Send this article to a friend:

June

25

2021

|

Send this article to a friend: June |

|

Social Security Under Pressure Thanks to These 3 Economic Trends

It’s the same program you have plunked your hard-earned dollars into, in the form of mandatory payroll taxes, over decades of work. Maybe we shouldn’t call them your hard-earned dollars, though. Because once that money goes to Social Security, it’s not yours anymore. As the SSA states very clearly:

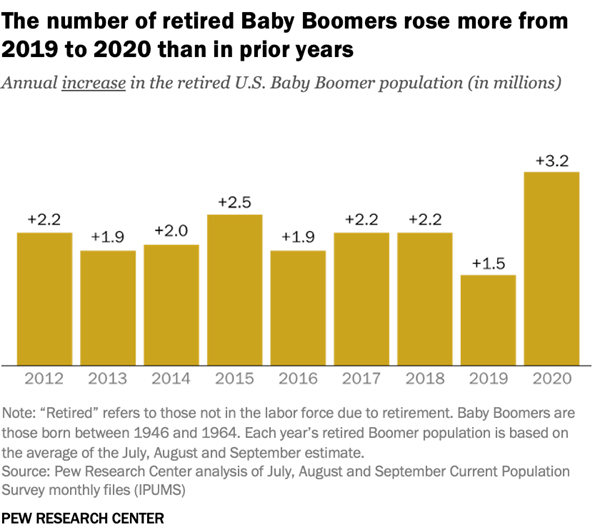

Regardless of where the money comes from or whose name is on it, it’s running out. So let’s take a quick look at each of the big economic trends happening today, and how they’re taking a toll on Social Security even as you read this. #1 – People are retiring at a faster pace According to Forbes’s Bob Carlson, “In September 2020, about 3.2 million more baby boomers were retired than a year earlier.” It’s quite likely that the COVID-19 pandemic played a role here, and Carlson’s source, the Pew Research Center report, shows over 50% more Baby Boomer retirements than 2019. There were also more of those retirements in 2020 than any year since 2012 (see bar graph):

Carlson came to a startling conclusion for Social Security:

People retiring sooner than expected leaves fewer people paying into Social Security, so that’s a fairly obvious conclusion. We won’t know what the specific impact will be until that annual report for 2021 is released. Still, it’s not positive news. When we consider our next big development, you’ll see there are even fewer people paying into the system… #2 – The ideas of work and retirement are changing According to Ramsey Solutions: “Retirement isn’t an age — it’s a financial number. And there’s no law that says you have to work until you’re 65. That’s a myth!” That’s your two-sentence introduction to the F.I.R.E. (Financial Independence, Retire Early) movement. The article continues by explaining what this means:

To be sure, this is an extreme movement: super-low living costs, simple lifestyles, stringent and zealous savings goals. Those who are successful are problematic, at least from a Social Security perspective. A successful F.I.R.E. will effectively sit out their peak earning years, denying the SSA their tax dollars. On the other hand, they will also have a smaller claim on future Social Security payments. (That’s not quite as important, because “We use your taxes to pay people who are getting benefits right now,” remember?) Couple F.I.R.E with another trend called the “gig economy” where workers make a living doing lots of little jobs rather than a single, full-time job. Think of an Uber or Lyft driver, an AirBnB host or a freelance writer to get the idea. The F.I.R.E. movement is big on gig work:

If people live on less, they are earning less in exchange for more free time. That means less payroll tax generated per gig worker. That certainly won’t help the Social Security Trust fund its obligations much, even if the gig workers all scrupulously report every dollar of income and pay their 15.3% self-employment tax. Which brings us to the final economic force challenging Social Security over the next few years (at least)… #3 – Rates, Rates, and More Rates Rising inflation doesn’t only erode your purchasing power, it presents challenges to the Social Security program too. Couple that with a lower real rate of return (interest minus inflation) for the Trust Fund’s U.S. bond portfolio, at the moment at least-1.5%. That’s the opposite of return on investment. If you’re not too depressed to keep reading, it gets worse. Economist Mike Shedlock calculates inflation rates adjusted for increased housing costs. His numbers put the real rate of return is -4.1% (the lowest since 1980). Regardless of your method of calculating the real rate of return, it’s negative. The money in the SSA trust fund is losing purchasing power every day. That’s simply not sustainable. And it’s a red flag for those of us counting on Social Security to ease the transition into our golden years. Social Security May Be in Trouble, But You Don’t Have to Be With stormy waters ahead for Social Security thanks to these 3 newer forces, a fresh perspective is sorely needed. Granted, a collapse of Social Security won’t happen overnight. First we’d expect a series of warnings, then payment cuts amid a lot of panic over what so many retirees think of as a certainty evaporating before their eyes. We can’t solve Social Security’s problems. Instead, we encourage you to educate yourself about your retirement options. It might be time to rethink your retirement savings. Examine your allocations, consider your risk levels, and consider adding physical precious metals such as gold and silver. They could store enough value to give you your own “safety net” should Social Security fail to deliver on its promises.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)