Send this article to a friend:

May

26

2023

|

Send this article to a friend: May |

|

Wages Going Up for Good: Catch-Up and Blowback

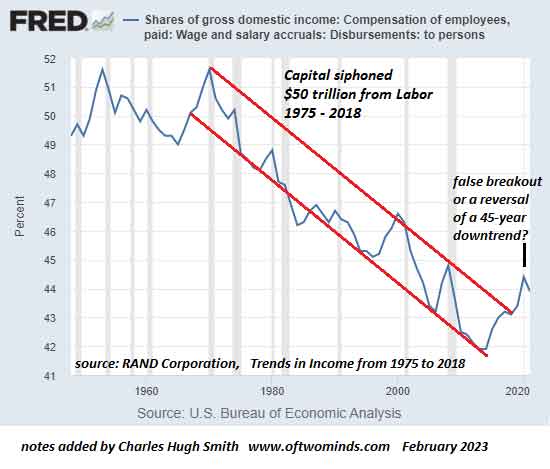

One of the most durable expectations in the financial sphere is that inflation will drop sharply in a recession and the Federal Reserve will lower interest rates back to near-zero. There is a good reason to doubt this: rising wages. Yes, we all hear about the millions of human workers who will shortly be replaced by AI–wonderful for corporate profits!–but few pundits bother looking at long cycles in interest rates and inflation, and even fewer pay any attention to the absurdly extreme asymmetry of labor and capital. As I’ve often noted here, labor’s share of the economy has fallen for 45 years. Only recently did it reverse slightly. It’s not yet clear if this was a brief false-breakout ot a change in trend, but there are good reasons to expect a secular, cyclical reversal that lasts years or even a decade. In other words, a decade in which labor / wages gain at the expense of capital. There are two basic narratives that are offered as explanations for how capital siphoned $50 trillion from labor over the last 45 years. One is that the macro-forces of globalization and financialization inherently favor capital and reduce labor’s leverage as production and jobs were offshored and US workers entered a race-to-the-bottom competition with developing nations’ low-cost workforces–a competition that kept US wages stagnant even as US corporate profits and financial assets soared. The other narrative starts with the observation that the erosion of wages and the glorification of corporate power was the direct result of specific policies being adopted. The dominance of corporate interests and the stripmining of labor were anything but inevitable: it was engineered by policies that enriched the top 0.01% (the Financial Aristocracy), and the top 10% who own 90% of America’s productive capital. This wholesale transfer of wealth and income from workers to Capital was documented by a RAND Corporation report, Trends in Income From 1975 to 2018. Time magazine summarized the findings: The Top 1% of Americans Have Taken $50 Trillion From the Bottom 90% — And That’s Made the U.S. Less Secure. (We’re told the stagnating wages of the past 45 years) were the unfortunate but necessary price of keeping American businesses competitive in an increasingly cutthroat global market. But in fact, the $50 trillion transfer of wealth the RAND report documents has occurred entirely within the American economy, not between it and its trading partners. No, this upward redistribution of income, wealth, and power wasn’t inevitable; it was a political choice–a direct result of the trickle-down policies we chose to implement since 1981. The net result of this four-decade siphoning of wealth/income from workers was documented by a Foreign Affairs article: Monopoly Versus Democracy:

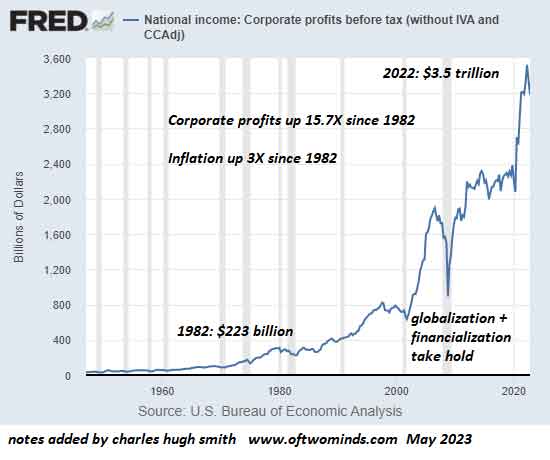

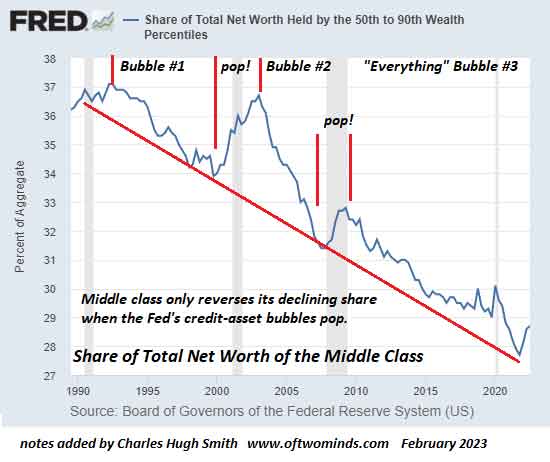

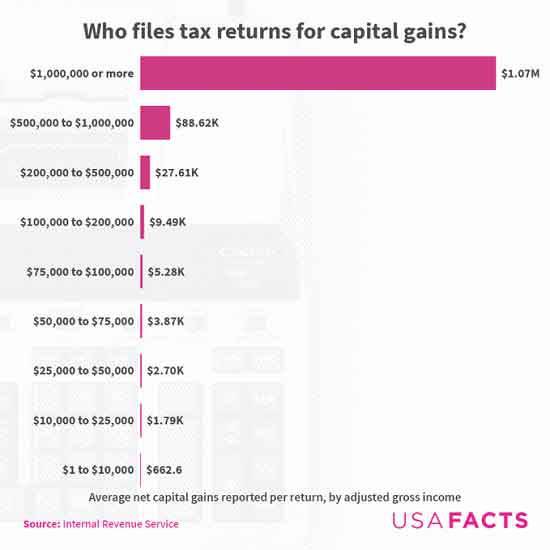

In other words, the bottom 90% have very little stake in the status quo: they receive essentially zero income from America’s stupendous $140 trillion hoard of private wealth and have essentially zero political influence, as documented in Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens. We can see these realities in the data /charts. As the charts below (courtesy of the Federal Reserve FRED database) show, wages’ share topped out in the early 1970s and trended down for 45 years. Corporate profits skyrocketed 15.7-fold since 1982 while inflation rose “only” 3-fold. This decline in wages is mirrored by a corresponding decline in the wealth of the bottom 90%. It’s not just wages that stagnated–so did the share of the nation’s wealth held by the middle class / bottom 90%. The middle class’s share of private-sector wealth (total net worth) has plummeted from 37% in the early 1990s to 28%, a decline of $12 trillion compared to what would have been the case had the middle class continued to hold 37% of net worth. $50 trillion here, $12 trillion there, pretty soon you’re talking real money that’s been transferred from the wage-earning peasantry to America’s Financial Aristocracy. We see this vast asymmetry in who collects the primary engine of wealth for the top few: capital gains. Those who already own most of the wealth have pocketed the stupendous gains of the past three decades. Middle class households pocket $4,000 or $5,000 in annual capital gains while those who own most of the wealth pocket on average a cool $1 million–200 times the middle class gain in unearned income. So why will wages rise, regardless of deflation and AI? Catch-up and blowback. Even if we accept the “gee, we were helpless to stop wage stagnation” story (which is false, as detailed above), financialization and globalization are reversing and so labor can finally play catch-up to capital’s asymmetric gains. If catch-up is suppressed by corporate political power, then blowback kicks into gear. The workforce has had enough of corporate-state pillaging, and while corporations are gleefully planning the elimination of their human workforce via AI and automation, that fantasy isn't going to play out as expected, for automation has limits which I discuss in my book Will You Be Richer or Poorer?. Nobody thinks that there could be political limits on corporate power, but precious few asymmetries that reward the few at the expense of the many last forever. Blowback has a remarkable ability to careen from nobody notices or cares to full-blown revolt in relatively short order. The greater the asymmetry, plunder and hubris of the Aristocracy, the greater the eventual swing of the pendulum to the opposite extreme. Blowback has its own dynamics, as we'll learn in the decade ahead. Wages--and the inflation they generate--are going up for good whether anyone thinks this is possible or not. And inflation pulls interest rates higher, whether anyone thinks this is possible or not. It's not just the Federal Reserve that matters; asymmetries, exploitation and plunder matter, too.

At readers' request, I've prepared a biography. I am not confident this is the right length or has the desired information; the whole project veers uncomfortably close to PR. On the other hand, who wants to read a boring bio? I am reminded of the "Peanuts" comic character Lucy, who once issued this terse biographical summary: "A man was born, he lived, he died." All undoubtedly true, but somewhat lacking in narrative.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)