Send this article to a friend:

May

31

2019

|

Send this article to a friend: May |

|

|

Gold in the Age of Eroding Trust

In front of you, dear reader, lies the 13th edition of our In Gold We Trust report.1 It’s a special edition. Never before have we invested so much time, energy, money and passion into this report. Never before has the team for the report been so large. And never before have we analyzed such a broad spectrum of topics. For the first time, we are publishing the In Gold We Trust report in China, for a market that is becoming increasingly important for us and for the gold industry. But it is also a special vintage because we have chosen a theme that is of the utmost importance for both interpersonal cooperation and economic prosperity. The term is so crucial that it is an integral part of the name of our annual publication: trust. Let’s start with the definition:

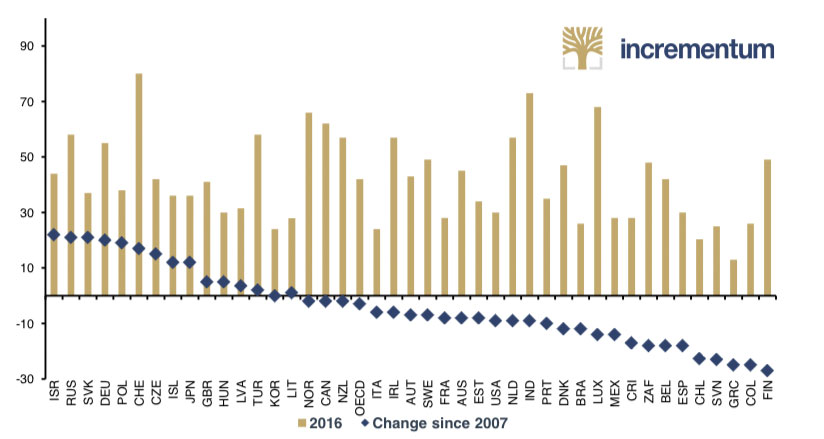

Trust is often underestimated. Many of us take trust for granted, but almost all human interactions are based on trust. When visiting a restaurant, we trust that the cook will not use any spoiled ingredients, ensures cleanliness in the whole preparation process, that eventually results in a tasty meal. We trust that the pilot, crew, and technicians will do a good job when we get on a plane and go on holiday. We trust that our friends are there for us when we really need them, and we trust our partner to always remain faithful to us. Without a minimum of trust, a human relationship – even in a rudimentary form – is simply unthinkable. Trust is the basic value of human interaction and the cement of our social order. In a constitutional state, citizens trust state institutions to respect and protect their private property. But equally private and public institutions such as the media and science build on a certain basic trust. Introduction Trust looks to the future, forms itself in the present, and feeds itself from the past. Gaining trust, erosion of trust, and social polarization Trust within a society must grow; it is not simply there. Societies are characterized by different levels of trust. A distinction is made between so-called “high-trust societies” and “low-trust societies”.4 In a high-trust society, individuals are more open to new personal friendships and new business relationships, while in low-trust societies there are major barriers to building trust with people outside the family.5 Similar to the capital stock of a society, whose abundance and stability leads to a more productive economy, trust capital can also be consumed and gambled away. As with physical capital, building trust capital is much more difficult than consuming it; and as with physical capital, consumers of trust capital can consume too much of it in the short term –taking without giving. The Western world is to a large extent a high-trust society. Cooperation is no longer based on belonging to a small, tight-knit community such as a clan, but rather to a comparatively anonymous society in which people trust each other without necessarily knowing each other. Without this advance of trust, without this open approach to each other, there can be no mutually beneficial cooperation. However, there is growing evidence that this trust is increasingly eroding. Trust in institutions such as politics, science, and the media is of crucial importance to society. Confucius was of the opinion that three things were necessary for governance: weapons, food, and trust. If a ruler is unable to obtain all three things, he should first give up weapons, then food, and finally trust.6 Politics, science, and the media have suffered losses of confidence in recent years, some of which have been significant. Since 1972 the General Social Survey has measured the confidence of Americans in various institutions. Since 2000 confidence in virtually all institutions has eroded, with the exception of the military. Only one in five persons still has confidence in banks, churches, or big business and only one in ten (!) in the government. According to the next graph, trust in politics is eroding all over the globe.

Trust in governments, in %, 2016 and change since 2007

Among millennials, confidence in democracy is waning, says Neil Howe: Howe refers to studies by Harvard professor Yascha Mounk showing that not only American but also Western European youth have lost faith in democracy. The later the interviewees were born, the lower their confidence in democratic institutions and the greater their desire for strong leaders.7 A by-product of the loss of trust is the spreading polarization of society.8 This development is so pronounced that the degree of polarization sometimes culminates in personal contempt and even violent acts. Surveys show that Americans, for example, are politically more polarized than they have been since the Civil War. Since the election of Donald Trump as US president, one in six US citizens no longer talks to a close relative or once close friend if they belong to the other political camp.9 In Europe, too, different symptoms of loss of trust can be seen, accompanied by increasing social polarization. The emergence of right- wing and left-wing populist parties and movements is not the only sign of a loss of confidence in the established party landscape. Phenomena such as the Yellow Vests protests in France and the Reich citizens’ movement in Germany are clear indications that some European citizens are withdrawing confidence from the government. The Friday-for-Future movement, which openly accuses politicians of failing to live up to their responsibilities, has recently joined the ranks of the disaffected. 2019: “Since 2014 the asymmetry in the attribution of motives (my convictions are based on love, yours on hatred) has been as great as between Palestinians and Israelis. Nine out of ten Americans suffer from the division.” (Our translation). In this respect, the book Love Your Enemies, by Arthur C. Brooks is recommended.

Trust in the mass media has undoubtedly also declined. Donald Trump, who has regularly questioned the integrity of the press in the USA since taking office, has contributed to this. Numerous other media events, such as the scandal surrounding the German journalist Claas Relotius, who made up some of his reporting,10 have also further damaged confidence in the media. The designation of the mainstream media as a “lying press”, spouting “fake news”, is an expression of this loss of trust, which further deepens social polarization. Trust in science is also declining. Skepticism towards scientific findings is widespread. Much attention is paid to topics such as climate change, which are highly emotional, but the various camps are deeply distrustful of the scientific facts presented by the other side. The loss of confidence also manifests itself in doubts about highly conventional scientific findings. Thus, dubious worldviews such as the “Flat Earth Theory” are enjoying increasing popularity.11 The phenomena of the increasing erosion of trust are fascinating and worrying, but they should not be the focus of this publication. Nevertheless, we wanted to start by deliberately pointing out such developments in order to put the leitmotif of this year’s report into context. Because if the level of public trust is declining, that may have serious implications for one of the most important institutions of our society: money.

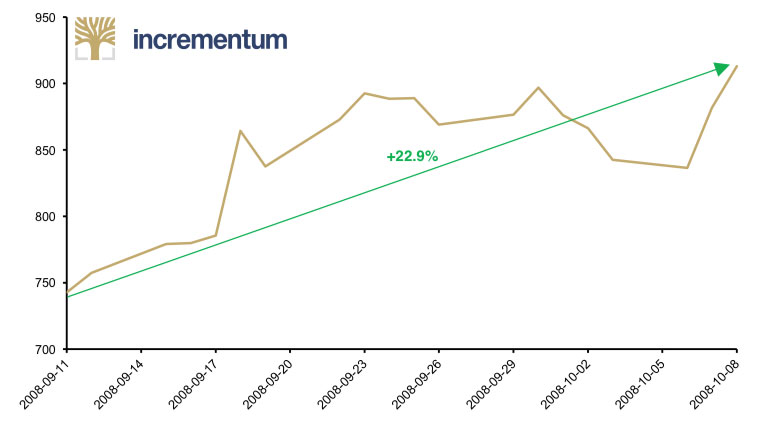

Gold price during Lehman crash, in USD, 11/09/2008-08/10/2008

Trust in the monetary system High basic trust within a society results in economic prosperity, because only trust enables an efficient division of labor. One prerequisite for this is a medium of exchange that enjoys general trust, because otherwise the exchange of goods and services becomes constrained, highly inefficient and costly. Money is ultimately spiritual energy which man acquires, reasonably consumes, gives away, or gambles away. Money is thus nothing more than an abstract energy store. But in order for fairness of exchange to be maintained over time, money should be a stable measure of trust.12 David Hume described trust as a performance of promises, which perfectly captures the perfidy of inflation. Inflation is a devaluation of the future through broken promises.

Courtesy of Hedgeye

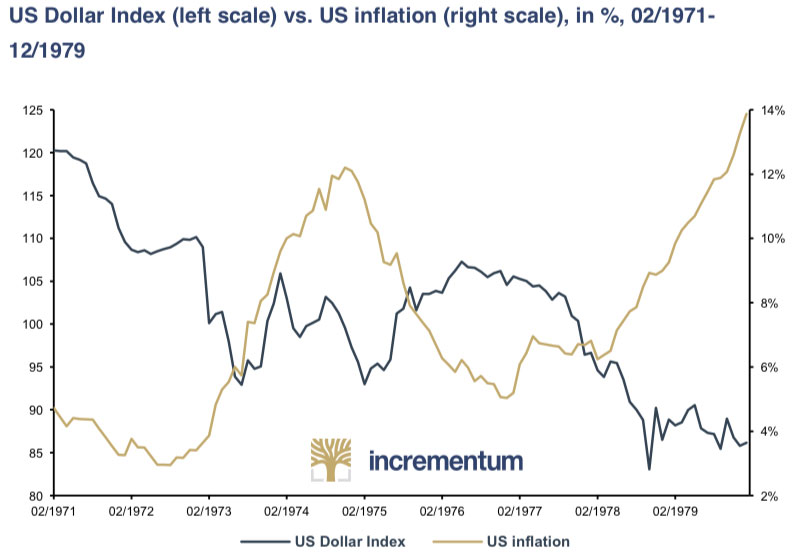

As our loyal readers know only too well, our current monetary system has been de facto uncovered and dematerialized for almost half a century now. All the more important, therefore, is the aspect of trust. Looking at monetary history from the point of view of confidence, one can see a history of ups and downs of dwindling and regained confidence. In the first decade after the final dematerialization of the monetary system in August 1971, the international monetary system was seriously shaken. Several US recessions, coupled with international conflicts and high price inflation, put the now uncovered world reserve currency under enormous pressure. International investors increasingly lost confidence in the US dollar. In 1978, US bonds had to be issued in the hard currencies of the Swiss franc and the German mark – the so-called Carter bonds.13

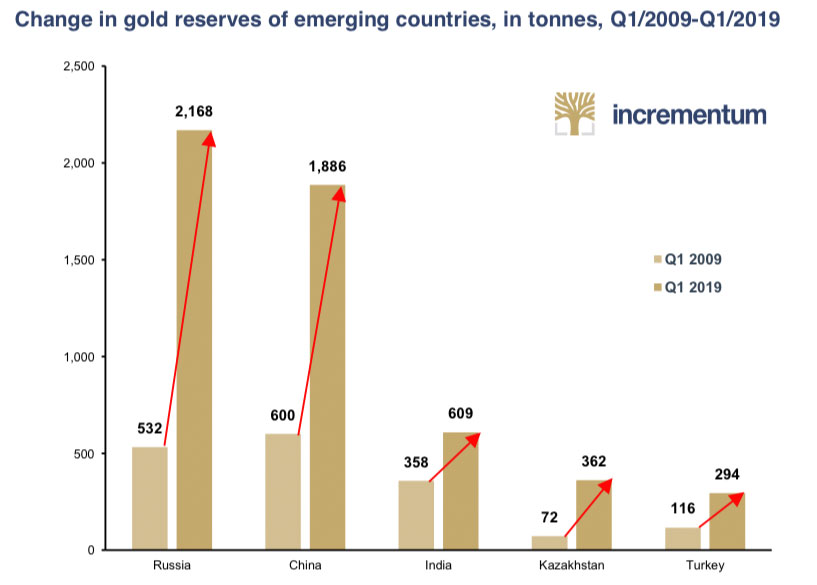

The Federal Reserve under the chairmanship of Paul Volcker was able to turn the tide, rehabilitate the US dollar, and successively restore confidence only through a highly restrictive monetary policy that led to sky-high interest rates and is still unparalleled today.14 The capital of trust in the US-centric order continued to be restored with the fall of the communist Eastern bloc in the early 1990s. In the struggle of systems, the “neoliberal capitalist system” associated with the USA emerged as the supposed victor. There remained a geopolitical tailwind for the US-centric world order until the mid-2000s. The influential US geostrategist Zbigniew Brzeziński said that the US was “the only comprehensive global superpower”15. But the events of the years 2008-2009 represented a serious turnaround. For the first time since the 1980s, confidence in the US-centric system was fundamentally eroded, as the global credit crisis originated from within the USA. Erosion of trust in international monetary policy The steady buying of gold and the repatriation of central bank gold clearly indicate growing mutual distrust among central banks. Last year we took up this topic under the heading “A turning of the tide in the global monetary architecture”16, and this year we are again dealing with the topic of de- dollarization, which has lost none of its relevance, in a separate chapter.17 The rising gold stocks of the Russian and Chinese central banks are not news to most people interested in gold.

Source: World Gold Council, Incrementum AG

In addition to the “usual suspects”, a growing number of other central banks are currently following the example of the “axis of gold”.18 An example is the recent tenfold increase in the Hungarian gold stock. The official announcement of the Hungarian central bank on its first gold purchases since 1986 states:

There’s nothing to add. It seems as if our Hungarian friends are attentive readers of the In Gold We Trust report! Further catalysts for emancipation from the US dollar are, among other things, the monetary and economic reprisals undertaken by the USA, which are occurring more and more obviously under the Trump administration. These include explicit sanctions, as in the cases of Russia and Iran, as well as political influence on the SWIFT payment processing system.20 Even in Germany, which is otherwise loyal to the US, for the first time voices are growing louder in favor of more self-confidence in matters of international currency policy. This is what the German Foreign Minister wrote in a guest article in the German Handelsblatt in autumn 2018:

And the criticism of the greenback’s currency monopoly is also gradually becoming louder on the part of the EU. In his “Speech on the State of the Union 2018”, EU Commission President Jean-Claude Juncker noted:

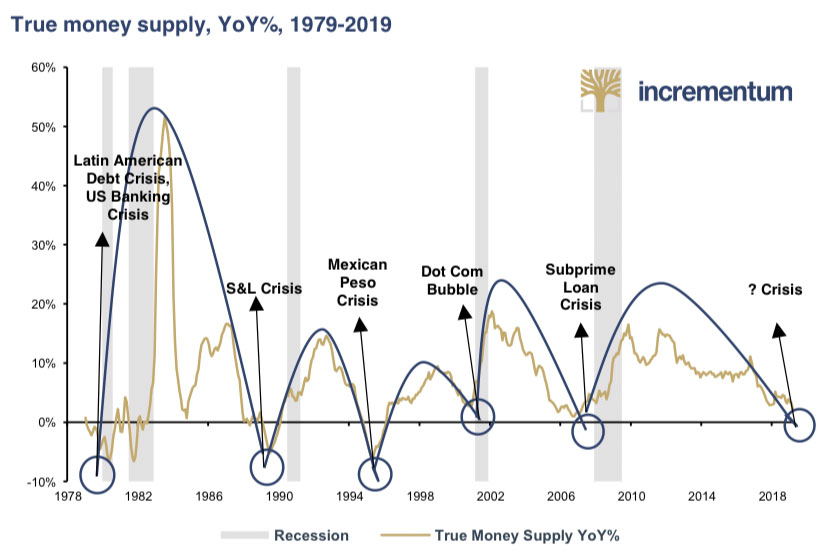

Building trust in new technologies As a consequence of the erosion of confidence in international monetary policy, new technologies are increasingly being examined with the aim of helping circumvent sanctions and achieve greater autonomy in international payments. Iran, for example, is reported to work on various blockchain projects that will make it easier to circumvent US sanctions.23 Moreover, an increasing number of private crypto projects in the gold sector are also worth mentioning in this context. The “Turning of the Tide in Technological Progress”, which we described in last year’s report, is thus making definite progress.24 However, these new technologies need to prove themselves over a longer period of time to earn trust for wider use. The Everything Bubble: A bubble of misguided trust Although there is increasing evidence at the international level that confidence in the US-centric world order is crumbling, the apparent loss of confidence has so far not been reflected in either a weak US dollar or a significant rise in the price of gold (in USD). How do we explain that? From our point of view, Donald Trump’s “all-in” economic policy contributes significantly to this. In the years following the financial crisis, global central banks flooded the economy with exorbitant monetary stimuli. Nearly 20trn USD of central bank money was created ex nihilo. Global stock markets were deliberately driven up in order to accelerate the so-called “wealth effect”. However, this did not seem to be having any effect in 2015, and stock markets began to stagger in the wake of fears of low growth.

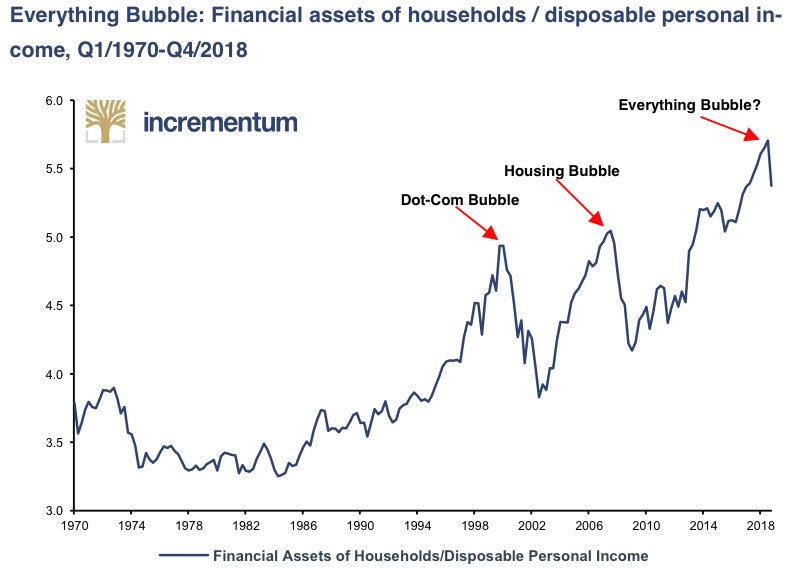

Courtesy of Hedgeye Everything Bubble? Housing Bubble Dot-Com Bubble

When we recall the 2016 election year, various indicators at the time seemed to point towards an economic slowdown and approaching US recession. The gold price acknowledged the foreseeable end of economic expansion and the renewal of monetary and fiscal stimuli with its first significant rally since the bear market that began in 2011-2012. On the fateful election night in November 2016, however, the momentum was temporarily halted. Yields at the long end of the bond yield curve rose, allowing the Federal Reserve to implement long-awaited rate hikes in subsequent quarters without having to invert the yield curve. With the rise in interest rates, the gold rally was halted, at least for the time being. Through massive tax relief and a change of mood on the part of many disillusioned voters, who often voted for Donald Trump because of economic dissatisfaction, the economic cycle could actually be extended once again. Not only the stock markets but also corporate bonds, luxury real estate, and works of art boomed. To describe this period, we have adopted Jesse Felder’s apt term “The Everything Bubble”.

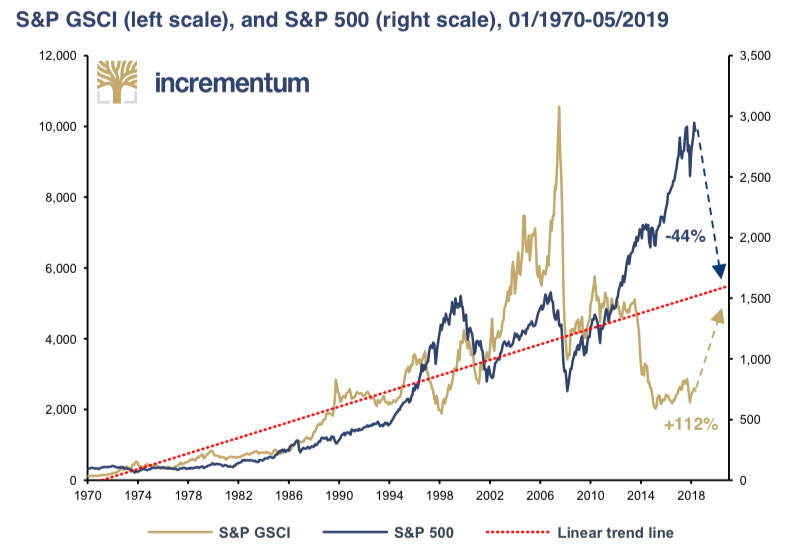

Everything Bubble: Financial assets of households / disposable personal in- come, Q1/1970-Q4/2018 Source: Federal Reserve St. Louis, Incrementum AG Alas, commodities remain the exception to the rule and still do not participate in the everything bubble. The extreme relative undervaluation of commodities compared to the stock market becomes evident in the next chart. It shows the development of the S&P GSCI and of the S&P 500, as well as their long-term upward trend line. To return to this trend line – which happens on average every 6 to 8 years – the S&P would have to fall by 44% and the GSCI to rise by 112%. This is a scenario that seems highly unlikely, if not impossible, at the moment. However, a glance at the following chart or at the history books puts this alleged impossibility into perspective.

Source: Prof. Dr. Torsten Dennin, Lynkeus Capital, Bloomberg, Incrementum AG

In any case, as long as the equity market party continues, trust in the credit-financed growth model seems intact. The President regularly exploits the all-time highs of US stock markets in the media, and investors and commentators praise the resurrection of the USA as a global economic locomotive. In the midst of a global economic slowdown, US consumers are being celebrated as “consumers of last resort”. Not even the permanently boiling trade conflict between China and the USA can spoil the mood of investors. But how sustainable is such an upswing, really? You don’t have to look too far below the surface of economic data to be suspicious of the sustainability of the recovery. The debt increases at the governmental and, in particular, at the corporate level continue to be largely ignored. This topic is dealt with in detail in the next chapter “The Status Quo of Gold”.25 Last year we therefore warned under the heading “The tide is turning in monetary policy” that the planned reduction of liquidity would inflict severe damage on the stock markets. This is exactly what happened in the fourth quarter of 2018: The stock markets suffered their biggest selloff in years and the Federal Reserve promptly announced that it would stop raising interest rates.

In fact, the long-announced normalization of the Federal Reserve’s balance sheet via QT (quantitative tightening), which according to Jerome Powell was still running “on autopilot” in December 2018, was cancelled at the next FOMC meeting. Once again, monetary policy was massively asymmetric: While in previous years the Federal Reserve had expanded its balance sheet by USD 3.7trn, the Federal Reserve is now expected to be able to reduce its balance sheet by only 0.7trn in total.

Source: Bloomberg, Incrementum AG

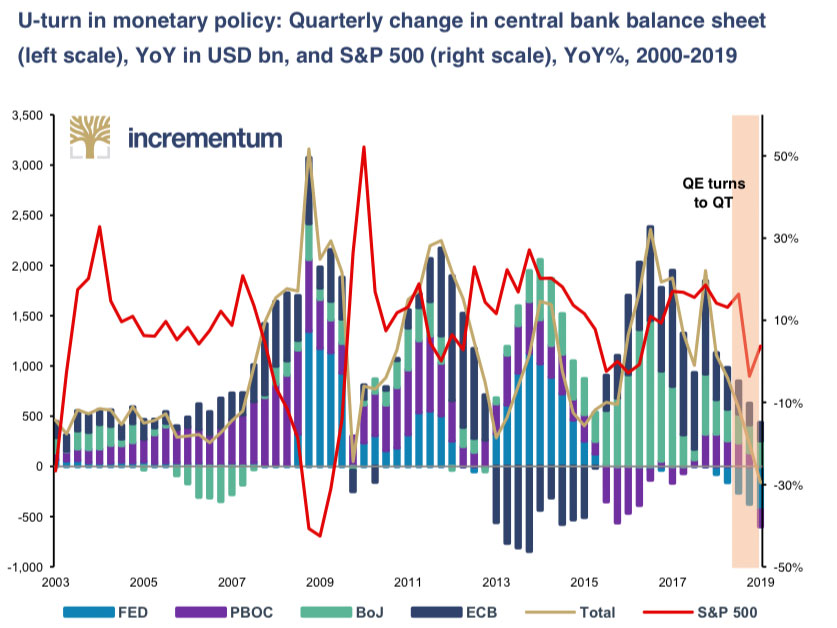

The pressure to print will continue to increase. Loss of confidence in monetary policy? How long can the current boom in financial markets be perpetuated? How long will market participants continue to trust the omnipotence of monetary authorities? When will the bubble of misguided trust burst? For the time being, global central banks have only paused the normalization of monetary policy and not (yet) reversed it. However, it has already been communicated several times that in the event of a renewed economic slowdown, the well-known expansive means of monetary policy will be used. However, there are two major differences compared to the last time:

At present, conventional risk investments such as equities are still enjoying the confidence of investors. This could change quickly if the current expansion, which has become the longest economic upswing in the history of the US, comes to an end. The fact that the coming recession could become extremely uncomfortable due to the starting position of economic fundamentals has already been expressed by many grandees of the capital market, such as Jeffrey Gundlach: “When the next recession comes there is going to be a lot of turmoil.”26 The closer the upcoming presidential elections come, the greater the pressure on the Federal Reserve from the Trump administration not to stall the upswing and to reopen the monetary floodgates. President Trump has cleverly positioned himself in the media by repeatedly criticizing the Federal Reserve for interest rate hikes and quantitative tightening. If there is serious economic slowdown, he will be able to pass the buck to the central bank and adorn himself with a false mantle of economic competence, especially if the Fed does not immediately implement the appropriate measures that he will propose. But as can be seen on the following chart, Federal Reserve and ECB – relative to the BoJ – seem to have plenteous leeway to further increase their balance sheets. But the independence of the Federal Reserve will also be increasingly tested by the opposition Democrats. The left wing of the party is strengthening and increasingly flirting with questionable monetary experiments that usually start with the buzzword MMT (“Modern Monetary Theory”).27 A Democratic victory in next year’s presidential election could bring on the perfect storm for the US economic model, which has so far been able to maintain a good mood among investors and the general perception of a humming economy through stock price inflation. All this could change abruptly with a political leftward slide. We will report on this potential in detail in the coming election year. In any case, our decision to link our four-year price forecast to the US President’s term was the right one, because the expanding interventionist measures and indirect and direct influence on monetary policy are obviously increasingly interlinking policy with the financial markets. Our updated scenarios and forecast can be found in the conclusion of this year’s In Gold We Trust report, “Quo Vadis, Aurum?” In Gold We Trust Popular trust in the idea that monetary policies can sustain growth and employment and that central banks have inflation under control will be seriously tested in the next recession. The spread of the loss of trust to other pillars of the Western world, such as the media, the financial system, and the judiciary could have devastating consequences.

When it comes to trust in specific investments, our vote – at least for a portion of the portfolio – is clear. Trust looks to the future, forms itself in the present, and feeds itself from the past. As monetary asset, gold can look back on a successful five-thousand-year history in which it was able to maintain its purchasing power over long periods of time and never became worthless. Gold is the universal reserve asset to which central banks, investors, and private individuals from every corner of the world and of every religion and every class return again and again. One thing should not go unsaid at this point: If our diagnosis is correct and trust is generally on the decline, this does not necessarily have to be negative. Although many of the developments we have noted should be regarded as worrying, we must not forget that trust levels in a society follow a cyclical pattern. Disappointment with familiar institutions may well allow the laying of the cornerstone for a more solid foundation in the future. Gold looks to a future in which the natural value of this unique precious metal is once again fully appreciated. In our opinion, the currently high trust granted into the skills of central bankers and the supposed strength of the US economy are the main reasons for the somewhat weak development of the yellow metal. If the omnipotence of the central banks or the credit-driven record upswing are called into question by the markets, this will herald a fundamental change in global patterns of thinking and help gold to old honors and new heights. Now we invite you to our annual tour de force and hope that you enjoy reading our 13th In Gold We Trust report as much as we enjoyed writing it. Yours truly,

Ronald-Peter Stoeferle and Mark J. Valek P. S. All previous issues of the In Gold We Trust report can be found in our archive.

3 Wikipedia entry “Trust“: On the etymology of trust: “Trust has been known as a word since the 16th century (Old High German: “fertruen”, Middle High German: “vertruwen”) and goes back to the Gothic trauan. The word “trust” belongs to the group of words around “faithful” = “strong”, “firm”, “fat”. In Greek this means “π ίστις” (pistis) (“faith”), in Latin “fiducia” (self-confidence) or “fides” (faithfulness). Thus, in ancient and medieval use, trust stands in the area of tension between good faith and faith (e.g. with Democritus, who demands not to trust everyone, but only the tried and tested). For Thomas Aquinas, “Trust is hope confirmed by experience for the fulfillment of expected conditions under the premise of trust in God.”. Our translation. 4 See Wikipedia entry “High trust and low trust societies”, as well as Stoeferle, Ronald, Hochreiter, Gregor and Taghizadegan, Rahim: Die Nullzinsfalle (The Zero-Interest Trap), FinanzBuch Verlag, 2019, chapter 3. 5 See Govier, Trudy: Social Trust and Human Communities. 1997, pp. 129 ff. 6 Haumer, Hans: Vertrauen. Angst und Hoffnung in einer unsicheren Welt (Trust. Fear and hope in an uncertain world). 2009, p. 101 7 See “Neil Howe: Super-bullish the U.S.A. in the 2030s. But between now and then...”, Macrovoices Interview, April 2019 8 See “Populism and its true root”, In Gold We Trust report 2017 9 See Gaulhofer, Karl: „So klappt es auch mit Feinden” (This is also how it works with enemies), Die Presse, April 10, 10 See All posts on the Claas Relotius case, spiegel.de 11 See Stoeferle, Ronald: Keynote Presentation at the European Gold Forum Zurich, April 2019 12 See Haumer, Hans: Vertrauen. Angst und Hoffnung in einer unsicheren Welt. (Trust. Fear and hope in an uncertain world). 2009, p. 85. 13 See U.S. Department of Treasury: “Resource Center – International – Exchange Stabilization Fund – History” 14 This year two chapters deal with this era of monetary history: (1) “The Relevance of John Exter”, including an interview with Barry Downs, John Exter’s son-in-law, and (2) “History Does (Not) Repeat Itself: Plaza Accord 2.0 at the Gates?” The two chapters are part of the “Extended Version” which you can download for free at https://ingoldwetrust.report/igwt-en/?lang=en. 15 Brzezinski, Zbigniew: The Grand Chessboard: American Primacy and Its Geostrategic Imperatives, p. 25 16 In Gold We Trust report 2018 17 This chapter is part of the “Extended Version” which you can download for free at https://ingoldwetrust.report/igwt- en/?lang=en. 18 James Rickards includes Iran, Turkey, Russia, and China. See Rickards, Jim: “Axis of Gold“, Daily Reckoning, December 20, 2016. 19 Press release: “Hungary’s Gold Reserve Increase Tenfold, Reaching Historical Levels“, Magyar Nemzeti Bank, October 16, 2018 20 See “Die Dominanz des Dollars weckt Unmut” (“The Dominance of the Dollar Arouses Discontent”), Neue Zürcher Zeitung, April 4, 2019 21 See Maas, Heiko: “Wir lassen nicht zu, dass die USA über unsere Köpfe hinweg handeln” (“We will not allow the United States to act over our heads”; guest commentary), Handelsblatt, August 21, 2018 22 Jean-Claude Juncker: “State of the Union 2018 - The hour of European sovereignty”, September 12, 2018 23 See “Iran in Talks With 8 Countries for Use of Cryptocurrency in Financial Transactions”, news.bitcoin.com, January 29, 2019 24 In Gold We Trust report 2018 25 This chapter is part of the “Extended Version” which you can download for free at https://ingoldwetrust.report/igwt- en/?lang=en. 26 See Interview with Jeffrey Gundlach, Yahoo!Finance, February 13, 2019 27 Evil tongues also speak of the Magical Money Tree.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)