Send this article to a friend:

March

13

2023

|

Send this article to a friend: March |

|

Panic in the STREET: One Bank Crashes, A Bigger One RUNS for its life then crashes, and Suddenly it’s Panic on Wall Street!

Just a glance at the top Daily Doom headlines this morning gives you a clear overview of all that transpired in one twenty-four-hour news cycle:

And that was just the beginning! (Note: Readers of The Daily Doom, who get the morning news articles that become seeds for my own articles, may want to read the next section of this article, even though they’ve read a fair part of this morning, just to see who it had to be changed.) Panic sweeps through the marketplace It was not at first the big banks crashing, but smaller banks (Silvergate) with heavy exposure to crypto currencies. That caused some analysts and financial commentators to ask if this is the beginning of “Savings & Loan Crisis 2.0.” Now, with one small bank down and one big one on the way and another much bigger one already down, too (AM revision), a panic has begun to sweep has swept through Wall Street. Out of the blue, serious problems emerged in one of the nation’s top-twenty banks — Silicon Valley Bank, which grew exponentially during the tech craze in stocks. A run on deposits at SVB The all-out crash of SVB right after the failure of a small crypto bank, which already had investors a bit on edge, left global stock markets gasping even when rising unemployment rates today would normally have breathed life into stocks (under the Wonderland bad-news-is-good-news scenario in which stock investors sigh in hope that relief from Fed tightening may be right around the corner if the economy is slowing as the Fed wants). Instead, stocks plummeted yesterday and opened down plunged again globally today — especially bank stocks, even too-big-to-fail bank stocks — as contagion fears build around the ongoing cryptocrisis that began last summer that is refusing to settle down, but especially as it suddenly appears became a fact that Fed interest hikes have reached the point of suffocating speculative tech companies and taking out banks. SVB is a major player in the venture-capital realm where companies with promise but no profit financed their way along, covering their expenses with ultra-cheap credit that is no longer available. These zombies are rapidly depleting the cash “burn” they raised and have stored in banks like SVB, leaving Wall Street to now worry that the run on SVB crash of SVB, as other tech companies try to protect what cash they have left, may be the emergence of something more ominous than was seen at Silvergate. It could be that we have We have hit that point where the Fed has tightened until something big broke. The nearly overnight emergence of a truly major bank that clearly lost its shorts as the tide ran out (its stock down 60% in a day and still falling again today) leaves investors wondering how much more is already breaking beneath the surface in other sizable banks. And the bailout-beggars have already started sounding off on SVB’s behalf (and you can be sure on their own behalf as well). Even Michael Burry (not a bailout dude, but a short-the-duds dude), the eccentric investor featured in the “The Big Short,” warned, “It is possible today we found our Enron.” And, from the time I composed that intro in the early morning, which I had to revise as soon as I published it, the news got worse! Much worse! A marathon run of runs begins The run on SVB started as venture capitalists urged their clients to quickly withdraw their funds in order to save themselves.

Warnings of that kind, which appeared overnight around the world, built on fears that had already been building to a slow simmer on Wall Street, as I had covered yesterday in The Daily Doom. That set the mood for a much broader scare today:

Yes, this is, once again, Fed tightening causing the exact kind of damage I laid out for what is coming (now is HERE); and it comes, inevitably from way too much prior Fed loosening of monetary conditions. This also seriously bad news for other banks that are heavily involved in either the crypto sector or the high-tech sector of the economy. The latter realm contains many of the zombies I warned my Patrons about in many posts early last year and the year before that as the kinds of companies that would be first to fall when the real Everything Bubble Bust got underway. So, this means the Everything Bubble Bust is now fully emerging as the contagion spreads from a few small companies to truly major US banks. That is why in just one day we are already hearing cries for bailouts! Yes, once again, the big money is running to the Fed and Feds for bailouts:

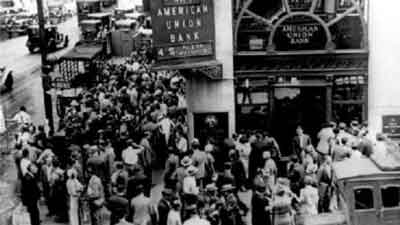

First, the run got real, as in right at the bank’s doors in old-fashion Great-Depression style:

Then regulators shut down the bank to prevent the run from growing:

Well, that escalated quickly! So, yes this is a full-on bank run (revise to crash) at a major US bank, right after Jerome Powell assured all of us at his congressional hearing things looked steady for banks ... as these things always happen. They are black swans in that no one saw which particular bank was going down, while most people did not see anythingcoming at all. They are not black swans in the broader sense that the breakdown of banks under Fed tightening is something I and others have warned about as clearly coming. Just as I just wrote earlier in the week regarding commercial real estate, we have hit that stage where we are suddenly starting to see, as the tide rolls out, what major financial firms are swimming naked. (See, if you missed it, “Real-Estate Bust 2.0: The Commercial Real-Estate Tsunami Has Arrived.”) Not only did the bank get shut down to lock depositors out from making physical withdrawals (and shutdown electronically, of course), but the bank’s stock trading got shut down today, too, after its stock took an additional 47% plunge from the ending point of its massive 60% cliff-dive yesterday! (That is a 79% crash from where it was valued just two days ago!) We’re talking major destruction that almost no one outside the bank saw coming at the start of this week, including particularly the Fed. We never learn That is how these big bust events happen every time! They burst on the scenes so big that we are already hearing the bailout bastards beg for help again (but “only for the sake of others,” of course):

Whether Ackman has any interest in SBV at all, he undoubtedly has interest in other firms that this contagion can spread to or in companies that are dependent on this kind of bank to maintain their funding. That, or he wants government backstops in place for deals he’d love to scarf up. He clearly sees that the trouble here has mushroomed in just twenty-four hours to the point where major intervention by Fed and feds is going to be necessary to stop a rapid cascade:

I’m sure he knows private capital is not going to step in when the stocks are falling 60% one day and then 47% from that point the next day. No one wants to rush into that house of flames without a major Fed backstop like we saw regularly back in the Great Recession — the origin of this blog’s rage:

Yeah, taking advantage of that great fire sale resulted in JPMorgan Chase needing to be bailed out later on. Of course, with its major influence in the Fed, JPM Chase could literally bank on that rescue if it scooped up the bargain. Now, we are hearing the calls that went out after Bear Stearns for bailouts telling us to get ready again.

Of course not, because they saw what happened when the powerful JPM Chase needed a Fed rescue plan right after bringing Bear-Stearns’ cancer into itself. I wrote about how sick all of that was in the following articles that were published by the Hudson Valley Business Journal before I started writing this blog: (They are what eventually got this blog started.)

That’s right, this pattern is SO predictable, I laid it all out way back then and promised it would be coming around in future cycles because the moral hazard created by these bailouts with the constant readiness of the Fed and feds to cower before the toppling of these banks assures the greed of wild speculation will continue, and the rescue plans for the overall economy fuel that rampant speculation. It’s how our politicians always underwrite the greediest most-depraved aspects of our capitalist system (a human problem no system is without). My whole reason for writing everything on this blog is to say, “This is what we keep doing. The longterm results of not doing differently are totally predictable, so we will repeat history.” I’ve said that many times, describing what is happening today.

Those articles I eventually gathered and combined with other articles from the time and new writings in my first ebook, “DOWNTIME: Why We Fail to Recover from Rinse and Repeat Recession Cycles: The same characters who created bailout bonanzas for banksters in the Great Recession are doing it again. Shall we let them?” That tiny book promised we’d do it all again because, as became a mantra in that book, “We never learn!” With that background, let us return to today’s story and the current bailout beggar:

It is the same old garbage all over again, just as I wrote back then we would see happening in each bust cycle to come down the road, in part because all we ever did was make the banks that were too big to fail bigger. We also solved a debt problem by creating massively larger debt at even cheaper rates, which was never sustainable and certain to self-destruct as those rates went away.

What the Feds did to JPM? Are you kidding me? In the last of those articles listed from longago, I wrote about JMP swallowing Bear Stearns as follows:

And congress and the feds in the Bush government wholeheartedly supported all of that! What did the Fed with approval of the feds actually do in the end? It made JPM much bigger than ever before! Sure JPM foundered with indigestion after gluttonously eating such a cancerous beast until the rescue came in. Ackman merely wants to see guarantees again that those who rush in to the fire sale will have the Fed and the government fully behind their guaranteed enrichment. Perhaps, he’d like to snarf up a fire-sale bargain for himself AFTER he’s assured the Fed and Feds have the situation fully backstopped to take all the risk out of it. I’m sure the big boys would love to enjoy another feeding frenzy like we had last time:

Yup. These are the times when fat banksters feed like sharks to get fatter off the failures of their competitors … but they want insurance that they won’t die of colic or indigestion from eating such internally rotting garbage with all of its buried problems as a path to growing as quickly as cancer can spread. And we’ll let them do it. We always do. If you want to see a clear picture of how all of that played out back then and how I laid out years ago how it would certainly happen again, and the how I laid it out in 2020 for what would happen in 2020, which it did, you can read the short ebook that encapsulated the whole escapade for our current times. In the book I also lay out a clear alternate path to a true recovery — a path we’ve never had the wisdom or courage to take because it requires taking the pain up front, instead of pushing it away. You could see this crisis coming from the other side of the world! In the meantime, here we are again as was easily predicted based on the Fed’s chosen path of interventions and baked-in crashes:

Poor wealthy individuals and long unprofitable zombie tech companies whose failure in the event of Fed interest-rate hikes was predicted here for months ago! Poor, poor zombies and their rich investors who can’t see where they will go now without a return to bailouts to stabilize the losses that are resulting from their greedy leveraging and wild speculative risks and all the exuberance they wrongly invested in the stocks of profitless companies … or in any company likely to lose value when the Fed starts tightening the financial system. Poor rich people!

Well, that happened quickly, didn’t it? In less than one week one of the United States’ largest banks crashed all the way into receivership … the very same week, in fact, where Jerome Powell assured congress there was no apparent bank risk on the horizon because banks were well capitalized with strong reserves. Do you suppose they will ask him back to smack him on the head??? How many times are we going to listen to this effluent before we fire the Fed? No chance of contagion, though, right? We’ve been assured of that by Father Fed, too.

Oh, well that sounds a little contagious! Fortunately, we have some familiar heroes watching out for us:

Well, thank the devil for her I guess. Where were her watchful eyes wandering months ago when she was assuring us all was fine? That is how these guys always fail — assuring us all is fine because they are blind. Congress then anoints these failures to high positions like national Treasurer. That’s right: our top watchdog of government treasure is the same person who assured us just before the start of the Fed’s quantitative tightening under her direction in 2017 that QT would go on autopilot and be as boring as watching paint dry. The same people who didn’t see the repo crisis coming, which I came to called The Repocalypse, after saying how much worse it would become than the Fed was letting on in 2019. The same people who have been assuring us all of this year that banks were “fundamentally sound.” Now the 16th-largest bank in the nation has crashed into government receivership in less than a week! Yup, sound! Very sound! And all of a sudden, there are hints of broader contagion even from Gramma Yellen:

Besides being a “no kidding” statement that is dimmer than a seven-watt lightbulb, let me re-quote the important part: “THERE ARE A FEW BANKS THAT I’M MONITORING CAREFULLY.” Just a few! I wonder if some of them are as big as number sixteen. She says it so casually, so as not to trigger larger alarm, just as she casually told us all year that all banks appeared to be on a strong footing. Gee, what will we wake up to on Monday? We all remember how the Fed liked to orchestrated its greatest bailouts in secret with the full help of the Treasury on weekends!

No kidding. In other words, problems like this impact the zombies, which have accounts at other banks, which impacts those banks. So, on it spirals. Thank anyone but God (because why blame God?) we have someone vigilantly asleep at the switch like Yellen! She has so much experience at sleeping through these things. Now, do we have a populace that will finally start yellen, “NO BAILOUTS!” If you want to see how that can work to force the greedy to fully absorb the pain while minimizing collateral damage to all the bystanders, you can read the book where the plan is succinctly laid out … after it fully lays out the predictable problem from the repeated past so you can understand why the alternate solution is necessary: Liked it? Take a second to support David Haggith on Patreon!

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)