Send this article to a friend:

May

13

2022

|

Send this article to a friend: May |

|

The most difficult thing in economics…is to explain rising prices

Those who have protected their wealth by investing in financial assets no longer have the following breeze of falling interest rates. Financial bubbles are now bursting. Understanding the causes and therefore being able to assess the likely losses involved is becoming urgent for anyone committed to financial markets. This article explains inflation in its proper context, which is loss of purchasing power for state-issued currencies, so that current conditions are better understood. It dissects the delusions behind monetary policies over both the causes of rising consumer prices and interest rate management. It concludes that we are beginning to experience the worst of two worlds simultaneously: while the financial bubble collapses, in anticipation of and the response to an accelerated debasement of fiat currencies, prices of everything from commodities to finished goods will soar as a crack-up boom materialises. The role of money For the first time in decades inflation fills the headlines. The popular press is full of tales of hardship for the disadvantaged in society. Higher energy costs, higher food costs, rising taxes — they all serve to inflict hardship. In opinion polls politicians are facing the wrath of those who suffer. Financial commentators have not much of a grasp of the situation, reacting religiously to government statistics and many concluding that the condition is stagflation — a condition whereby the economy stagnates while prices rise. The combination, according to macroeconomists, cannot be adequately explained because it cuts across the relationship between supply and demand: a stagnating economy or a recession represents inadequate demand and inadequate demand leads to falling prices, they say. So how can prices rise in a stagnating economy? This is what students of economics are taught today and the thread of this economic illiteracy runs through everything from monetary policy to discussions over the dinner table. Until Keynes weaponised it, perhaps economists could agree on one thing, and that is money’s function is as a medium of exchange, whereby we earn it in return for our labour and we spend it to acquire the things we need and desire which we don’t produce for ourselves. This division of labour still applies when we save it. Money is then a credit for our production yet to be spent. The intention is always to spend it or give it to someone else to spend it in the future, such as by lending it, through inheritance, or even paying the government to pass on as welfare. The concept of money’s purchasing power is simple enough, being what can be obtained in exchange for it. But what amounts to the same thing, the objective exchange value, perhaps needs further elaboration. Simplistically, when we exchange money for goods the exchange is recorded in the price of the goods measured in money, and not the price of money measured in goods. We say that a loaf of bread has a price, not that of the money used to buy it. And the value of a loaf of bread is purely subjective, meaning that the individual considering its purchase places his value on it when considering whether to buy it. While his decision is whether he values the loaf more or less than the money, it is impossible for him to decide unless he assumes that the exchange value of the money is a constant factor enabling him to exchange it for other goods, or even an alternative type of loaf of bread. But we must take that one step further and explain that despite Keynesian economic use of money as a medium for macroeconomic management, money has no other use than as a medium of exchange. The value we place on a medium of exchange is the anticipated use-value of the things that can be obtained with it. Obviously, this is a subjective factor in the minds of those that use the money, and this use-value of it therefore depends on psychological factors. Equally and separately from its use-value, its exchange-value is also subjective. In other words, there must be trust that the money in one’s possession will be accepted by others in exchange for goods. By combining both use and exchange values, the possessor of money can then view it objectively when it comes to exchanging it for goods. It allows for the comparison of the values of goods to be made one against the other, with the medium of exchange being regarded as the common, or objective factor in the comparison. While automatically assuming money’s objective value in transactions, it permits individuals to understand that changes in the purchasing power of money can occur, so long as they continue to accept both its use- and exchange-values. As Ludwig von Mises put it in his The Theory of Money and Credit:

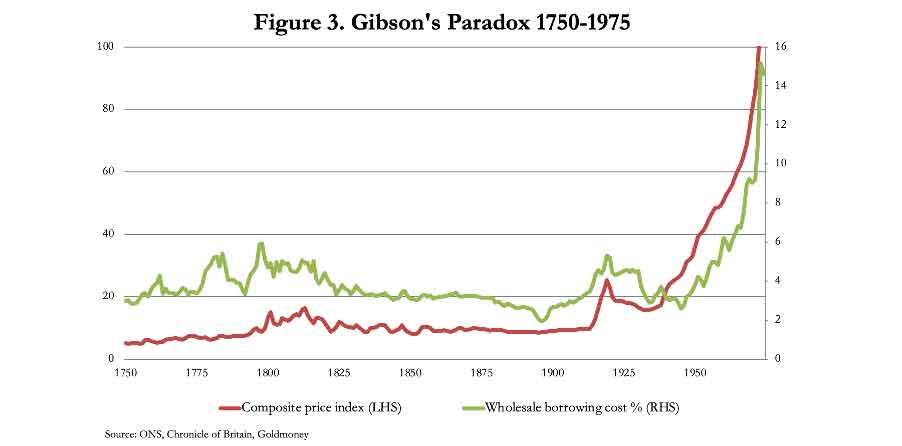

As Mises stated, it is only a starting point. But it is from this point that the disinformation starts. When the general level of prices rises, it is commonly referred to as inflation. The word in this context is incorrect. Inflation is something that happens to balloons. In this context it is an increase in the combined quantity of money, currency, and credit, which will tend to increase prices all else being equal. An increase in the general level of prices reflects the falling purchasing power of money. The purchasing power of money can fall for two reasons, one of which is the dilution of money through an increase in its quantity or the quantity of its substitutes in the forms of currency and credit. But the most important reason for its fall is changes in the anticipated use-value of the things that can be obtained with it. In other words, if a population believes that the purchasing power of money will fall, by altering the preference relationship between monetary liquidity and ownership of goods in favour of goods, the purchasing power of money will indeed fall. So even the idea that rising prices always reflects monetary inflation is incorrect. Deflation is another linguistic sin. Deflation is something that happens when the air is let out of a balloon, or expectations are not fulfilled. Common parlance amongst economists is that it is falling prices. No —falling prices are the consequence of an increase in money’s purchasing power, which can happen either due to a contraction in the total of money, currency, and credit, or when a population decides that on the margin holding a greater amount of money, currency and credit is preferable to adding to one’s stock of goods. We must now look in greater depth at the relationship between money and prices. The economics of sound money differ from fiat money The economists of the twentieth century based their concepts of money and credit on knowledge gained under the gold standards of Britain, Europe, and America before the First World War, and in important respects have not revised their notions in adapting theory for the purely fiat currency world that has been our lot since the end of Bretton Woods.Monetarist theory evolved from David Ricardo’s observations in the early nineteenth century, and the debate over money, currency and credit subsequently raged between the currency and banking schools until the Bank Charter Act of 1844. But the consequence of the gold standard was that it imparted an underlying stability of human action over money which allowed for monetarist theory to develop. It allowed economic actors to combine the subjective use- and exchange-values into an objective value for currency as described above. Remove the sheet anchor of true money, and a currency becomes exposed to a breakdown in its objectivity. Not only have economists in their theoretical deliberations paid insufficient attention to the difference between money with its credible substitutes and an unbacked fiat currency, but most of academia does not understand credit either, as exemplified by incorrect descriptions of the workings of the banking system.[ii] While the cycle of creation and contraction of bank credit is common to both sound and unsound monetary systems, a gold coin backed system differs materially in its effect on the general level of prices from that based on a purely fiat currency. Secure in the knowledge that it can exchange currency for coin on demand, the public does not generally alter the relationship between its currency preferences and ownership of goods, other than when tempted to do so by credit-driven variations driving interest rate changes. Therefore, through all the ups and downs of bank credit, wholesale prices tended to fall gradually between the official introduction of the British gold sovereign in 1820 and 1897. The general level of wholesale prices fell 17%, driven entirely by industrial and technological progress despite the increase in above-ground gold stocks (see Figure 3 below, of the UK composite price index). Following 1897, prices began to rise, reflecting the unprecedented increase in gold mine supply, when South African gold output began to affect the purchasing power of money. From 1886 annual world mine output rose from an estimated 157 tonnes to 702 tonnes in 1913, slightly more than doubling recorded above-ground stocks.[iii] Under this influence the general price level increased by nearly 13%. But the fact that this price increase was minor compared with the increase in above-ground gold stocks is justified partly by the expansion of non-monetary gold stocks not entering the reserves of the banking system, partly by a tendency for the British population to increase their savings attracted by wholesale borrowing costs which rose from 2% in 1897 to 3.6% in 1913, and partly due to improvements in production methods. At the outbreak of the First World War, over 80% of world shipping afloat was built in Britain, a talisman of Britain’s economic success in the global context following the introduction of its gold coin standard in 1820. But that was to be the peak, and following the Great War, we must follow prices set under America’s monetary standards, a gold exchange regime fixed at $20.67 to the ounce. In the post-war slump, US wholesale prices fell by 44%, but then stabilised until 1930. Reflecting a collapse of bank credit, the depression drove prices down to pre-WW1 levels.

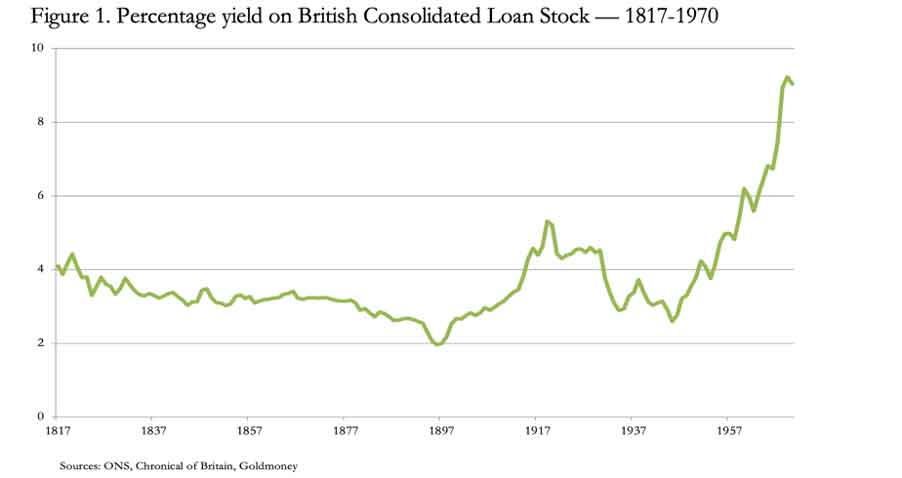

Under the 1944 Bretton Woods agreement, foreign central banks were free to exchange dollars for gold, reflected in stability in prices for commodities, energy, and raw materials, which were priced in dollars. Crude oil was priced at $2.57 per barrel in 1950, and by 1968 it had only increased to $3.07. The stability of energy and commodity prices contributed to wholesale prices increasing only gradually over the period, despite the increase in the quantity of money and credit, which from 1947 had grown a further 287%. In effect, there were two standards, a domestic fiat dollar and an intergovernmental bullion-dollar exchange standard. The empirical evidence is that a pure gold coin standard is associated with gently falling prices over time. Compromises which restrict the ability of economic actors to exchange gold freely for currency remove the strict discipline on the issuer, leading inevitably to a fall in purchasing power. By giving foreigners through their central banks access to a bullion exchange standard, the Bretton Woods agreement preserved a general price stability for commodity and energy inputs. But that was not to last due to the expansion of dollar currency and credit, not just on the domestic front but also to finance wars, notably in Korea and then Vietnam. Further currency expansion was deployed as America established military presences throughout the free world and inevitably this debasing expansion would impose systemic strains between the domestic fiat and foreign bullion standards. This led to the failure of the London gold pool in the late 1960s, and then the ending of the Bretton Woods agreement in August 1971. The end of Bretton Woods was followed by massive price increases by energy and commodity exporting nations, who had had the bullion exchange standard removed from them. Led by Saudi Arabia, OPEC members sought compensation sufficient to persuade them to retain dollar deposits, and the price of oil jumped to $32.50 per barrel by December 1979, more than ten times the 1968 level of $3.07. To fully appreciate the consequences of the demonetisation of currencies into their fiat status, we must now refer to the change in purchasing power for the fiat dollar against money itself — that is gold. We know that under an unlimited gold coin exchange standard currency operates as a gold substitute and the relationship between the level of public holdings of monetary reserves relative to ownership of goods is inherently stable, reflecting confidence in the currency. But under these sound money circumstances, the expansion of currency and credit led to a corresponding fall in their purchasing power. In other words, the quantity theory of money was an adequate description of the price relationship. This allows us to use the gold price as a proxy between the sound money case and that of fiat currencies. From a notional $35 the gold price this week stands at $1850. That is a fall in the dollar currency’s purchasing power against lawful money of 98.1%. Note that we are not claiming that any one measure of rising prices has risen by the reciprocal of that amount. But clearly, loss of purchasing power for a purely fiat currency is in a different league from the fluctuations under a gold exchange standard. And if we look at the change in the quantity of M3 money supply, we arrive at a similar conclusion with respect to the dollar’s debasement. In 1971, US M3 was recorded at $638.3 billion, and the figure for February this year comes in at $21,812. That is a debasement of 97.1%. The extent to which this is reflected in the general level of consumer prices is impossible to quantify. There is considerable subjectivity in the construction of a price index, and each person’s experience differs, so in this context government consumer price indices are unfit for purpose. We can only say one thing: the close relationship between M3 and the dollar price of gold over time suggests that the public’s liquidity preferences have not changed materially since the end of Bretton Woods. But instead of fuelling higher product prices in their entirety, the application of added monetary quantities has undoubtedly inflated financial asset values not in the consumer price index. We must therefore be aware of two consequences. Not only has the expansion of the combined quantities of currency and bank credit led to a falling purchasing power for fiat currencies, but it has also resulted in a financial bubble and increasing speculation that puts earlier excesses, such as John Law’s Mississippi venture and the South Sea Bubble in the shade. It is a global phenomenon that can only be associated with the financialisation of currency and credit. And a feature of it is the suppression of interest rates to the zero bound, and in the case of other systemically important currencies, into unnatural negative territory. The fallacy behind interest rates Central banks would have us believe that interest rates are the price of money, and that by managing the price, they can manage demand for it. While undoubtedly a businessman making an investment calculation in connection with his production sees interest as a business cost, an investor sees it very differently. He views interest as compensation for loss of possession of his money, compensation for lending risk, and compensation for any expected changes in the purchasing power of his money until its return.When money is sound, in other words no deterioration in its purchasing power is expected, an interest rate before taking account of lending risk is a function of savings supply set in the context of time preference, being the compensation savers expect for the temporary loss of money’s possession. Despite all the decades of denial by the authorities that it is the case, the legal definition of money is metallic, usually taken to mean gold because it was the gold standard that prevailed over silver. Gold coin in possession pays no interest. When it is exchanged for credit, being a promise to repay it to the lender, it is only then that interest is involved. Figure 1 shows how this has varied for loans to the British government, which for sterling credit can be regarded as the rate free of counterparty risk compared with, say, a loan to a business. The timespan is from the minting of the first sovereigns which became the gold coin standard in 1820, to the year before the abandonment of the Bretton Woods agreement.

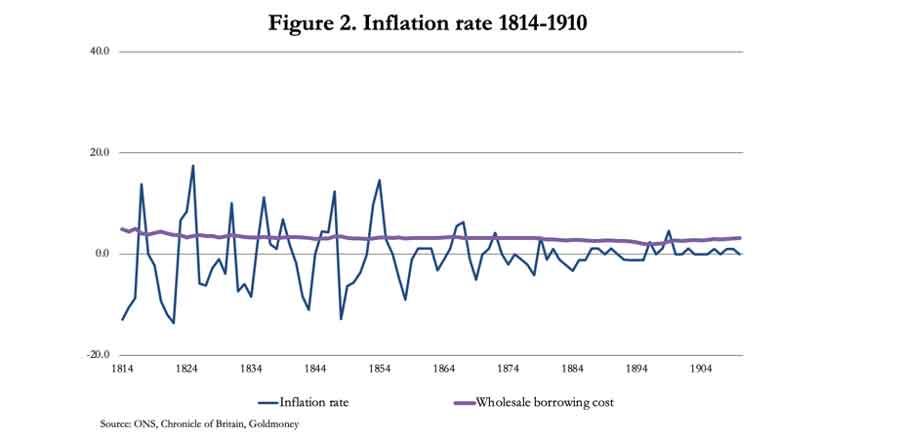

In no particular order the factors to consider are the availability of specie, the price volatility of the debt, the expansion and contraction of outstanding credit, war risk, political risk, and the suspension of the metallic standard. 1817 was two years after Napoleon’s defeat at Waterloo, and as Britain prospered through the industrial revolution that followed, the yield fell to a low point in 1897. Variations in the yield were particularly noticeable before the 1844 Bank Charter Act, reflecting a cycle of bank credit expansion and contraction, after which interest rate volatility was likely reflected more in bank deposit rates more than in the “risk-free” Consols yield. At the end of the nineteenth century, South African gold discoveries began to affect the purchasing power of money. From 1886, annual world mine output rose from an estimated 157 tonnes to 702 tonnes in 1913, slightly more than doubling estimated above-ground stocks. Convertibility was suspended in 1914 at the outbreak of the First World War and followed by a bullion standard in 1925 which operated until 1932. It was a time of interest rate volatility, affected by the collapse of European currencies and their economies, interventions in both bullion markets and interest rates, the American boom in the 1920s and the subsequent depression, labour unrest and the Second World War. In 1945 the yield on Consols reached a low of 2.6% before rising to over 9% when the London gold pool failed in the late sixties. This post-war rise in yields reflected the decline of Britain relative to America under punitive taxation, aggressive socialism, and fiat sterling increasingly skirting with crisis. Even with a gold coin standard, the evidence is that interest rates can vary considerably. But Figure 2 shows how they do not correlate with the rate of inflation.

Named Gibson’s paradox by Keynes who failed to explain it, the explanation for the correlation is that producers must estimate the final price of their production in their calculations. Higher prices allow them to pay a higher rate of interest in the quest for profits, so their agents in the banking system can bid up deposit rates to entice savers to lend rather than spend. Keynes’s mistake was to assume interest rates were set by savers withholding savings supply greedy for “unearned” income instead of businesses as a result of their profit calculations. Following the mid-seventies, in the UK the correlation ended as the price index continued to soar. Nominal interest rates measured by Consols remained high, initially hitting a peak of over 15% during late-1973, when price inflation had soared to 26% and the IMF bailed Britain out of its crisis. The US’s price inflation crisis did not materialise until the end of the decade when the Fed finally raised the Fed funds rate to over 19%. Thereafter, central banks increasingly gained control over markets as the financialisation of major Western economies gathered pace. That period appears to be coming to an end with central banks being challenged by markets in their attempt to keep interest rates low, while the decline in currencies’ purchasing power has accelerated. The markets appear to be reasserting themselves. Now we face rising prices The invention of macroeconomics, borne out of Keynes’s General Theory and his denial of Say’s law, was to establish and justify statist management of economies to the detriment of free markets. The self-interest of governments and their agencies in the form of central banks has led to our current situation. The establishment has been spending beyond its revenue income and manipulating interest rates to conceal the consequences. The evidence of economic malfeasance has been suppressed through statistical management. Macroeconomics has now run its course and with its adherents turning a blind eye to the quantity effect of money we appear to be on the edge of a currency sinkhole.Since Alan Greenspan’s tenure at the Fed, if not before, the importance of sustaining asset values as being essential for maintaining confidence in the economy has been the central plank to official policy. Production of goods has been chased away into Asia, where labour is cheaper, and time taken to production considerably shorter. Hollowed-out western economies have increasingly relied on financial activities to fill the gap left by production, and the trend of falling interest rates since the early eighties has bolstered financial asset values in a long-term bull market. It has been a win-win for the big banks, which increasingly rely on financial assets as loan collateral, as opposed to assets which are productive. Even if it cannot be properly verified, it is certainly credible to argue that the inflation of the financial bubble has replaced inflation of goods prices to some degree. The extent to which this might be true has undoubtedly informed monetary policy to the point where everyone in the mainstream from policy makers downwards no longer believe that changes in the quantity of currency and credit matter with respect to consumer prices. But they do. The expansion of budget deficits to unprecedented levels over covid and for other reasons has debauched the dollar and allied currencies, resulting in accelerating falls in their purchasing power. And finally, in a political suicide pact the Americans are leading their allies into a sanctions war against the world’s largest exporter of commodities — Russia. It should remind us of the power wielded over energy prices by OPEC when denied the facility offered to turn dollars into gold by the ending of Bretton Woods. If those called the unfriendlies by President Putin were to stop the expansion of currency and credit stone dead, then their currencies would stabilise. But that is not going to happen because of Keynesian misconceptions and political reality. Consequently, prices will continue to rise, and there is now a growing risk of the second factor in the money-to-prices relationship coming into play. A fundamental confidence in the power and authority of governments setting monetary policy is required for fiat currencies to have any validity with its users. If that goes, preferences in favour of a currency become eroded to the point where no sane consumer wants to hold it. We are now at an important point in that journey to extinction. Interest rates are rising inexorably, and market participants are just beginning to understand that official forecasts, which are after a year or two of slightly higher interest rates price increases will return to a targeted CPI rise of 2%, are propaganda. The financial bubble, which has been decades in its inflating, is now imploding. In it past time to consider the policy makers’ response. Having discarded the quantity theory of money, we can see that the imploding financial bubble requires central banks to increase the rate of currency expansion and to underwrite the expansion of bank credit, by rescuing the entire commercial banking network if called upon. We are about to experience the worst of two worlds simultaneously: while the financial bubble collapses, in anticipation of and the response to an accelerated debasement of fiat currencies, prices of everything from commodities to finished goods will soar as a crack-up boom materialises.

[i] Chapter1: The concept of the value of money. [ii] For a description of how the banking system operates and the creation of bank credit, see https://www.goldmoney.com/research/goldmoney-insights/building-a-better-banking-system

[iii] Estimates from a study by James Turk: https://www.goldmoney.com/research/goldmoney-insights/the-aboveground-gold-stock

|

Send this article to a friend:

|

|

|

It is apparent from media commentary that there is considerable misunderstanding over the causes behind rising prices and the consequences for interest rates. There are now signs that the official narrative over these issues is misleading at best.

It is apparent from media commentary that there is considerable misunderstanding over the causes behind rising prices and the consequences for interest rates. There are now signs that the official narrative over these issues is misleading at best.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)