Send this article to a friend:

March

06

2023

|

Send this article to a friend: March |

|

The War for the Dollar is Already Over Part I

For nearly the past two years I’ve been a nearly lone voice in the wilderness questioning the financial orthodoxy over the behavior of the Federal Reserve. It started with an innocent, if not openly naïve question back in June of 2021, “Could the Fed actually be getting off the globalist train?” When I asked that question it was just days after musing to my Patrons on the eve of the June 16th, 2021 FOMC meeting that the Fed would have to step in and defend the US dollar. The dollar’s weakness during the Trump presidency couldn’t last forever. Even then I didn’t have a good answer as to how they would do it. I just knew, intuitively, that they had to. Back then there was no indication that the Fed was ready to begin raising rates. But by raising the Reverse Repo payout rate 0.05% above the Fed Funds Rate the Fed started the avalanche of US dollar strength that has persisted through to today. And the pebbles screaming, “Pivot!” have been consistently overrun by the reversal of flow of US dollars from overseas back home, now getting extinguished at an unprecedented rate. It was that extreme response by the market to the RRP rate that led to my asking that question. Nothing more, nothing less. The implications of that question were far reaching. It led to a whole series of questions as to the knock-on effects. I wrote about some of these in the days after the Geneva summit where President “Biden” and Vladimir Putin hashed out a ceasefire over Ukraine. In that article I didn’t get everything right, but the main point, that the Fed was no longer willing to go along with the destruction of the private formation of capital, has more than held true. Here’s the most important point:

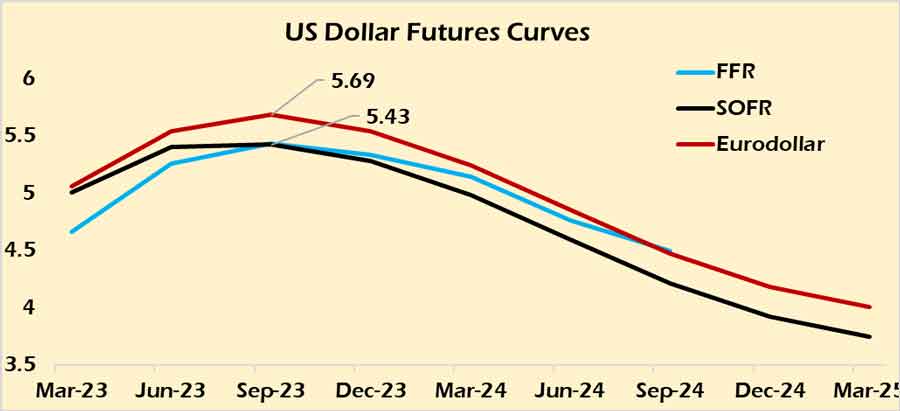

It was the possibility that the Fed, who ultimately answers to US commercial banking interests, is pursuing its own agenda that I explored in a recent podcast with Danielle Dimartino Booth, hoping to get her perspective on this widened lens of Fed policy rather than just focusing on inflation. In my opinion, Danielle more than delivered. One of the biggest complaints about the Fed’s policies since the 2008 financial crisis has been that it has acted as the Central Bank of the World, rather than the Central Bank of the US. What I find hilarious, honestly, if not a little pathetic, is that the moment the Fed starts acting like a domestic central bank, the wailing and gnashing of teeth comes from all corners. I expect that from globalists and vultures who love taking the Fed’s zero-cost dollars and levering them up to feather their own nests to build their own private empires in the shadow banking system. I didn’t expect that from the alternative economics space, however. It’s like the Fed had just become everyone’s punching bag and that was that. Ok, rant off. Back to the avalanche at hand. Think back to 2021, or even the beginning of 2022, and remember that no one could even conceive of where we’d be today — the Fed Funds Rate at 4.75%, likely going to 5% in less than two weeks, and the term structure of dollar futures markets reluctantly admitting to a terminal rate between 5.50% and 5.75%. I argued strenuously that in order for FOMC Chair Jerome Powell to make this new sovereign US monetary policy stick, he would have to ‘pull a Volcker’ and raise rates aggressively. This would expose the lies of the “Biden” administration about deflation and the need for trillions more in COVID-19 relief funds — the Build Back Better bill. It would uncover who on Capitol Hill was aligned with the Fed and the New York Banks it represents, or, at least, who had their backing — Kyrsten Sinema (D-AZ) and Joe Manchin (D_WV) — and who was actively working against them. — Joe Biden, Federal Reserve Vice-Chair Lael Brainard, the Democratic Party and most of the Republican Party and Treasury Secretary Janet Yellen. Even as I was making these arguments I never thought Powell would actually do it. Then he did it. And here we are today (well, March 3rd’s closing).  When I say markets reluctantly acceded to the Fed’s program I mean that just one month ago these curves were all signaling a Fed “Pivot” at 5% and that it would happen in June. Now the Fed Funds Futures is essentially flat at 5.45% until December. But these curves are highlighting for me exactly what I’ve been preaching for the past two years. The Fed, through aggressive rate hikes and fundamental changes to its transmission of monetary policy, has placed the biggest burden on on US dollar markets overseas, not domestically. Moreover, every major shift in policy, the statements coming from Powell, and the upcoming changes to US dollar markets themselves have supported this idea. All of this was taking place against a gradual change in the foundation of US dollar markets phased in over a five-year period; the shift from LIBOR as the debt-indexing rate in US dollars globally to SOFR. As of today there are three major futures markets to coordinate the supply of US dollars through time, the Eurodollar, the Fed Funds, and now SOFR. But all of these ultimately were subservient to LIBOR because that’s where the overnight money markets took their cues directly from. The futures markets reacted to the LIBOR call out. Remember in January 2022, the penultimate phase of SOFR’s replacement for LIBOR took place. That was when all new US debt had to reference SOFR as the baseline rate, rather than LIBOR. LIBOR was ending in June 30th, 2023. Keep that date in mind. Because it looms large over everything currently happening. Go back to what I’ve been saying for over a year, the Fed is not raising rates to combat inflation. The Fed is raising rates to drain offshore dollar markets and force the offshore dollar trade to take its cues from the domestic cost of dollars as priced by SOFR, not LIBOR. If you still haven’t been convinced of this argument, fair cop, but then why is the Eurodollar futures curve, at the first sign of bond markets finally believing the Fed is serious about not “pivoting,” trading significantly above both the Fed Funds and the SOFR futures markets? (see graph of yield curves above). The spread being positive (26 basis points positive!) means the demand for US dollars overseas is far greater than the demand for them domestically. That spread is the pain threshold not for the Fed but for, primarily, the ECB and the Bank of England. As much as we would like to blame the Fed for everything happening, creating scapegoats are simply a coping mechanism for being unable or unwilling to reconcile what is happening versus what we would like to see happen. They are a reflection of our anxiety about that which we can’t control. And you can argue that I’ve done that with my incessant invoking the Davos bogeyman lurking behind the scenes, and, again, fair enough. But that’s why we go deeper and ask the questions necessary to map out where everyone’s incentives are and how they would react to specific pressures changes in policy or personnel. Bye Bye Eurodollars, Hello SOFR Two years ago the idea that SOFR would successfully replace Eurodollars as the global market yield curve for US dollars was laughable. When SOFR was introduced in 2017 it was phased in with a five-year rollout plan, culminating in January 2022’s mandate. SOFR was the indexing rate of the US and that was that. In December of 2021 SOFR futures traded around 290,000 contracts per day. By this report by IFR going from numbers from the CME, volume surged to 964,000 contracts.

That was last year, less than a month before Powell began squeezing the Eurodollar markets to death. Oh, but wait there’s more from Feb 2022:

Still not convinced? Why would you be, a year ago SOFR was doing 37% of the mighty Eurodollar’s business. Then let’s flash forward to February of this year with a press release from the CME itself.

Ooops. If this was a prize fight they would have called it on a technical knockout two rounds ago. Oh, but wait, they already did. You see, this is why I sandbagged you for this entire article. One, because I’m an asshole and two, because so are the guys running the CME. The CME announced back in October that it was suspending trading in its former champion Eurodollar Futures and Options on Futures contracts dated after (wait for it) June 30th, 2023. The last day of trading will be April 14th. For a little more fun you can check out the CME’s daily SOFR Futures report. I think that avalanche is now so loud it could be heard from space. Poor pebbles.  SOFR knocked out the Eurodollar because that was the Fed’s and New York’s ultimate goal; to replace the global rate for dollars with a domestic one where the capital would have to trade here. The globe takes its cues, not from what Europe or Hong Kong wants, but what America needs. This stabilizes our banking system, taking back power the Fed had ceded under Greenspan, Bernanke and Yellen and reminding everyone else just who runs Bartertown. Most importantly, it pulls liquidity from around the world back into US markets, providing a foundation for a future where Davos doesn’t control DC. There are further implications of this but I’ll leave that for Part II. The question I leave you with is the following, “Is there another, bigger avalanche further up the mountain?’ Join my Patreon if you don’t want to be a pebble.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)