Send this article to a friend:

May

27

2023

|

Send this article to a friend: May |

|

Today’s Housing Market Looks Even Worse than 2008

Why housing? Well, here’s what The Economist has to sayabout it:

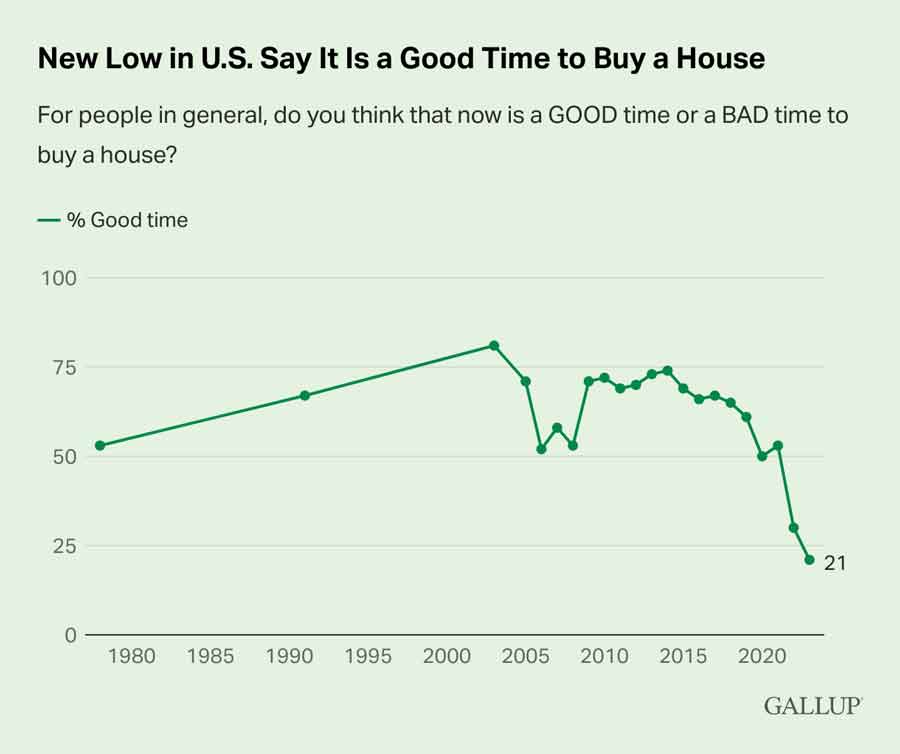

Owning a home is a crucial financial step for Americans – and, for most of us, our home represents the largest single investment we ever make. A massive amount of our nation’s wealth ($45 trillion dollars!) is tied up in homes. That’s why the housing market matters whether you rent or own. The housing market is a reliable leading economic indicator. As goes housing, so goes the economy – and right now, it’s not exactly going great… 79% of Americans say it’s not a good time to buy a house A recent Gallup poll asked whether it’s a good time to buy a home. (In 2003, that answer was a resounding yes.) Not anymore.

There’s a capsule history of housing market polling, since the last housing bubble burst in 2007:

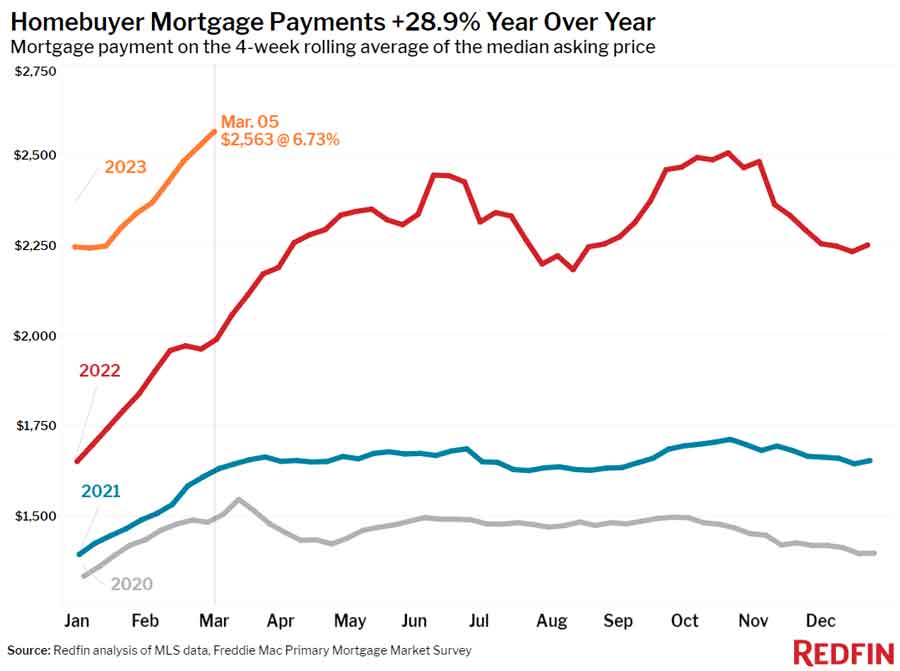

The housing market was already becoming unaffordable for many families back in 2021. It’s gotten much worse since then. Prices rose significantly, along with interest rates… In the last three years, the typical mortgage payment has risen 71% to a record high. (I had to triple-check the math.) Mortgage broker Redfin published a chart showing year-over-year changes since 2020:

Note this is just one bottom-line, real-world result of the Federal Reserve’s Here is the bottom line result of this mess, which results from the Fed raising rates (which they needed to do to ease red-hot inflation), as laid out nicely in a tweet by Charlie Bilello: Bilello followed up with an article that explained the rest of the bad news in the housing market:

Remember when I said housing was a bellwether, a leading economic indicator? Here are a few reasons why:

Like any other asset inflated by the Fed’s response to the pandemic panic, the housing market is in a tight spot. The reduction in sales and price stagnation (along with the fall in new home starts) point to an economic downturn in the very near future. And that will be bad news for everyone, not just those who saddled themselves with a 7.1% 30-year mortgage on a home with a declining value… Real estate isn’t the only real asset There are a few assets you can generally rely on to resist the corrosive effects of inflation. However, some inflation-resistant assets (in this case, homes) are much more economically sensitive than others. As I’ve just explained, housing is so extremely economically sensitive you can actually use it to forecast economic trouble ahead. Other “real” assets include Birch Gold’s specialty, physical precious metals. Gold isn’t just inflation-resistant, it’s the historic safe haven asset of choice during periods of economic crisis. If I’m right about the housing market, and this time around things really are worse than the last housing bubble that destroyed so many dreams, now is the time to consider your finances could survive a repeat of the Great Financial Crisis. Take a few minutes right now to learn more about the benefits of owning physical precious metals. About those might be the best thing you can do to protect your savings against both red-hot inflation and an economic downturn.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)