Send this article to a friend:

March

12

2020

|

Send this article to a friend: March |

|

Rate Cutters Unanimous Last week the FOMC surprised the markets with a rare inter-meeting rate cut. As the FOMC statement released on the occasion reveals, the decision to cut the federal funds rate by a hefty 50 basis points was unanimous. The much-lamented “zero bound” is coming closer rather quickly. A happy little money tree… from “The Joy of Printing” >>> As Mish notes here, Mr. Powell stated the following in remarks to the press after the announcement:

Wise words, chair-person, wise words. Why cut rates then, if none of these objectives can be achieved? The explanation according to Mr. Powell:

Looking around the inter-tubes, we noticed that this prompted numerous people to wonder at what level of the federal funds rate precisely they would feel the urge to book their next cruise. The stock market at first bounced in typical knee-jerk fashion after the announcement, but then sold off rather significantly. As confidence boosters go, this rate cut appeared to leave a lot to be desired. In fact, one had the impression that it was undermining rather than boosting confidence, by conveying the message that the monetary mandarins are quite worried. Following Market RatesThey probably are quite worried, and there is reason to believe that yet another rate cut will be implemented at the regular FOMC policy meeting this month. Consider the following charts:

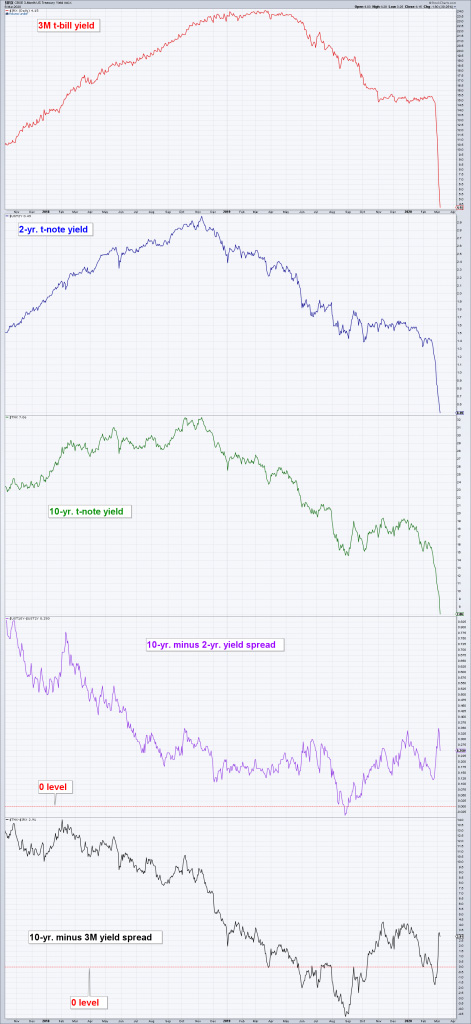

US interest rates and yield curve spreads: 3-month t-bill yield, 2-year t-note yield, 10-year t-note yield as well as the 10 year – 2 year spread and the 10 year – 3 months spread. The decline in yields in the past two weeks is unprecedented; the Fed is simply following the lead of the markets and is actually still lagging substantially behind recent market moves. Note that the spreads between 10-year note yields and shorter term yields have begun to rise after inversions were recorded previously. This is usually a major recession warning. We currently don’t really see any good reason for short term yields to recover, but even if they do bounce a little, the federal funds rate will probably remain too high relative to the rest of the yield curve:

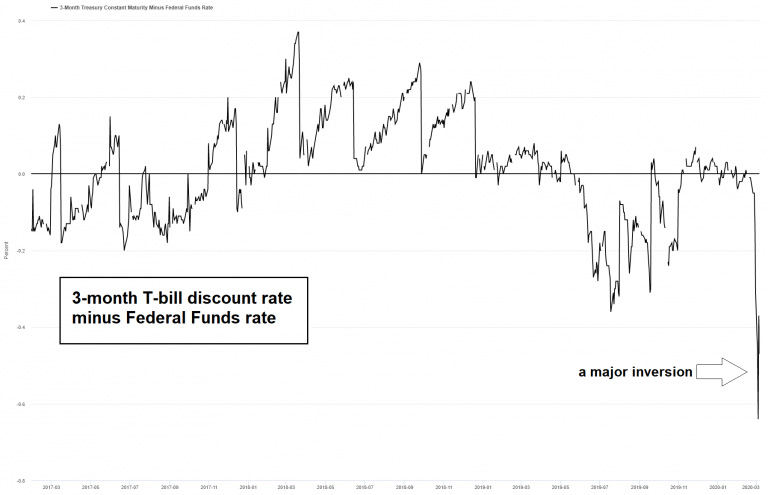

3 month t-bills rate minus the Federal Funds rate – the current steep inversion strongly suggests more rate cuts are on the way. With more rate cuts highly likely, one can begin to speculate when the recent bout of “not-QE” will officially morph into the next round of “QE”:

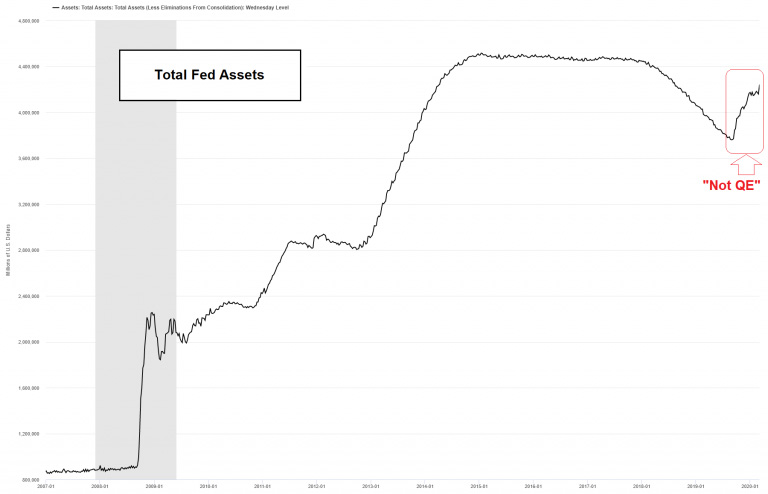

Total assets held by the Federal Reserve system. Under the recent “not QE” debt monetization program, the Fed’s balance sheet is rapidly approaching its former peak. ConclusionMore monetary pumping is on its way, not only in the US but also elsewhere in the world. However, as Mr. Powell correctly noted, this can neither fix supply chain disruptions nor persuade the COVID-19 virus to magically disappear. We suspect that while “not-QE” and whatever asset purchase program follows in its wake will continue to boost money supply growth, the effects will probably be offset by rising demand for money. This is highly likely because the risks from the spreading COVID-19 infection are not really quantifiable at this stage. Both individuals and companies will probably want to increase their cash balances as a result – and this means that the “usual” effects of strong money supply growth on asset prices may not occur this time. If e.g. share buyback programs are curtailed, a significant source of demand for stocks will disappear. In the near term the market may be sufficiently “oversold” to prompt a bounce (even that is actually far from certain), but caution continues to be advisable. There are times when the old adage “don’t fight the Fed” does not work as advertised.

Charts by stockcharts, St. Louis Fed

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)