Send this article to a friend:

June

12

2021

|

Send this article to a friend: June |

|

Bitcoin Is De-dollarization. Ethereum Is DeFi-nancialization

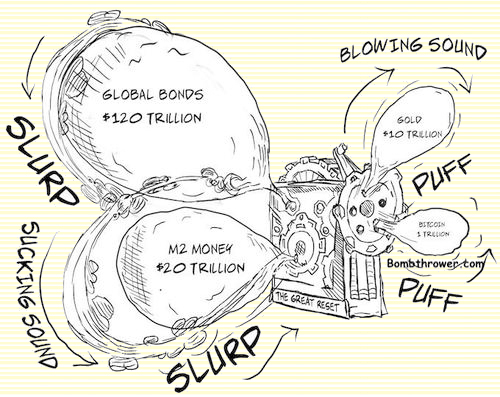

Behind the FUD we see actions. We see Russia dumping dollar assets (can you blame them?). We hear Munger making almost childishly uninformed remarks on crypto, yet BRK is investing in one of the world’s most crypto friendly banks. We see El Salvador as the first country in the world to make Bitcoin legal tender. In my mind this has not only sounded the starting gun on de-dollarization in earnest, it goes beyond that. Back in the late 90‘s people like me were about the age of many of the crypto kids today, and we were talking about the Internet Asteroid headed straight at the telecoms and traditional media. Today, pretty well everybody is aware of Bitcoin. They may have positive or negative opinions on it, but most people are figuring out that it’s here to stay and there is a spectrum of sentiment around that ranging from enthusiasm to denial. But I don’t get the sense that traditional institutional finance sector sees the other asteroid coming, and it’s coming straight at them. The new 60/40 portfolio will mean Bitcoin/Ethereum Or maybe Ethereum/Bitcoin. Whatever your risk tolerance and investment objectives entail. I’ve been listening to the Bankless podcast lately and in more than one episode they’ve said something about Bitcoin as compared to Ethereum that I think is very helpful. It’s really helped me think about the two in terms of construction of a crypto portfolio. They’ve said, in essence, that Bitcoin is for when you’re bearish on society and Ethereum is for when you’re bullish. It’s not that I agree with that literally (I don’t), but it really helped me refine the distinction I’ve always had around Bitcoin being the value and Ethereum being the execution in a coming tectonic shift into crypto. In the olden days, bonds and equities had an inverse correlation. Bonds kept your portfolio afloat when the economy hit a soft patch and stocks went down (yes, in the olden days, stocks could experience bear markets, sometimes for months or even years). Conventional wisdom was to have a portfolio mix between equities and bonds, along some rule of thumb like 60/40 adjusted for your age, risk tolerance, etc. We’re headed into a world where Bitcoin and Ethereum will fulfil the roles that bonds and equities did traditionally. The basic thesis of my Crypto Capitalist Letter is that Bitcoin will be on the receiving end of an impending mother-of-all wealth-transfers. Many Bitcoiners think that if Bitcoin is “digital gold” then that means the incoming funds flow will be from the 10 Trillion dollar gold market. I think this is wrong. Bitcoin’s looming funds inflow isn’t going to come from gold. Maybe some will, maybe some shorter term gold holders will jump ship to Bitcoin in much the same way that this latest down cycle since April has been driven largely by younger coins (weaker hands) selling out. (Overall I think gold and silver will also be on the receiving end of this great transfer). But Bitcoin’s inflow will come largely from the more than ten times larger bond market. Not gold. Not 10 Trillion. 120 Trillion, of which 20 trillion of it already yields negative returns ( “return free risk”). A simple layer 1 Bitcoin lending program with an institutional level custodian like Gemini or Galaxy (whom we hold in our TCC portfolio) would yield 400 basis points right there, and that’s without even counting the price appreciation.

“The TAM is Everything” But what I didn’t realize until the Bankless panel this week about the current state of DeFi is that there’s another 100 Trillion-plus market, and it’s going to be sending its value in a parallel mother-of-all wealth transfers. That wealth transfer is the flight of assets from the traditional banking system into Ethereum and into DeFi. In my mind this is what DeFi actually means. Where financialization is the widespread hollowing out of all value and turning it into multiple layers of rehypothecated debt, DeFi is De-Financializing assets. DeFi is where money gets intelligence and value can compound and where tokenized assets increase their purchasing power over time. It’s where savers are rewarded, instead of penalized and demonized. It’s where capital formation is possible.

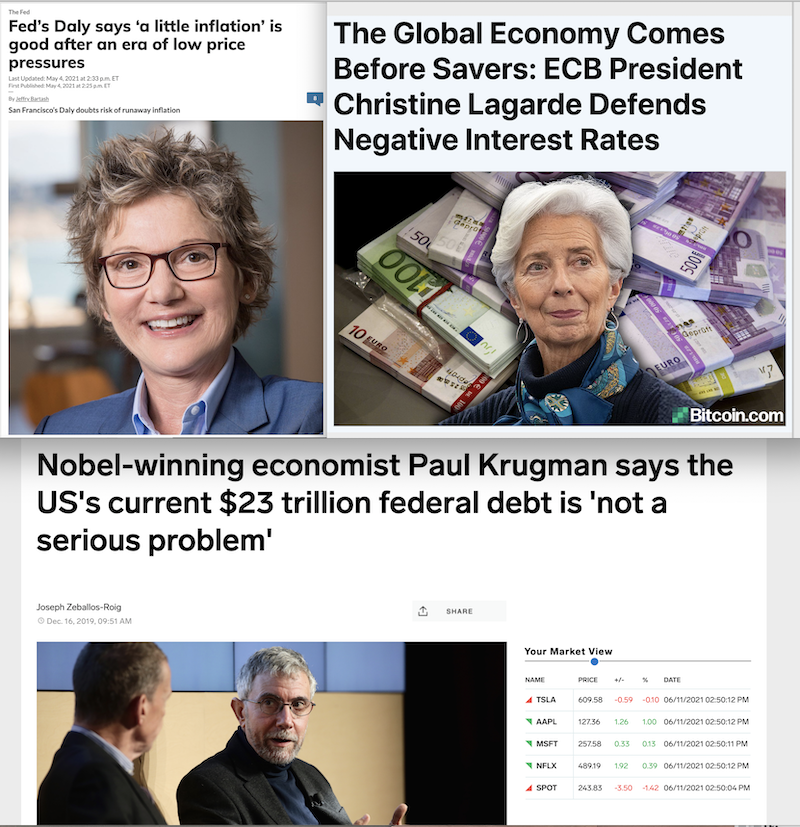

Most institutions won’t be making this transformation. The majority of them will gravitate toward the Central Bank Digital Currencies (CBDCs), which as we say in The Crypto Capitalist Manifesto, CBDCs will be specifically constructed to preclude savings, make capital formation impossible and will be a honeypot of dependancy for the masses who allow their economic lives to be bounded by them. But many of those institutional clients, the ones that see The Great Bifurcation coming, will make this shift, and they’ll bring their capital with them.

I see this playing out in real time in the world and in my personal experience, here’s three quick data points

It is this is the type of institutional lethargy that is all tailwind and gasoline for DeFi. In the case of the forex hedges, I’m now looking at places like Synthetix and hiring a smart contract developer to simply create the hedges for me. The way I envision it, anybody would be able to earn a return on their assets by staking the liquidity pool for USD/CAD, and Canadian businesses with exposure to USD currency weakness would be able to easily hedge for that without pledging their house (if you know anybody who can help me out here, my DM’s are open). I’m cancelling that credit card and getting set up with one of the many new crypto backed credit cards that give you cash back on every purchase in crypto. One of the reasons people are skeptical of crypto and fool themselves into thinking it’s some kind of passing fad (“ponzi” or the negligently uninformed “tulips”) is because this is happening so fast. In realtime. (They didn’t read Future Shock back in the 70’s, 80’s or 90’s or if they did, they either forgot about it or didn’t fully understand what it meant).

* * * To receive future posts in your mailbox join the free Bombthrower mailing list, follow me on Twitter, Mastodon or join the Bombthrower telegram

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)