Send this article to a friend:

May

05

2022

|

Send this article to a friend: May |

|

The Fed Is Creating an Opportunity of a Lifetime

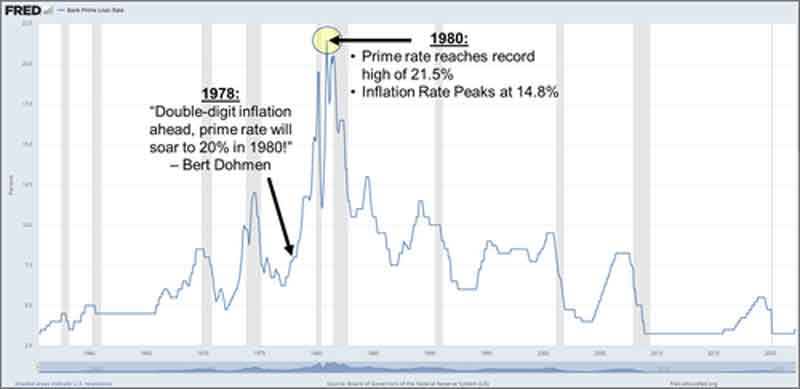

After the Fed chairman announced the Fed would not “tighten” money but would combat inflation through higher interest rates, we wrote that this was a “green light for inflation to rise.” We predicted that rising interest rates would therefore cause a plunge in long term US Treasury bond prices by “40%-50%.” Wall Street analysts called that forecast “absurd.” However, about two years later, T-bond prices had plunged 44%. Bond yields were over 15%, hitting a 100-year high. Investors who subscribed to our Wellington Letter and sold their bonds in 1978 saved themselves from devastating losses.

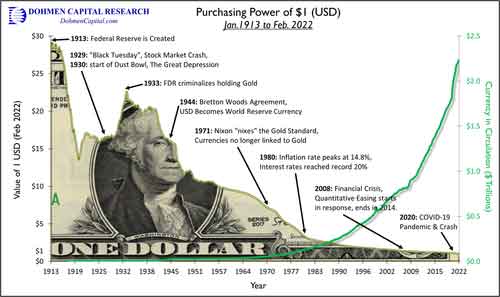

Other experienced investors, who followed our suggestion of selling T-bonds short during that time, accumulated great profits amid the bond calamity. Currently, in 2022, we see the “next” opportunity of a lifetime as the financial conditions are very similar to what we saw in 1978. With interest rates now soaring, T-bond prices have already plunged 35% from their year 2020 high. Those who sold short have made great profits while those with large bond portfolios experienced big losses. But the best opportunities for short-sellers is still ahead. Our work suggests that this is only the beginning. We see historic record losses in bond portfolios on the horizon. Whereas the losses in Treasury bond prices 40 years ago was around 44%, this time they could be 50%-70% greater. We expect that statement to be greeted the same way by Wall Street as it was in 1978. The reason for this forecast is the fact that inflation is rising and therefore interest rates are on their way higher. The central banks always try to fight inflation by hiking interest rates. It seems that somewhere analysts and economists were taught that more expensive money reduces the cost of doing business and therefore gives the incentives to businesses to cut prices, thus lowering inflation. This is totally false. How do they think this is possible? On the internet, this erroneous theory is explained: “As interest rates are increased, consumers tend to save because returns from savings are higher. With less disposable income being spent, the economy slows and inflation decreases.” Wow! Do you see the false assumption? People will increase savings when interest rates rise? But it says nothing about consumer spending increasing because of inflation; consumers want to beat future price increases. No wonder economics is called “the dismal science.” Rising interest rates only reduce growth when they result in tight money, i.e. the inability to get new loans. Borrowed money at today’s very low interest rates is basically free as you pay back the loans with much cheaper money that has far less purchasing power. This year we estimated that inflation was higher than 11% in January. But Dr. John Williams of shadowstats.com calculates that the true inflation at the end of February hit 16.05%, the steepest inflation rate since June 1947 (in 75 years). If you borrow money at 6%, you are still way ahead of true inflation, by 10 percentage points. Therefore, it pays to borrow as long as banks make the loans. This is how millionaires become billionaires. As long as banks want to lend at those low rates, this in turn boosts borrowing and thus inflation growth. The Fed raised rates the expected 0.25% in March 2022. The FOMC said that at their next meeting (Today, May 4, 2022) they would likely hike rates another 0.50% and also start reducing the Fed’s balance sheet, i.e. taking money out of our financial system. Our prediction is that this will not happen. Instead, they will just reduce the “rate of growth” of the balance sheet and declare victory. But that remedy is snake oil. On March 22nd, 2022, Fed head Powell suggested that there may be several meetings in which they would hike rates by 0.50% points. They are finally realizing that they are far behind the curve, just as we wrote last year. Therefore, the Fed must catch up, although they never do. Once again it is pretense. If they were serious in truly fighting inflation, why didn’t start last year, or this past January? Fed chair Powell expects inflation to come down later this year and in 2023. He didn’t explain how this miracle would be achieved. Of course, he is talking about “the rate of inflation,” not actual inflation declining. We ask, when have you ever seen inflation decline for a longer period without the Fed actually tightening the availability of credit? Not since the Federal Reserve was established in 1913. Below is a chart that shows how the value of 1 US dollar has been completely eviscerated over the past 109 years while the amount of currency in circulation has skyrocketed (green line).

Does historical data over a century long give you any confidence that the dollar’s value will ever increase, i.e. that price increases are “transitory”? The more money the Fed prints (green line on chart), the lower the value of the dollar will decline… Continue reading the rest of our special report, “Surviving Soaring Inflation: The Opportunity of a Lifetime”, FREE for a limited time. Simply go to DohmenCapital.com or click this link: Get My Free Report

|

Send this article to a friend:

|

|

|

We at Dohmen Capital Research declared our first “Opportunity of a Lifetime” in the history of our economic and investment research firm in 1978. At that time, our firm was a little over one year old.

We at Dohmen Capital Research declared our first “Opportunity of a Lifetime” in the history of our economic and investment research firm in 1978. At that time, our firm was a little over one year old.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)