Send this article to a friend:

June

28

2018

|

Send this article to a friend: June |

|

A New Global Debt Crisis Has Begun

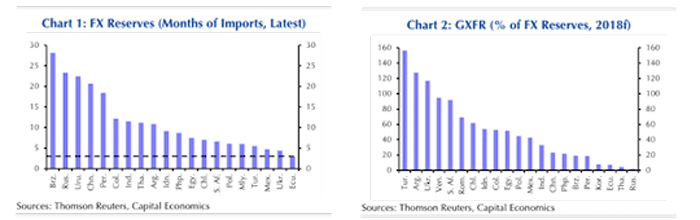

In recent decades, the first crisis in this series was the Latin American debt crisis of 1982–85. The combination of inflation and a commodity price boom in the late 1970s had given a huge boost to economies such as Brazil, Argentina, Chile, Mexico and many others, including countries in Africa. This commodity boom enabled these emerging-market (EM) economies to earn dollar reserves for their exports. (By the way, we didn’t call them “emerging markets” in the 1980s; they were the “Third World” after the Western world and the communist world.) These dollar reserves were soon supplemented with dollar loans from U.S. banks looking to “recycle” petrodollars that the OPEC countries were putting on deposit after the oil price explosion of the 1970s. I worked at Citibank from 1976–1985 during the height of petrodollar recycling and even discussed the process personally with Walter Wriston, Citibank’s legendary CEO. In the 1960s, Wriston invented the negotiable eurodollar CD, which was later critical to funding those EM loans. Wriston is considered the father of petrodollar recycling once the petrodollar was created by Henry Kissinger and William Simon under President Nixon in 1974. I remember those days extremely well. The bank made billions and our stock price soared. It was a euphoric phase and a great time to be an international banker. Then it all crashed and burned. One by one, the lenders defaulted. They had squandered their reserves on vanity projects such as skyscrapers in the jungle, which I saw firsthand when I visited Kinshasa on the Congo River in central Africa. Most of what wasn’t wasted was stolen and stashed away in Swiss bank accounts by kleptocrats. Citibank was technically insolvent after that but was bailed out by the absence of mark-to-market accounting. We were able to pretend the loans were still good as long as we could refinance them or roll them over in some way. Citibank has a long and glorious history of being bailed out, stretching from the 1930s to the 2010s. After the defaults, the reaction set in. Emerging markets had to flip to austerity, devalue their currencies, cut spending, cut imports and gradually rebuild their credit. There was a major EM debt crisis in Mexico in 1994, the “Tequila Crisis,” but that was contained by a U.S. bailout led by Treasury Secretary Bob Rubin. On the whole, the EMs used the 1990s to rebuild reserves and restore their creditworthiness. Gradually, the banks looked favorably on this progress and new loans started to pour in. Now the target of bank lending was not Latin America but the “Asian Tigers” (Singapore, Taiwan, South Korea and Hong Kong) and the “mini-tigers” of South Asia. The next big EM debt crisis arrived right on time in 1997, 15 years after the 1982 Latin American debt crisis. This one began in Thailand in June 1997. Money had been flooding into Thailand for several years, mostly to build real estate projects, resorts, golf courses and commercial office buildings. Thailand’s currency, the baht, was pegged to the dollar, so dollar-based investors could get high yields without currency risk. Suddenly a run on the baht emerged. Investors flocked to cash out their investments and get their dollars back. The Thai central bank was forced to close the capital account and devalue their currency, forcing large losses on foreign investors. This sparked fear that other Asian countries would do the same. Panic spread to Malaysia, Indonesia, South Korea and finally Russia before coming to rest at Long Term Capital Management, LTCM, a hedge fund in Greenwich, Connecticut. I was chief counsel to LTCM and negotiated the rescue of the fund by 14 Wall Street banks. Wall Street put up $4 billion in cash to prop up the LTCM balance sheet so it could be unwound gradually. At the time of the rescue on Sept. 28, 1998, global capital markets were just hours away from complete collapse. Emerging markets learned valuable lessons in the 1997–98 crisis. In the decade that followed, they built up their reserve positions to enormous size so they would not be disadvantaged in another global liquidity crisis. These excess national savings were called “precautionary reserves” because they were over and above what central banks normally need to conduct foreign exchange operations. The EMs also avoided unrealistic fixed exchange rates, which were an open invitation to foreign speculators like George Soros to short their currencies and drain their reserves. These improved practices meant that EMs were not in the eye of the storm in the 2007–08 global financial crisis and the subsequent 2009–2015 European sovereign debt crisis. Those crises were mainly confined to developed economies and sectors such as U.S. real estate, European banks and weaker members of the eurozone including Greece, Cyprus and Ireland. Yet memories are short. It has been 20 years since the last EM debt crisis and 10 years since the last global financial crisis. EM lending has been proceeding at a record pace. Once again, hot money from the U.S. and Europe is chasing high yields in EMs, especially the BRICS (Brazil, Russia, India, China and South Africa) and the next tier of nations including Turkey, Indonesia and Argentina. As Chart 1 and Chart 2 below illustrate, we are now at the beginning of the third major EM debt crisis in the past 35 years. Chart 1 measures the size of hard-currency reserves relative to the number of months of imports those reserves can buy. This is a critical metric because emerging markets need imports in order to generate exports. They need to buy machinery in order to engage in manufacturing. They need to buy oil in order to keep factories and tourist facilities operating. Chart 1 shows how many months each economy could pay for imports out of reserves if export revenue suddenly dried up. Chart 2 shows the gross external financing requirement, GXFR, of selected countries calculated as a percentage of total reserves. GXFR covers both maturing debt denominated in foreign currencies (including dollars and euros) and the current account deficit over the coming year.

Both charts reflect a crisis in the making. The hard-currency import coverage for Turkey, Ukraine, Mexico, Argentina and South Africa, among others, is less than one year. This means that in the event of a developed-economy recession or another liquidity crisis where demand for EM exports dried up, the ability of those EMs to keep importing needed inputs would be used up quickly. Chart 2 has even more disturbing news. Turkey’s maturing debt and current account deficit in the year ahead is almost 160% of its available reserves. In other words, Turkey can’t pay its bills. Argentina’s ratio of debts and deficits to reserves is over 120%. The ratio for Venezuela is about 100%, and Venezuela is a major oil exporter. These metrics don’t merely forecast an EM debt crisis in the future. The debt crisis has already begun. Venezuela has defaulted on some of its external debt, and litigation with creditors and seizure of certain assets is underway. Argentina’s reserves have been severely depleted defending its currency, and it has turned to the IMF for emergency funding. Ukraine, South Africa and Chile are also highly vulnerable to a run on their reserves and a default on their external dollar-denominated debt. Russia is in a relatively strong position because it has relatively little external debt. China has huge external debts but also has huge reserves, over $3 trillion, to deal with those debts. The problem is not individual sovereign defaults; those are bound to occur. The problem is contagion. History shows that once a single nation defaults, creditors lose confidence in other emerging markets. Those creditors begin to cash out investments in EMs across the board and a panic begins. Once that happens, even the stronger countries such as China lose reserves rapidly and end up in default. In a worst case, a full-scale global liquidity crisis commences, this time worse than 2008. A full-blown EM debt crisis is coming soon. It is likely to start in Turkey, Argentina or Venezuela, but it won’t end there. The panic will quickly affect Ukraine, Chile, Poland, South Africa and the other weak links in the chain. The IMF will soon run out of lending resources and will have to pass the hat among the richer members. But the Europeans will have their own problems, and the U.S. under President Trump is likely to reply, “America First,” and decline to participate in bailing out the EMs with U.S. taxpayer funds. At that point, the IMF may have to resort to printing trillions of dollars in special drawing rights (SDRs) to reliquify a panicked world. SDRs are essentially world money. Elites are working behind the scenes to ultimately replace the dollar with SDRs as the leading reserve currency. A new crisis will bring that goal one step closer to reality. Regards, Jim Rickards

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)