Send this article to a friend:

May

06

2023

|

Send this article to a friend: May |

|

Consumer Credit Shocker: Credit Card Debt Explodes At 2nd Fastest Pace On Record Just As Rates Hit All-Time High

One month ago, not long after we warned that consumer credit was about to get much tighter in the aftermath of one of the most depressing Senior Loan Officer Opinion Surveys, which saw near record tightening in lending standards coupled with a historic plunge in credit demand, we observed that - as one would generally expect - growth in US credit card debt had ground to a crawl, as revolving credit rose by just $5 billion, down sharply from the $12.8 billion in January, down from the $13.7 billion LTM average, and the lowest single increase since April 2021.

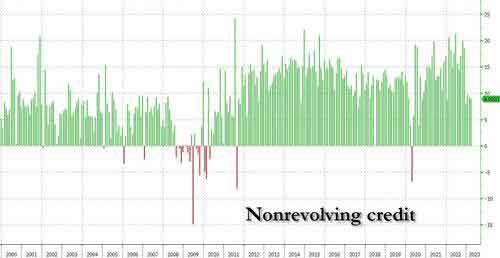

Looking at the data, we concluded that "while it is unclear if credit card usage rose at the slowest pace in two years due to weak demand or a sudden squeeze in supply - obviously we will have more information in one month when the next SLOOS hits - the implication is clear: one of the most powerful economic lifelines is grinding to a halt." Well, maybe not. Ever hear the saying never bet against (the stupidity of) the US consumer? Well, fast forward one month when moments ago the latest consumer credit data from the Fed was released and it was a doozy: instead of printing at a "credit-crunchy" subdued level, with the Street expecting only a modest increase from February's $15 billion to $17 billion in March, the Fed reported that the actual amount of new credit card debt was a whopping $26.514 billion, smashing expectations by almost $10 billion. But while the total number, while high, was generally in line with historical prints, it was the components that were remarkable. For once, we will start with the non-revolving credit, where the number was a big shock, or maybe not so big, because while historically the average number had been in the mid-teens, in March non-revolving credit, or student and auto loans, increased by just $8.9 billion, the 4th consecutive month in a row below $10 billion, the weakest such stretch since the covid crash.

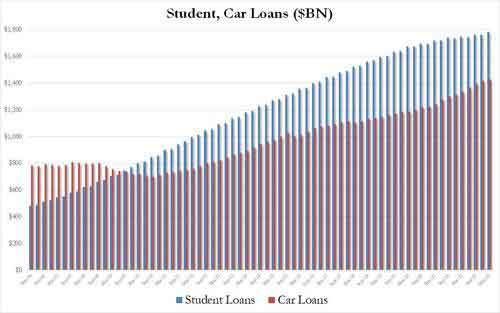

The reason for the slump in nonrevolving credit: as shown in the next chart below which shows the quarterly increase in non-revolving debt components, while student loans increased a mighty $20BN in Q1, auto loans rose by just $10.1 billion, the weakest increase since 2020. And yes, with auto loans at record high interest rates, this is not a shock.

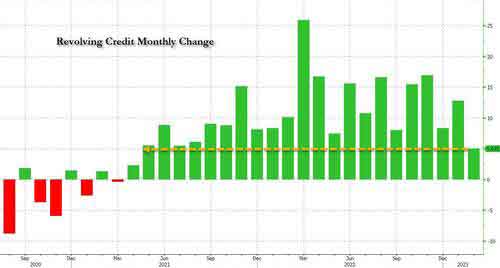

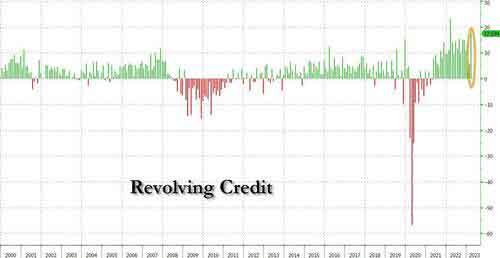

What was shocking, was the monthly change in the other big category, revolving credit. As shown in the next chart, after rising at the lowest pace since August 2021, the March change in credit card debt absolutely exploded, soaring by $17.6 billion, more than triple the February total, and the second biggest monthly increase on record! It's as if, either consumers - realizing this is their last hurrah to spend - went out and maxed out their cards at a pace (almost) never seen before, or perhaps the banks, desperate to load up peasants with some more debt, were handing out credit cards like hot cakes and the result is shown below. And while such a move could at least be explained, if not justified, when rates were at zero - after all the cost of money back then was negligible - this time it's a little more difficult to explain what is going on, especially when one sees the next chart from the Fed, showing that average credit card interest had just hit a record high 20.9%.

And so the scene for both the next crisis and credit crunch are set, because just like Americans couldn't afford their mortgages in 2008, hoping instead that some greater fool would take it off their hands at the right moment, so too now they are maxing out credit cards (just as rates hit all time high) knowing they will never repay the debt, but instead hope that the coming bank crisis will allow them to quietly sneak away without repaying their debt. Come to think of it, the bank crisis is already here...

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)