Send this article to a friend:

April

05

2018

|

Send this article to a friend: April |

|

Why Oil Producers Are Liking $60/barrel Over $100/barrel

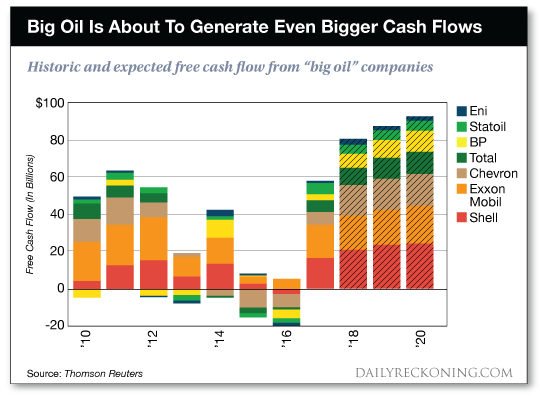

These traits are a recipe for a successful investment. And over the next several years, there is one surprising industry who could offer investors all three. Can you guess which one I’m talking about? Believe it or not, I’m talking about big oil! Cash flows at the major oil companies were strong in 2017, and they’re set to surge even higher starting in 2018. That’s because as a group, these companies are going to generate far more cash flow at $60 per barrel oil than they ever did when oil was $100 per barrel. And the best part for us, the share prices of these companies do not currently reflect these facts. Take a look for yourself…

Like every commodity business, this is a cyclical one, and for “big oil” the next three years are going to be the sweet spot in that cycle. Now let’s talk about why. 3 Reasons Why $60/Barrel Is Better Than $100/Barrel Reason #1: Major Projects Are Finally Coming On-Stream — With everyone buying into the idea that $100 per barrel oil was going to be the new normal, the period from 2011 through 2013 saw the largest number of mega-projects being sanctioned in the history of the oil industry. Those mega-projects required tens of billions of dollars of spending and took years to complete. Well guess what? Those projects are now coming onto production and the oil majors are finally going to be generating cash flow from the billions and billions of dollars that had been tied up as the projects were built but left idle. Reason #2: Cost Inflation From The Boom Has Receded — There is a reason we are all familiar with the concept that in a gold rush, you want to be in the business of selling picks and shovels, not digging for gold. That’s because the 170 year-old saying still rings true. You can charge exorbitant prices when you sell supplies and services during a boom. And the same rings true in the oil market. When oil prices were at $100 per barrel, competition for services was extreme and costs got out of hand. (I personally witnessed flocks of men in their early 20s with little training bring down six-figure incomes during the Bakken Boom.) Today, with activity levels much lower, these service costs are greatly reduced. That significantly reduces the cash that the oil majors need to spend on development. For a perfect example, consider that the day rate for an offshore semi-submersible drilling rig has gone from over $400,000 per day in 2014 to less than $150,000 per day today.1 Pair this reduction with massive layoffs at the oil majors themselves and you get a big reduction in total cash outflows. Reason #3: Backwardation Is Restraining Capital Investment — The oil futures market is currently in a severe state of backwardation — meaning futures contracts on oil are selling for less than the market price of oil today. This is keeping oil companies from hedging future production. (To increase certainty of future cash flows, oil producers typically like to hedge a significant percentage of their future production.) So with less hedging in place (and future cash flows uncertain), companies are also reluctant to commit to large capital expenditures. That has a further positive impact on service costs today and will help the price of oil in the future since it decreases future production. This Upswing In Cash Flows Is Not Reflected In Share Prices While the stock market has had a terrific run over the past five years, the share prices of the oil majors have gone nowhere. Chevron, Royal Dutch Shell, Total, Exxon and ConocoPhillips — all flat over a five year period! The market is certainly not pricing in the big increase in free cash flows on the horizon for these businesses. That provides us with an instance where we don’t need to pick just one stock to take advantage of this opportunity — we can spread our risk across all of the oil majors by owning the entire basket of them. That will not only set us up to profit from the cash flow surge that is coming, but also to receive some very nice dividend yields along the way. Here’s to looking through the windshield, Jody Chudley

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)