Send this article to a friend:

April

29

2022

|

Send this article to a friend: April |

|

Building a Better Banking System

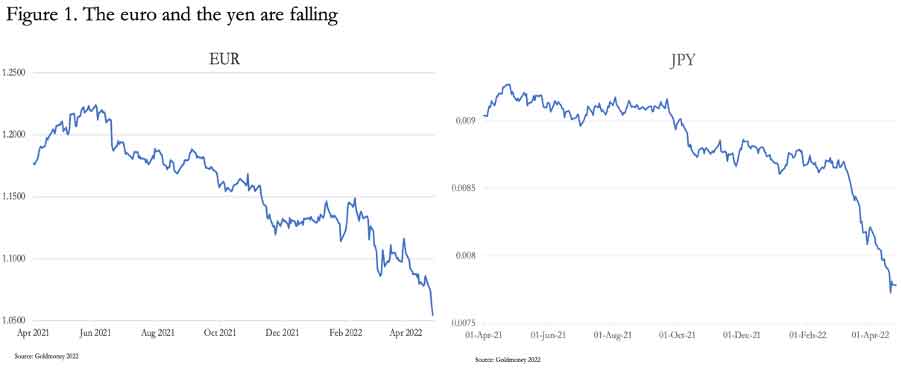

Economists of the Austrian school have argued that sound money would have prevented a crisis of this sort, and without it the crisis becomes inevitable. The argument for sound money, in other words, a credible gold coin exchange system for banknotes, has already been made. But the question remains over how bank credit, whose fluctuations for a long time have been behind the boom and bust of the business cycle, should be addressed. Some Austrians argue in favour of a dual banking system, split into separate functions of custodians of deposits and arrangers of finance. They say this arrangement would banish bank credit expansion and the destructive business cycle with it. But credit creation is not restricted to banks and is common in all economic activities. Banning banks from dealing in credit cuts across established law over credit which has evolved since Roman times. By doing so, banks of deposit would probably fail as a permanent solution and could turn out to be impractical as well. I suggest that there is a better answer, which is to remove limited liability status from banks and other dealers in credit. They would be less likely to carry excessive balance sheets relative to their own capital. This simple measure would have the merit of making credit available without the excesses we have seen in the past and render much of current banking regulation unnecessary. Introduction I have recently entered a debate with some friends about what constitutes a sound banking system. We all follow the a priori reasoning of the Austrian school of economics. Readers familiar with the argument will know the position adopted by some adherents: banking should be split into deposit taking on a custody basis and separately for the arrangement of loans, providing capital for production from savings. In such a banking system, the production of bank credit out of thin air no longer occurs, along with the economic disruption from variations in its quantity. The Austrian school position on inflation of currency and credit has been broadly unchanged since the 1930s, when Ludwig von Mises became more of a force outside his native Austria. Between von Mises and his fellow Austrians, such as Hayek who taught at the London School of Economics, the profession was made aware of the link between the business cycle of boom and bust, changes in the level of bank credit, and fluctuations in interest rates. Austrian business cycle theory was pushed aside by the rise of Keynesian macroeconomics, following Keynes’s publication of The General Theory. In 1936 when it was published, Keynes had discarded Say’s law, which set out the classical position on the division of labour. And he advocated a move away from financing production through savings. In other words, he became an inflationist, the antithesis of Austrianism. Keynes became fashionable with socialising governments, while Austrian business cycle theory was side-lined. Following Bretton Woods in 1944, the global economy stabilised and recovered under a dollar standard, only notionally tied to gold. That link was finally severed in 1971, since when currencies linked to the dollar, which in practice was all of them in the free world, have lost over ninety-five per cent of their purchasing power relative to that of gold. And other than the odd scare, such as the Lehman crisis, the world appears to have been cured of depressions. But… We are sitting on the edge of a systemic failure A consequence of the gathering energy, commodity, and food crisis is that increasing numbers of independent observers now see inflation, by which they mean rising producer and consumer prices, rising far more than previously thought likely. They are just starting to understand the consequences for interest rates, and the distant possibility that the whole thing might get out of control. In the 1970s it took years of markets battling statist control of monetary policies before central banks threw in the towel and Paul Volcker raised the Fed’s funds rate to over 19%. In those days, the UK Treasury was in control of Britain’s interest rate policy, and to be fair to the Bank of England, all it found in the Chancellor of the day was a three wise monkeys act with respect to market reality. Eventually, the Bank would get its way, raising interest rates to permit the Labour government’s profligacy to be funded. Hence, there were coupons on long-dated gilts of 15% and more. Imagine that today! Yet that is the direction of travel. The other thorny issue was the discrediting of Keynesian economics in favour of monetarism. Suddenly, Milton Friedman was on our TV screens telling us about why money supply was so important to prices, and why the solution was to index everything. But now Keynes is back with a vengeance. Friedman was only half correct in his analysis because money supply is just part of the story behind a currency’s purchasing power. The other is humanity’s view of a fiat currency, a factor not seen under the gold standards upon which monetarist theory was based. Bluntly put, irrespective of the quantity in circulation, if the population rejects it, then the state’s unbacked currency has no value in terms of the goods and services for which governments expect it to be exchanged. That was why Volcker had to raise the FFR to over 19%. It was a message to the people: do you want to reject the dollar, or do you want to save it and earn 20%? If he had left it much later, the answer might have been different. The inflation problem today is arguably worse than it was in the 1970s. Then, financial assets had endured substantial bear markets (the FT 30 Share Index lost 75% top to bottom), there was a commercial property and banking crisis in the UK in late-1973, and the IMF had to divert funds from rescuing impecunious governments in emerging economies to bail out the UK. But never did the civilised world face the prospect of the food shortages and the starvation we will almost certainly see later this year. Like rabbits caught in the headlights of a rapidly approaching truck, central banks are frozen into inaction. If they permit interest rates to rise, they undermine their own balance sheets. And because collateral held against loans at the larger commercial banks is principally financial assets, the commercial banks risk failing as well. Furthermore, the central banks’ common mandate is to maintain full employment consistent with CPI inflation at 2%, so they have no clear authorisation to tackle inflation of prices while ignoring the consequences for unemployment. In short, we face the likelihood of an impending crisis. It seems unlikely to start with the Fed or the Bank of England. More likely, it will be the Bank of Japan and the ECB’s euro system that will descend into crisis first as they are forced to emerge from negative rates. On 18 March the BOJ’s Statement on Monetary Policy reaffirmed the negative interest rate policy of -0.1%, and a commitment to buy unlimited quantities of 10-year Japanese Government Bonds to maintain a yield of zero per cent. Under pressure from markets, that was raised to 0.25% on 20 April. Consequently, the yen has fallen against the dollar at the fastest rate seen in modern times. Similarly, the ECB has its head in the sand. On 18 April, despite soaring producer price inflation and the obvious impact on consumer prices down the line, it reaffirmed its minus 0.5% deposit rate. With respect to quantitative easing, the ECB continues with its asset purchase programme, admittedly at a reduced rate, expecting it to conclude in the third quarter. It’s rather like St Augustin’s prayer: “Oh master, make me chaste and celibate — but not yet”. Both the BOJ and the ECB will have to mend their balance sheets if they fail to supress interest rates and bond yields. In the case of the BOJ, by indulging in continual QE from the year 2000 it has turned itself into a massive investment fund. The ECB has also done so but only since the Lehman crisis, and both central banks are now exposed to the vagaries of mark-to-market values. In the event of failure, the BOJ has a government to turn too, but the ECB does not. Its shareholders are the National Central Banks, which are afflicted with the same problem. Even worse, the major international banks in both the Eurozone and Japan are the most highly leveraged in the world, with both Japan’s and the Eurozone’s G-SIBs averaging asset to equity ratios of more than twenty times. Both the BOJ and the ECB cannot afford to let interest rates rise. But when you see Germany’s producer prices rising at over 30% and even Spain’s recorded at 46%, you know the gig is up. In Japan, consumer prices are heavily subsidised, reducing the apparent rate of consumer price inflation. But now that commodity and energy prices are soaring, there can be no question that Japan is horribly exposed to higher energy and commodity prices. If the BOJ and the ECB persist with current monetary policies, they will undermine their currencies, a trend which is already evident, as the two charts in Figure 1 illustrate.

Confirmed in the foreign exchanges, both the ECB and BOJ have chosen to protect themselves from rising interest rates instead of preserving the exchange values of their currencies. But falling exchange rates only serve to increase the pressures on the central banks to raise interest rates down the line, so long as they are prepared to see the destruction of their currencies’ purchasing power accelerate. Therefore, sooner or later interest rates and bond yields in euros and yen will rise. Their entire banking systems will face collapse from the top down, as the heavily financialised G-SIBs find their leveraged financial assets and loan collateral securing it all begin to implode. And the realisation of systemic counterparty risk from two of the largest economic units can be added to the woes faced by the banking systems in all other Western nations. The emergence of a crisis could be rapid, leaving the existing banking system in tatters — or even destroyed. The question then to be addressed is the subject of our debate today: can a new banking system be designed from the ground up so that it cannot fail again? The root of the problem is unsound money. A new banking system will not last while governments have control over money. Whether it be because of democratic demands or pure malfeasance, governments can never resist the temptation to use a currency as a source of funds. But other things must happen as well. Governments must stop intervening in their economies, limiting their involvement and the burden on production of goods and services to a bare minimum. They must give free rein to free markets and place monetary stability at the top of national priorities. It is enough of a leap of faith that an economic, financial, and banking crisis will force governments to understand and embrace these realities. It is yet a further leap of faith to assume that banking reform will be successful. However, given the increasing risk of such an event overtaking us, it behoves us to look at how a future banking system should operate. The Austrian economists’ solution Austrian economists, such as Ludwig von Mises recognised that the ills that led to a cycle of business behaviour originated in changes in the quantity of bank credit. Increases in bank credit had the effect of artificially stimulating economic activity, leading to debasement of the currency. The mistake made by twentieth-century economists was to attribute the consequential booms and busts in a gold coin backed currency environment to business itself instead of variations in bank credit. In his Critique of Interventionism, Mises wrote: “Governments and political parties are committed to the idea that it is good policy to lower the rate of interest below the height it would attain on a free market. And they believe that the expansion of bank credit is the right means to produce this desired effect. They do not realise that the boom which they artificially create by such credit expansion must finally result in the catastrophe of the depression.” Mises was identifying the reason why the business cycle existed: it is down to the money. Therefore, his followers concluded, the way to deal with the problem was to not permit the banks to create credit in the first place. But while being a pedant with respect to currency inflation, Mises was not so prescriptive over bank credit. In his essay on Senior’s Lectures on Monetary Problems Mises was more accommodating: “The pith of the problem lies in the deposit policy. Banks which promise no more than they couldn’t fulfil without the extraordinary assistance from the central bank never jeopardise the stability of the country’s currency. And even the other banks who have been imprudent enough to assume liabilities which they cannot meet are only a danger when the central bank tries to assist them. If the central bank were to leave them to their fate their peculiar embarrassment would not have any effect on foreign exchanges.” [My emphasis].[i] That is surely the point. The evil is the intervention by the central bank, as much if not more so than bank credit expansion itself. But it is common for followers of the Austrian School to attack credit creation as the real evil which must be stopped, without, perhaps, paying sufficient attention to the consequences of the actions of the Authorities. Furthermore, they criticise government regulators and the banks for not making it clear to their depositors that they are merely creditors of the bank when they believe they are custodians, and that they do not own deposits as their own property. Consequently, economists of the Austrian school suggest that the solution is a dual banking system, where a bank acts either as a custodian of a fee-paying depositor’s money or as an agent arranging for the loan of money to borrowers sourced from investors independent from its own balance sheet for fees or commission. But not both. And therefore, no bank credit is created. Immediately we can anticipate a practical problem. Following the value destruction from a collapse of the entire fiat currency system, fewer depositors today out of the total number than in the history of banking possess gold and silver coin and bullion to deposit in a bank on a custodial basis. And those that do will almost certainly be wary of any banking system, sound or not, preferring to store them in insured vaults or at home. If by deposits is meant banknotes backed credibly by the issuer’s gold reserves and exchangeable for specie in specie’s place, then it may be cheaper and perceived to be more secure for individuals to resort to safe deposit boxes to store bundles of notes. Banks of deposit, by which we mean a bank whose deposit reserves are fully backed by customers’ specie have existed in the past. The Bank of Amsterdam, established in 1609, was such an institution. But over time, it relaxed the 100% specie backing rule, and after the Dutch East India Company defaulted on loans from the bank, in 1790 the bank declared itself insolvent. In its early days, there was a further disadvantage with coins submitted from all over Europe, mostly clipped, so deposits were accepted by weight and had to be recoined. It may be argued by Austrian libertarians that a new start will allow strict regulations to be introduced at the outset to stop a bank from being distracted from a purely custodial role to create credit, like the Bank of Amsterdam. But the imposition of regulations goes against the libertarian spirit of the Austrian writers, which is to promote unregulated markets free from state interference. Furthermore, we could argue that attempts to persuade the state to introduce new rules will almost certainly be corrupted by the same lobbying which over time has corrupted the present system. Given the circumstances under which a new banking system will be required, the currency will need to be secured, it must be widely in circulation, and credit should be available for businesses to provide products for consumption. Credit is needed because expense is incurred by any business before an income stream from product sales is obtained. It is difficult to envisage this happening through a new loan market, which necessarily will not be readily accessible for local businesses that always make up the bulk of economic activity. In the past, these have been financed by small cooperative banks, which under a dual banking system will presumably not be permitted to exist. As the experience of the Bank of Amsterdam showed, over time the strictest restrictions on credit creation can become eroded. In more modern times and in a related context we saw the abandonment of the Glass-Steagall Act, which separated commercial banking from investment banking, repealed after only five decades. The lesson of experience, surely, is to frame future legislation that we can all live with. And to do that, we must understand the nature of credit and the natural laws that apply to it. Roman, or natural law with respect to credit Credit has existed since the end of barter. Money, currency and self-evidently credit itself are all credit. That specie is credit is a matter of fact: gold and silver coin in possession represents the unspent portion of production or earnings. It is regarded as money proper because it is the only form of credit with no counterparty risk. Currency is the credit of the issuer and bank deposits are bank liabilities (credit) in favour of a bank’s deposit customers. Credit is anything which is of no direct use, but which is taken in exchange for something else in the belief or confidence that we have the right to exchange it away again. Credit is therefore the right or property of demanding something else when we require it. It is the right to a future payment, and it must be particularly observed that credit is not the transfer of something, but it is the name of a certain species of rights or property. During Roman times, the earlier rulings of jurors were embodied in law at the time of the emperor Justinian (529—565AD). Thus, the findings of Ulpian (170—228AD) with respect to bank credit are incorporated in the code. The difference between a regular deposit contract for a specific good, and an irregular deposit for a fungible item was defined by Ulpian:

1,800 years ago, Ulpian codified what was then established practice. The distinction between custody and a loan contract was already clear. The banker had a duty to repay the money on demand, but not necessarily the same money deposited. He was therefore free to take the deposited money to do what he wanted with it, always regarding the duty to repay it. As well as money, there are goods which can be loaned and not remain the lender’s property because they are lent to be consumed. The property is transferred to the borrower, and the borrower has an obligation to repay, either by returning similar goods or an agreed amount of money in their place. In Roman law, this is a Mutuum, differing from a Commodatum, when in the latter instance the borrower contracts to return the same article and its possession does not change in the transaction. All commercial loans are mutua, whether payment in kind for consumable items or money to discharge the debt are involved. Where that payment is not yet discharged, it is credit and nothing else. And here we come across an important distinction not commonly understood: a debt is never the money owed by the debtor, but it is always the personal duty, the obligation, to pay the money. The common and widespread fallacy that a debt is money owed and belongs to the creditor is expressly provided against in Roman law. The essence of an obligation does not consist in making any specific goods property, but it binds someone to give us something. The money continues to be the absolute property of the debtor which he may spend or part with until he transfers the property in it to the creditor. But the debt or the duty to pay exists whether the debtor has any money to pay it with or not. The consolidation of Roman law under Justinian occurred after Rome had abandoned Britain in the fourth century and England subsequently developed its own legal system, split between common law and the Court of Chancery. The effect of the reforming acts of 1873 and more particularly 1875 was for the common law relating to credit to be superseded by equity, bringing it in line with the Roman law of Justinian which had already become the basis of all European law for credit. Debt and credit have come to mean the same thing, meaning a right of action against a person for a sum of money.[iii] While in economics the focus has been on the role of banks as dealers in credit, credit has a far wider role in economics than banking. Not only is the entire monetary system based on credit, but all actions of individuals transferring ownership in property that do not involve immediate settlement are governed by the same laws. These laws must be taken into consideration in any reform of the banking system. And removing the right from anyone in business to act in accordance with the long-established practice still available to everyone else will create substantial difficulties at the very least and goes against the spirit and natural laws that have evolved over two millennia of accumulated practice. Those of us that think it would be a simple matter to design a new banking system are probably insufficiently aware of the difficulties of overturning the entrenched legal position of Roman, or natural law. The practical design of a new banking system So far, this article has highlighted some of the difficulties involved with the abolition of bank credit, which have been assumed away by those of us recommending that banking be separated into deposit taking and the arranging of finance. While the intention is good, the banning of one class of business activity from dealing in credit while permitting everyone else to do so is surely inequitable. Proof of the difficulties in doing so can also be seen from the emergence of shadow banking, where dealing in credit is not covered by state licencing, thereby avoiding, or evading regulatory control. And surely, apart from the practical difficulties of framing new legislation, a solution that requires even stricter regulation is inconsistent with the free-market ethos championed by Austrian economists. One could argue, as Austrians do, that a bank of deposit is more honest with the public than a bank free to use money deposited with it as it sees fit. But aside from the threat that future laws and regulations would almost certainly threaten the status of custodial deposits in the banking system, après le deluge, would ordinary people not prefer to keep their deposits away from a bank which will have to charge fees to provide a custodial service? And as a starting point, so few people today actually possess specie, that custodial deposits would either be in bank notes (in sealed packages or identified by their numbers) or backed by deposits at the note-issuing bank. And that, surely, would require the note-issuing bank to offer free conversion of its notes into gold or silver coin. That being the case, why not merely maintain a deposit account at the central bank, and do away with the need for a custodial deposit-taking bank altogether? But that merely hands yet more power to a central bank, and central banks are already planning on these lines with the development of central bank digital currencies. The intention is certainly not in accordance with a movement towards free markets but by bypassing commercial banks the intention is to exercise even greater control over how economic actors deploy the state’s currency. It must be always understood that it will be the state that sets a post-apocalypse framework, and that the abolition of commercial banks as dealers in credit will play into the state’s controlling hands. This brings us to the point von Mises makes, quoted above from his critique of Nassau Senior’s lectures at the LSE in 1931. It is not the fluctuations of bank credit which destabilises a currency, but the policies of a central bank attempting to manage the outcome. To this we can add the whole statist apparatus which to impart stability to an inherently unstable banking system has played down its risks and misled the public over the role of banks as dealers in credit. Deposit protection for the little people is with that in mind. It would be far better, surely, to have a banking system that operates in accordance with long establish law and practice where people were encouraged to understand the risks rather than have them covered up. The reason Japanese and Eurozone G-SIBs make no attempt to reduce their balance sheet assets to equity leverage from over twenty times is that the shareholders enjoy limited liability. This means that a bank can take risks in the knowledge that if things go wrong, shareholders will lose no more than their investment in the bank. Worse still, there is a growing understanding that if the worst happens the central bank always will bail a bank out (or in). And the business continues, and the shareholders are left with something. If there is a solution, it could be very simple. Dealers in credit must lose the protection of limited liability. It is perfectly possible to insist that dealers in credit of any kidney act as partnerships, with at least some of the partners exposed to unlimited liability. They should be permitted to have limited partners as a source of capital funding, but the key point is that bankers must always be acutely aware of the risks involved in dealing in credit and excessive leverage. Under a partnership regime, banks will be smaller, less leveraged, and likely to be more numerous. And with less leverage, the fluctuations of bank credit which Austrian economists correctly identify as the reason behind the business cycle of boom and bust will be considerably moderated. Banks will always fail, but in a diverse modestly geared banking system failures will have only a limited impact. — [i] Senior’s Lectures on Monetary Problems, a critique by von Mises published in the Economic Journal (September 1933) Nassau Senior delivered nine lectures on money and international trade at the London School of Economics in 1931 [ii] As translated and quoted in de Soto’s Money, Bank Credit, and Economic Cycles pp. 26—27. [iii] As defined for the Royal Commissioners in the Digest of the Laws of Bills of Exchange, Bank Notes, &c. as quoted in HD Macleod’s The Elements of Banking.

|

Send this article to a friend:

|

|

|

This article anticipates the rapidly approaching time when we might be engulfed in a combined currency, asset, and banking crisis. It is becoming clear that such an event can no longer be ruled out.

This article anticipates the rapidly approaching time when we might be engulfed in a combined currency, asset, and banking crisis. It is becoming clear that such an event can no longer be ruled out.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)