nation of debtors.

As Thomas Jefferson warned, should private bankers prevail …the banks and corporations that will grow up around them will deprive the People of all their Property until their Children will wake up homeless…

Today, Jefferson’s words have come true. …Hundreds of thousands of single-family homes are now in the hands of giant companies — squeezing renters for revenue and putting the American dream even further out of reach. – New York Times, A $60 Billion Housing Grab by Wall Street, March 4, 2020

In mobile home parks around the country, millions of tenants and owners are being mercilessly exploited and regularly evicted, often by giant Wall Street firms like Blackstone. – Jacobin, Wall Street Is Holding a Gun to Mobile Home Residents’ Heads, May 2023

Note: Central banking originated in the United Kingdom

In the bankers’ ponzi-scheme of credit and debt, banks take the savings of depositors, pay a nominal rate for its use and then can loan over 10 times the amount of those deposits to those who deposited their savings and others at interest rates far above the interest paid on their savings, see my article, Make Millions By Loaning Money That’s Not Even Yours That You Don’t Even Have—It’s All Legal Too.

In 2023, however, depositors began withdrawing their savings from banks, the very cotter-pin of banking’s societal tyranny.

Today, banks are in trouble, economies are in a state of distress, homelessness is increasing as are extreme weather events, democratic institutions are under attack, the influence of dictators grows and nuclear war is a possibility

What will happen next?

The Coming Crisis – Rising Prices, Economic and Political Collapse and the Emergence of a New and Better World

Professor David Hackett Fisher observed that price revolutions, i.e., waves of rising prices, end in the collapse of historical epochs, e.g., the Middle Ages, the Renaissance, the Enlightenment, etc. followed by new, more equitable eras.

All major price revolutions in modern history began in periods of prosperity. Each ended in shattering world-crises and were followed by periods of recovery and comparative equjlibrium.

p.9, The Great Wave: Price Revolutions and the Rhythm of History, David Hackett Fischer, Oxford University Press, 1996

According to Professor Fisher, today’s price-revolution will bring about the collapse of The Era of Victorian Equilibrium, an equilibrium brought about by England’s ability to wage war on credit, gratis the Bank of England, a central bank.

Central banking, an inherently unstable system of vast potential, played a major role in world events for over three centuries. Today, however, it is in disarray; for we are approaching the culmination of another great wave of rising prices which will bring banking’s extraordinary run at the table of luck to a devastating close.

The present great wave of rising prices shares characteristics with all price-revolutions. In each of the prior price-revolutions, Professor Fisher noted:

Food and fuel led the upward movement. Manufactured goods and services lagged behind. These patterns indicated that the prime mover was excess aggregate demand, generated by an acceleration of population growth, or by rising living standards, or both.

… prices went higher, and became increasingly unstable. They began to surge and decline in movements of increasing volatility. Severe price-shocks were felt in commodity movements. The money supply was alternately expanded and contracted. Financial markets became unstable. Government spending grew faster than revenue, and public debt increased at a rapid rate.

In every price-revolution, the strongest nation-states suffered severely from fiscal stresses: Spain in the sixteenth century, France in the eighteenth century, and the United States in the twentieth century.

Wages, which had at first kept up with prices, now lagged behind. Returns to labor declined while returns to land and capital increased. The rich grew richer. Inequalities of wealth and income increased. So did hunger, homelessness, crime, violence, drink, drugs, and family disruption. – pp. 237-238

Today, we are again in the final stage of another great wave, a stage that will culminate in the collapse of the present world.

“Humanity is moving ever deeper into crisis—a crisis without precedent.” – Buckminster Fuller, Critical Path, 1981

The introduction to Critical Path, Buckminster Fuller’s advice to humanity, is titled Twilight of the World’s Power Structures. Fuller believed the collapse of today’s economic, political and religious power structures was a pre-requisite to a better world; that their collapse in a crisis without precedent would bring to an end the present era and the emergence of a new and far-better world.

Fuller predicted this far-better world—a world of cooperation, abundance and peace—would be opposed not only by today’s power structures but by those fearful of change. …There are millions in the U.S.A., for instance, who…would become activist “patriots,” and might get out their guns and start a Nazi movement, seeking dictatorially to reinstate the “good old days.”

p. 217, Critical Path, Buckminster Fuller, St. Martin’s Press, 1981

The collapse of Silicon Valley Bank ($212 billion in assets), Signature Bank ($110 billion in assets), First Republic Bank ($229 billion in assets) and the forced reorganization of Credit Suisse ($1.4 trillion in assets) are but portents of the coming cataclysmic crisis.

Then, it will get better.

In Time of the Vulture (2007), www.survivethecrisis.com, I predicted a severe economic crisis was about to happen. In 2023, that crisis is now entering its final stage.

In times of expansion, it is to the hare the prizes go. Quick, risk taking, and bold, his qualities are exactly suited to the times. In periods of contraction, the tortoise is favored. Slow and conservative, quick only to retract his vulnerable head and neck, his is the wisest bet when the slow and sure is preferable to the quick and easy.

Every so often, however, there comes a time when neither the hare nor the tortoise is the victor. This is when both the bear and the bull have been vanquished. When the pastures upon which the bull once grazed are long gone and the bear’s lair itself lies buried deep beneath the rubble of economic collapse.

This is the time of the vulture. For the vulture feeds neither upon the pastures of the bull nor the stored-up wealth of the bear. The vulture feeds instead upon the blind ignorance and denial of the ostrich. The time of the vulture is at hand.

My new book¸ Docking At The Mothership: Notes On Going Home (2022), gives the metaphysical reasons for today’s transformative crisis and what will be necessary to survive it. These are most interesting times—and, they are about to become even more so.

Buy gold, buy silver, have faith

Darryl Robert Schoon

www.drschoon.com

In college, I majored in political science with a focus on East Asia (B.A. University of California at Davis, 1966). My in-depth study of economics did not occur until much later.

In the 1990s, I became curious about the Great Depression and in the course of my study, I realized that most of my preconceptions about money and the economy were just that - preconceptions. I, like most others, did not really understand the nature of money and the economy. Now, I have some insights and answers about these critical matters.

In October 2005, Marshall Thurber, a close friend from law school convened The Positive Deviant Network (the PDN), a group of individuals whom Marshall believed to be "out-of-the-box" thinkers and I was asked to join. The PDN became a major catalyst in my writings on economic issues.

When I discovered others in the PDN shared my concerns about the US economy, I began writing down my thoughts. In March 2007 I presented my findings to the Positive Deviant Network in the form of an in-depth 148-page analysis, "How to Survive the Crisis and Prosper In The Process."

The reception to my presentation, though controversial, generated a significant amount of interest; and in May 2007, "How To Survive The Crisis And Prosper In The Process" was made available at www.survivethecrisis.com and I began writing articles on economic issues.

The interest in the book and my writings has been gratifying. During its first two months, www.survivethecrisis.com was accessed by over 10,000 viewers from 93 countries. Clearly, we had struck a chord and www.drschoon.com, has been created to address this interest.

drschoon.com

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)