Send this article to a friend:

April

07

2020

|

Send this article to a friend: April |

|

Credit Markets – The Waiting Game

After the first inter-meeting rate cut in early March, we opined that further rate cuts were a near certainty and that “not-QE” would swiftly morph into “QE, next iteration” (see Rate Cutters Unanimous for the details). As it turned out, the monetary mandarins did not even wait for the official FOMC meeting before deciding to throw everything and the kitchen sink at the markets. Not only were rates insta-ZIRPed, but “not-QE” became “QE on steroids, plus”.

The federal debt monetization machinery goes into orbit. Moon landing next? The “plus” stands for the alphabet soup of additional support programs for various slices of the credit markets, ranging from money markets to commercial paper to corporate bonds (investment grade only – for now). Alan Greenspan once said in Congressional testimony that if need be, the Fed would one day even “monetize oxen” – he may well live to see it. What spooked the central bank was clearly the fact that corporate credit markets froze in response to the stock market crash and the lockdown measures. The latter have left a great many companies bereft of cash flows, not an ideal situation considering that trillions in corporate debt have to be refinanced in coming months and years. We have long argued that burgeoning corporate debt was the Achilles heel of the bubble, and this remains the case. When the stock market crash started, money initially continued to flow into investment grade corporate bonds. LQD (investment grade corporate bond ETF) still made new highs in early March, while stocks were already in free-fall. But that didn’t last, and in less than two weeks LQD not only joined the crash, but began to trade at unprecedentedly large discounts to its NAV. Critics of the proliferation of ETFs long predicted that once push came to shove, the disparity in the liquidity of ETFs and the liquidity of their underlying holdings would lead to major dislocations and trigger negative feedback loops. Although that seems more than obvious, a number of prominent sell-side analysts vehemently disputed that something like this was likely to happen. And then it happened (LQD was by no means the only ETF suffering such price distortions).

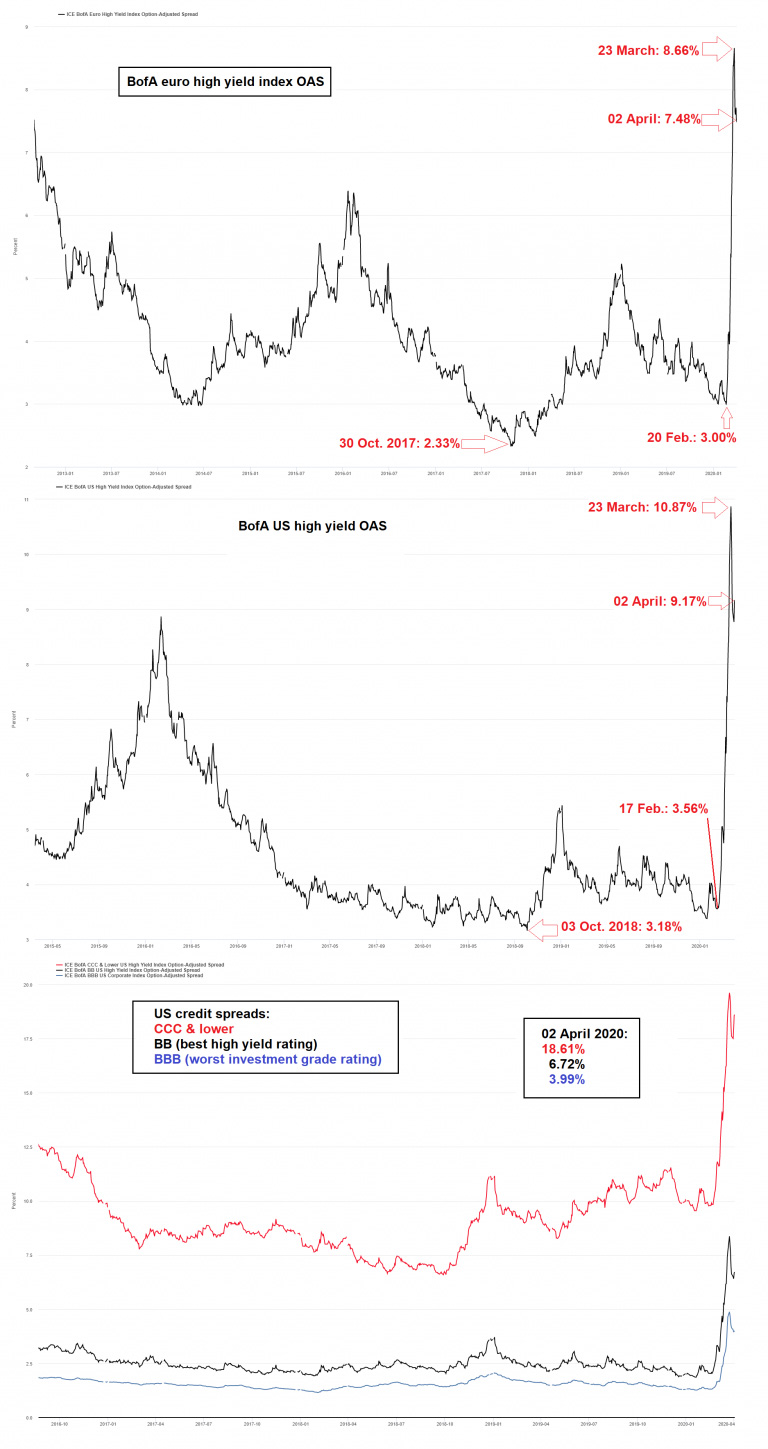

LQD enjoyed a brief moment of Wile E. Coyote-type weightlessness before belatedly joining the crash. It is worth noting that the Fed singled out LQD as an ETF it would also buy – presumably to neutralize it as a source of bond selling. This has led to a strong rebound, but it has so far failed to overcome the 200-day moving average. From a technical perspective, the success of this rescue operation is not a fait accompli just yet. The recent interventions by the Fed and the ECB nevertheless did unclog the primary market for IG issuers, and even a few junk bond issuers were able to sell new bonds. In fact, year-to-date US IG bond issuance is up 63% y/y, which is quite remarkable. The by far biggest new bond issues were placed by companies the revenues of which are not directly affected by the lockdown, such as telecoms, utilities, health care providers, pharmaceuticals, food & beverages companies, etc. Higher yields attracted brisk demand. Despite this burst in bond issuance, credit spreads indicate that the situation remains dicey. Here are various high yield spreads:

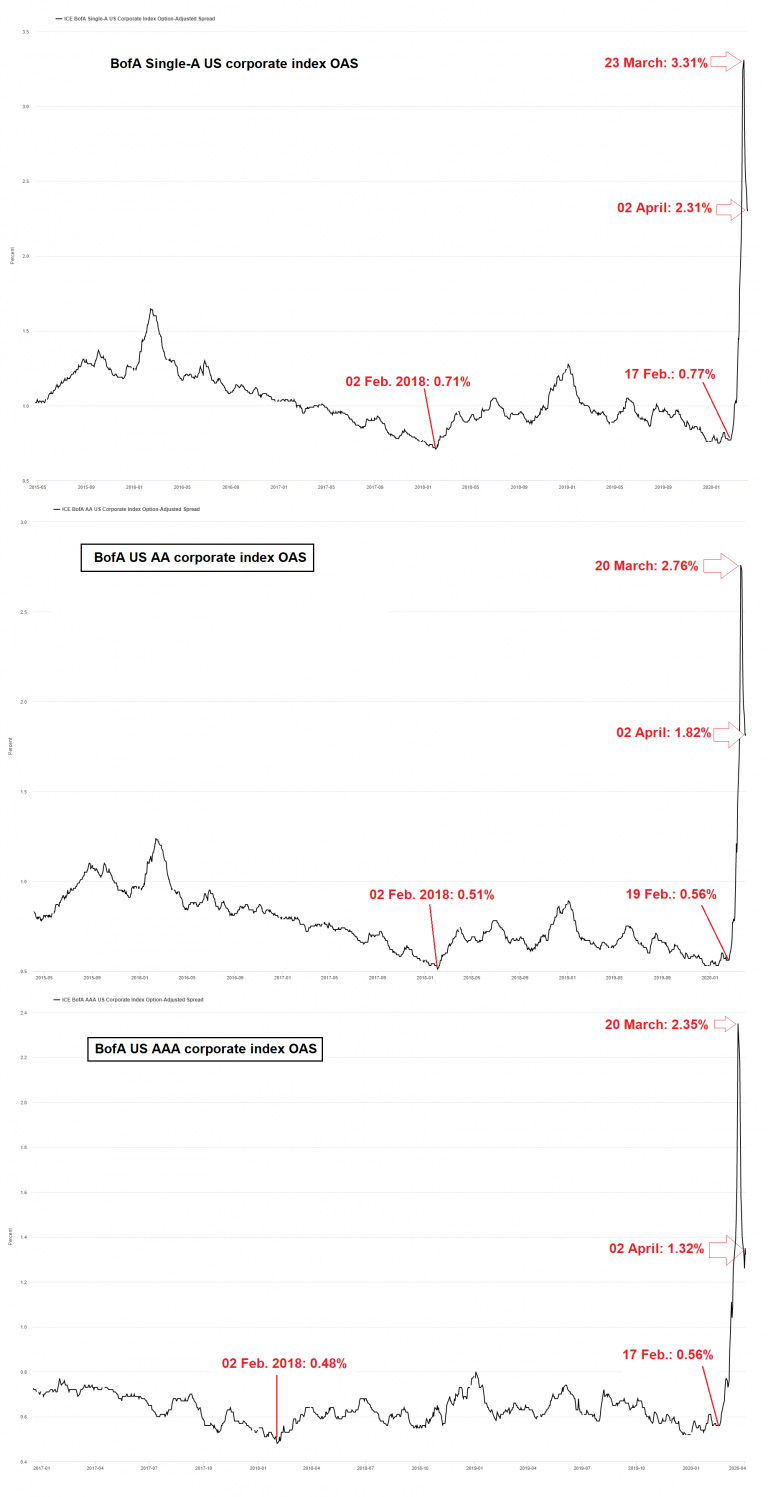

Option-adjusted spreads, from the top: euro area corporate high yield index, US corporate HY index, CCC and lower, BB, and BBB (the lowest investment grade rating; more than 50% of all outstanding IG bonds are rated BBB. Since BBB-rated bonds are just a one-notch downgrade away from being designated junk, their spreads are “sticky”). While high yield spreads have pulled back a little bit since their highs on 20/23 March, this remains a precarious situation. Not surprisingly, spreads at the upper end of the investment grade universe have come in a lot more on a relative basis, but their levels also remain a far cry from the status quo ante:

Option-adjusted spreads on top-rated US investment grade corporate bonds, from single-A to AAA. IG bonds receive direct support from the Fed, which has emboldened buyers who gobbled up $111 billion in new supply last week alone. And yet, IG spreads are still at their widest since the 2008 crisis (or since the 2011 euro area debt crisis in the case of single-A spreads).

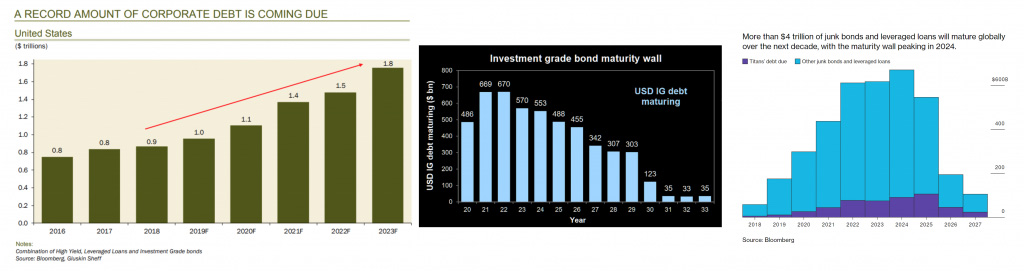

Dr. Powell dispenses medicine. Rumor has it he may be a quack. Waiting Game One could probably call this a half-exploded powder keg. Obviously, much will depend on how much longer it takes for the pandemic to recede and some semblance of normalcy to return. On that front some tentative improvements are becoming detectable, as the expansion in the number of new cases and COVID-19-related fatalities seems to be slowing down in some of the hardest-hit European countries. Alas, even in the best case, we are still weeks away from the lifting of restrictions. In the meantime there has been a wave of downgrades and more are probably on the way. All sorts of payments will no longer be made, as government measures cannot possibly replace everything; and ultimately there is no “replacement”, but only redistribution. Governments produce no resources of their own. They can only take them from the private sector by taxation, borrowing or inflation and alter their distribution. Many companies are bound to default and the longer it takes for economic activity to resume, the more defaults will occur. It cannot be taken for granted that the surge in investor demand in the wake of the recent central bank and government interventions will persist and the “wall of maturities” continues to loom:

Looming corporate debt maturities: 1. US IG bonds, HY bonds and leveraged loans combined; 2. US IG bonds; 3. global HY bonds and leveraged loans. The actual figures are probably somewhat higher, as the first and third charts are a bit dated by now. There is inter alia also a feedback loop between stock prices and corporate debt prices. If stock markets continue to weaken, corporate bonds are likely to be affected as well. With new debt issues more expensive, it is in turn becoming a lot more difficult to justify debt-funded dividend payments and buybacks (in fact, it seems stock buybacks are coming to a screeching halt). Investor demand for all sorts of debt issued by governments and government-related entities was recently also extremely strong. There is no guarantee that this will continue. The euro area debt crisis has already demonstrated that government debt is not immune against growing risk aversion (note that CDS on developed market government debt have recently begun to rise). In addition to this, we now have enormous amounts of money creation by central banks coinciding with a collapse in demand and supply. Declining inflation expectations suggest that rising demand for money is holding price inflation in check for the time being, but it cannot be ruled out that it will eventually accelerate. This may be a more distant threat, but not one that should be dismissed out of hand. Unintended Consequences The Fed’s attempts to bolster liquidity have already produced unintended consequences. Apparently its purchases of agency MBS have blown up the hedges of several leveraged mortgage REITs. Even companies dabbling mostly in the very same “risk-free” agency bonds the Fed is buying have run into trouble as a result:

Annaly Capital Management is usually regarded as a well-managed and rather boring dividend stock. The vast bulk of its assets consist of US agency bonds (MBS issued by the GSEs), which are de facto guaranteed by the US Treasury. MBS purchases by the Fed seem to have led to NLY and other mortgage REITS being inundated with margin calls on their hedges and suddenly these boring stocks have crashed. We are not sure if this is a buying opportunity or a trap, as detailed information on the severity of the problem has not been revealed yet. We mention this because it illustrates that in today’s complex credit markets with their many highly leveraged players there are always nasty surprises lurking somewhere, and often in places where one would not expect them to lurk. As an aside, even though this is not the first time something of this sort is happening, it strikes us as quite funny that companies can be threatened by “hedges” meant to protect their positions. Conclusion Central bank interventions have temporarily put an end to the deep freeze in primary markets, but time is not on the side of borrowers with weak balance sheets, nor is it on the side of investors. There are a great many corporate “zombie” borrowers out there, which are dependent on the willingness of market participants to refinance their debt. A vicious circle of self-reinforcing feedback loops can easily get underway despite all efforts to arrest such a development.

What’s left of the Icarus is approaching heavy weather.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)