Send this article to a friend:

March

25

2020

|

Send this article to a friend: March |

|

COVID-19: Market panic and how to navigate through it

Covid-19 First of all, I am not a medical professional or epidemiologist. We have all heard the same stuff from doctors, WHO, and the CDC, I have no knowledge to offer from that standpoint. Many people are taking advice strongly and self-quarantining. A lot of people though think we are making too big a deal of this. There is however, no doubt that the corona virus headlines have been exacerbated by the stock market declines, and likewise, stock market declines have exacerbated the round-the-clock, fear driven, corona virus headlines. Please note, this is not my opinion, it's just whats happening. Don't scream at me that I am on the side of the people who say we are overreacting, I am not saying that at all. The simple fact of the matter is that the reactions by people, politicians and the news are being fueled by the reactions by financial markets and vice versa. This would be a very different scenario if the stock market wasn't down over 30% in 3 weeks and we weren't staring down the barrel of a recession. It is also important to note, that the corona virus is NOT the reason why the market is declining in record amounts and at record speeds. The reason for these declines is massive over-leverage, massive debt and a culture of reckless investments and moral hazard that has been created by government bailouts, fed monetary policy and debt monetization, and an utter lack of consequences for people and organizations who have failed at business, taken advantage of customers and taxpayers, and in some instances, literally broken the law. The corona virus has simply been the catalyst; the sound of the music stopping in a multi-trillion dollar game of musical chairs. Let's rewind back to the last financial crisis to figure out how we got here and what will likely happen next. 2008 Financial Crisis The biggest financial crisis since the Great Depression was caused by a housing market bubble. Everyone seems to know and understand that much. But what brought down the financial system was over leverage, bad risk management, and poor planning. Banks like Lehman and Goldman were holding massive amounts of MBSs (Mortgage backed securities) These got significantly impacted by people suddenly unable to pay their mortgages, mortgages that in a lot of cases, they never should have had, but with loose credit standards and subprime rates they were somehow able to get away with it. (Lets also not forget about the blatant lying and fraud by financial institutions involving predatory mortgage loans, who were later found responsible, and somehow skated off with only a fine. No jail time for executives and the businesses were not banned from the industries they abused. What a country!) Now, these organizations spend lots of money hiring people who should probably be working at NASA to build financial risk models to calculate what defaults on MBS, and every other asset they own, would look like to their overall assets and operations. They then analyze these scenarios, and quite literally, leverage as much as they can to profit as much as they can without risking an imbalance in something that could trigger a serious problem for the business. And it worked for many years, until it didn't. The number one reason so many models failed resulting in so much losses and the eventual need of the government using taxpayer money to bail them out, was simply that most models never took into account a situation where everyone would default at once. It just statistically was not possible, so it was not accounted for. And that of course, is exactly what happened. So we bailed out the banks, we bailed out the people who had counter-party risk with these institutions, like AIG. We didn't bail out the auto companies because of a decline in the auto industry, we bailed out the auto industry because their financing departments were bigger sources of revenue then their business of actually manufacturing cars. Consequently, they suffered the same defaults on their loans. But bailouts weren't enough. With these massive losses, the fear was that credit would dry up, causing a significant decline in GDP and risking a massive rise in unemployment, akin to the Great Depression. So the Federal Reserve took "bold and unprecedented measures" to ensure this wouldn't happen. They cut interest rates to zero to incentivize borrowing. Unfortunately, there are 2 sides to that coin, and incredibly low interest rates do not really incentivize lending. They began a round of Quantitative Easing, which is essentially printing money out of thin air to buy government treasuries and MBS. The first round started at about $1.4 trillion worth. In November of 2010, they announced they would do an additional $600 billion. Then in September of 2012 they announced an open ended monthly purchase of $85 billion in treasuries and MBS that didn't end until October 2014. As treasuries reached maturity, they announced another measure, "Operation Twist" in which they would reinvest the money from shorter term expiring treasuries into longer duration bonds in an attempt to push down long term interest rates. In total, they accumulated $4.5 trillion in asset purchases, all in the plight of pushing down interest rates to incetivize borrowers to spend money into the economy. Today's Financial Crisis I saw this coming. No, I didn't predict an infectious virus would come out of China and effectively shut down the world economy and lead to the fastest stock market decline in US history. No one did. And that's half the problem, but we'll get back to that later. What I did see, very blatantly and in an extreme fashion weeks before this collapse, was incredible recklessness in investing. Tesla stock shot from 300 to 900 in weeks. Virgin Galactic soon followed in a similar parabolic fashion. Institutions were massively over-leveraged, betting heavily on foolish things. Hedge funds had been shorting the VIX (volatility index) in record numbers as it reached all time lows. As long as the market was melting higher, it worked. The Fed had dropped interest rates earlier in 2019 from 2.5% to 1.75%, and in November announced overnight Repo operations to provide the financial system with liquidity after overnight swap rates neared 10%. (It's worth noting, right around the time they did that was when things began going a little crazy with stocks like Tesla and Virgin Galactic. It's also right when the market finally rocketed higher from the 2850 area the S&P had been held back by for the previous 2 years. I'll leave it up to you guys to figure out if the liquidity pump at the same time frame had any correlation with rocketing stock prices immediately after. Sure to be a real head scratcher.) Some people I have tremendous respect for have hypothesized that a substantial institution, like a hedge fund, might have "Blown up", or in short, went over leveraged into a bad bet and suffered massive losses that could have impacted other financial institutions they did business with, and their obligations to them. (Sound familiar?) If this is what happened, we likely wont find out the details for a few more months anyway, but I think it is a very real possibility and explains the Fed's sudden reaction as well as the liquidity crisis we are facing now.And then in comes the Corona Virus. Again, this is not the cause of the markets collapse. It merely was the first domino to fall, leading to a modest but swift decline in the market and a spike higher in volatility. But when the world is overleveraged, that's all you need. A few big players get squeezed and start losing money, now they need to raise cash to cover their losses and impending margin calls, so they start liquidating, triggering more losses for other overleveraged funds who now also have to liquidate. In a world where 90% of all trades on the NYSE are computer algorithms, the snowball effect of this begins happening in minutes. In a very short period of time virtually every financial institution, business, and individual has reassessed their financial situation and has found they are dangerously low on cash. The important thing to remember in a liquidity crisis is this: Logic has no use here. We have a saying on Wall Street, "If you can't sell what you want, you sell whatever you can." When margin calls come and liquidity has to be raised, you very rarely have the luxury of choosing whether to sell bonds, gold, your Apple stock, Walmart, or Tesla. You have to sell to meet liquidity requirements, often by the end of the day. It doesn't matter, you just sell. Doesn't matter if the market is down 2,000 and all of your stocks are selling for way less then you would ever dream of selling them for, you MUST sell. If you are fortunate enough to choose, people typically choose like this: First they sell their dogs. Stocks that have gone nowhere, Macy's, Ford etc. Then when you still need to raise cash, you sell your hedges that are at least making you a profit as things collapse so that you can lock in those gains. This is the stuff like gold, bonds and the VIX, which is why gold has dropped significantly and interest rates have spiked higher in the last few days. (It's also the same reason why gold dropped 30% during the financial crisis after hitting $1000/oz on the impending economic fears. People needed cash, so they sold everything) The last and final thing people will sell is Apple. Not just Apple, the usual suspects, Amazon, Google, Facebook, etc. All of the high flying tech names that have made people a fortune over the last decade. They'll liquidate everything but Apple because they sold Apple once, and it went skyrocketing, so they've learned to hold it forever because it makes them a fortune. When they have no choice, they'll sell Apple too, at prices they never imagined. In addition to the liquidity crisis we have a very real economic problem with this pandemic. The month of March is a total loss. One third of the first quarter will have near zero economic activity. With a few days left till the end of the month and no progress in sight yet, it will undoubtedly be a major drag on 2nd quarter GDP as well. Currently by the Fed's own estimates, 1st quarter will be significantly less then expected, and 2nd quarter will report -2% growth. They project by 3rd quarter we will be at +0.1% growth, which is as good as flat, and could very easily be negative. And that right there, 2 quarters in a row of declining GDP is your dictionary definition of recession. (And I personally think it will be a miracle if we report positive on Q1) Nobody could have predicted this. But they should have. Just like how in 2008, nobody factored into their models that everyone would default at once, they never factored in a freak pandemic that put the world at a standstill. It is not that businesses need to factor once in a century type situations into business models, but they do need to take some prudent measures to ensure that "outlaying" events from their statistical models don't blow up their companies and create financial contagion around the world. This could be avoided by not over-leveraging to begin with, but after what 2008 proved, why wouldn't you? It's zero risk.

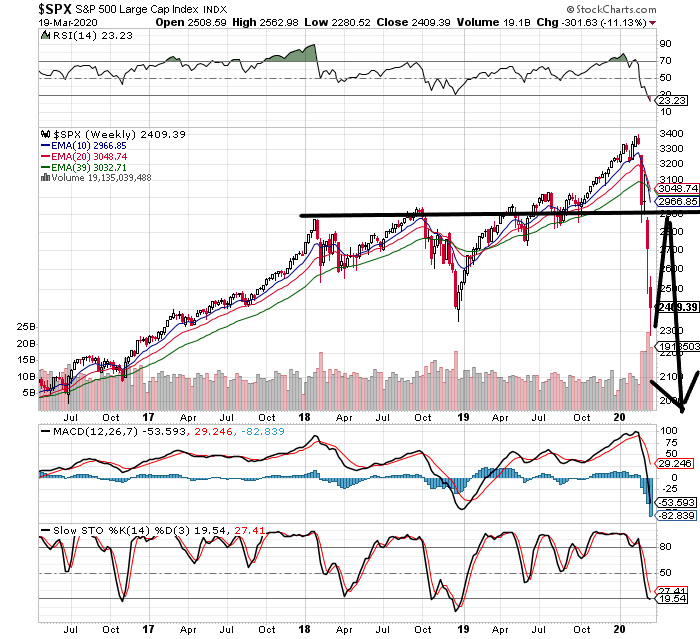

Fallout and Response We went from "debt is good at these rates" to the kiss of death in remarkable time. The institutions that are collapsing are the ones riddled with debt. Fracking operations have been financed in the hundreds of billions by financial institutions to jump on the "Fracking/American energy independence" boom. Problem is they are on average only profitable when oil is above $60/barrel. So now these operations have about $5 billion in assets for their operations, $20 billion in debt and there is no way their operation can make a profit at these prices, so even after liquidating everything, there's someone holding a $15 billion default. Of course right now were looking at the problems with the airlines and Boeing, which has had its own problems with the 737 Max long before this started, but the debt is everywhere, and you can find it by simply scanning which stocks are down significantly more then the overall market indices. Boeing is of interesting note. From 2013 to 2019 they repurchased $43 billion of their own stock. From 2018-19, they purchased over $11 billion in their own stock at a time when their stock was ranging between $300 and $450, likely averaging close to $375 for the $11 billion repurchased. At today's closing price of 97, Boeing has lost nearly 75% on the $11 billion they spent from 2018-2019 and are down overall on the ENTIRE $43 billion of repurchased stock over the last 7 years. (They began their repurchases north of $100 a share). I never understood why investors view stock buybacks so favorably, its essentially like management admitting defeat. They cannot make money at their business by expanding it, so they reduce the amount of pieces their earnings are divided into. Historically, they almost always buy back stock at highs and have no cash at the lows to make any smart investments. A few days ago, Jim Cramer said that Boeing "must be bailed out". Watch how much they end up needing in bailout money, it'll probably be close to 43 billion. But the bailouts will happen. Trump has already said they will protect the airlines. They will bailout the indebted industries in need of rescue directly, or they will be forced to bailout the financial institutions holding the debt that will inevitably default. All debts get paid, either by the borrower or by the lender, and as we are quickly growing accustom to seeing, sometimes the tax payer and sometimes the Fed. But the bailouts will happen again. Because of the same problem; debt and over-leverage, again. And the Fed has already dropped interest rates to 0, again. And has announced a 700 billion dollar round of QE, buying treasuries and MBS, again. They will likely need to increase this amount drastically, again, and increase the duration of the purchases, again until we're doing literally every aspect of this process all over again for the next 7 years before we can see interest rates rise to 1%, only to have them chased down again while we inevitably deal with this exact problem once more, 10 years down the road from now. Is there a better way? Should we ban companies who receive bailouts from doing stock buybacks? Should we cap executive compensation? Should we allow Boeing and the airlines to go under, and instead of bailout money spend significantly less in incentives for others to purchase their operations in bankruptcy where they can actually run the company better and more prudently? Is it any wonder why American car companies can't innovate and Elon Musk is eating their lunch? Why GM's best offer of an electric vehicle, the Chevy Volt was so dismal that it was discontinued a few years later? Maybe it's because we've been bailing them out since the 70s and rewarding management's failure and lack of good ideas with the ability to keep operating in such a way. Quite simply, it doesn't matter. We can philosophize on what we would LIKE to see happen all day long, but what we need to do is figure out what is most LIKELY to happen. When we can figure out that, we can come up with a clearer map of what is ahead of us and how we need to respond. And the answer to that is bailouts, both fiscally from congress, and monetarily from the Fed. Markets Without a doubt, what everyone is focused on is stocks. But all markets are interconnected. You will be hard pressed to find much love for gold when everyone is piling into stocks. Capital flows need to shift into another direction, and for so long, it has been stocks and only stocks. Now it is cash. The S&P has gotten obliterated in less then a month, losing over a 1000 points from 3400 to just under 2300. This is massive. I know many people who were waiting for a strong rally when the market was down 15% that have given up now that we are down 30%. Sentiment is extremely negative in all areas. I personally, have never seen anything like this, even in the financial crisis. Markets don't move in straight lines up or down so it does seem likely that a very strong rally is coming soon. I must make this clear, in no way does that mean you should buy hoping for one. We are still in a liquidity crisis and moves the market will make will defy all logic. You will literally go broke wondering why a "good" stock is collapsing so much. But it seems to me, a logical scenario now is the good old "two steps forward, one step back", or as others call it, a 50% retracement. The S&P has lost about 1100 points. A logical move now, in a bear market, would be a massive 550 or so point rally that makes everyone breathe a little easier. That would be about a 5,000 point rally for the Dow. Interestingly, if you look at where a 550 point rally would take us, it would be right around 2800-2900, an area where the S&P had been topping for the last 2 years, until the Fed turned up the gas by lowering rates and pumping Repo, causing the blow-off, break-out we had in November that is now collapsing. Ultimately though, I think we are only about half done with this. There is a lot that needs to be unwound, but after losing 30% in 3 weeks, I think after a fake-out, strong rally that eases everyone's fears, we will ultimately see the markets continue to slide until they have reached 50-60% down from their peaks. Historically, such declines have taken about 18 months from the time we hit the top till the time we hit the bottom, but given the severity of all of this, and the dramatically faster speed that our algorithm run market is falling by, I believe we will plunge and bottom in far less time, likely seeing a low of 1700-1500 on the S&P by the end of the year.

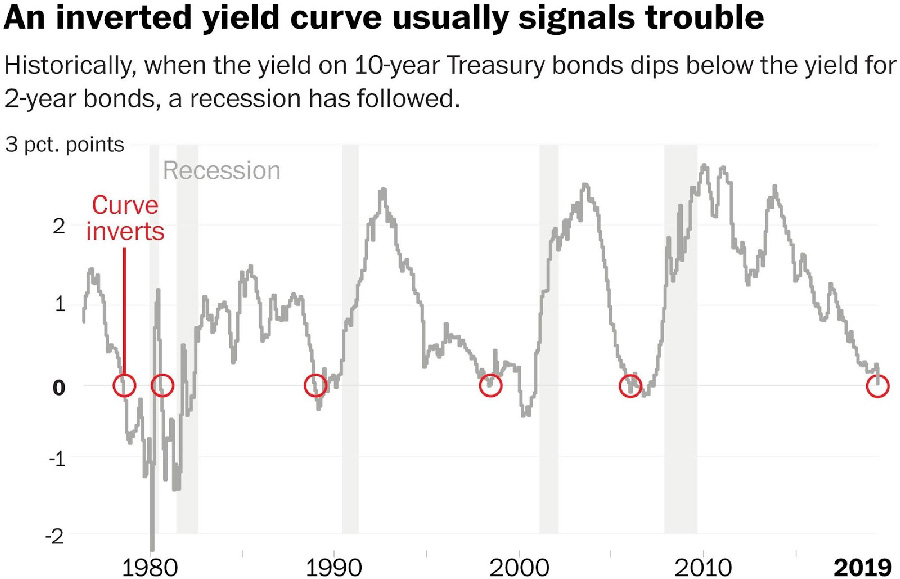

Bonds were the first harbinger of doom here, with the yield curve inverting over a year ago. As the panic ensued, yields collapsed with the 10 year treasury hitting a low of 0.3%. Immediately there was a surge of Google searches for "Mortgage Rates" by people hoping to refinance at half a percent, only to find that the 15 year fixed is still holding at 3%. As the market dropped, bonds surged. When the market hit 10% down, they surged. When it hit 15%, they went up dramatically, when the market hit 20+% down from the high, they collapsed. This is the 2nd step I spoke of earlier, where people sell even their hedges to raise capital. Today, 10 yr rates were back up to 1.1%, nearly where they started off at before the crash. The trajectory for interest rates should be clear. We are at zero now. We have been at zero now for 7 of the last 10 years. We will likely stay here another 5 years or more. Around the world, the Bank of Japan is monetizing everything, so is the ECB in Europe. Both are seeing negative interest rates on their bonds. I can assure you though, no one there is getting paid to take out a mortgage. The real world is operating outside of this fictional creation in bonds that central banks around the world have created. It is only a matter of time until we join them. Trump has advocated this. Apparently no one has informed him that the only interested party in paying for the government to borrow money from them is the Fed, which is essentially, printing the money to cover debts (and then some, cause at negative rates the lender pays the borrower to take it) so we never have to live within our means again. Isn't it amazing, that throughout all of recorded history, we are lucky enough to be living in a time where economists and financial wizards first thought of the idea that you could borrow money and get paid by the lender to do it, and nothing bad will ever come of this? We have truly reached financial enlightenment.

It's remarkable how much the gold market now has been acting like the gold market of 2006-2009. About 18 months ago, gold was 1200/oz stuck in a range for nearly 6 years. Then all of a sudden, gold started skyrocketing, breaking above the 1375 area it had been held below for half a decade. But why? No one could figure it out. There is no panic, no catastrophe, market was going up. But then it happened, and all at once everyone understood why. Gold was $400 an ounce in 2004. It started climbing slowly for the next few years till it was $700/oz. Nobody knew why. Bob Pisani from CNBC reported on the dramatic rise in gold months before the financial collapse, laughing at it's seemingly ridiculous move. When the market started crashing and the financial crisis was looming, it spiked up nearly 50% to $1000. And then the liquidity crisis hit and it plunged back to $700. Gold today went up 40% from its low 18 months ago and has now started plunging. Again, back to step 2, where you sell your hedges. This will likely continue, and again, don't think logically. These markets will be very irrational. 1350 would be a LOGICAL place for gold to pullback to as a crisis looms but because it's logical, it might be far worse. Anywhere from 1350 to 1200 is an area gold can pull back to, so don't think this is a safe haven in these times, because you will get slaughtered. Coming out of this, with debt, deficits, printed money by the trillions, zero or negative interest rates, gold will clearly be a winner. But we could have a lot of loss between then and now. It will be vital to own positions in gold in the future and some select gold mining, but preferably royalty companies. Take advantage of massive swings lower in gold and gold stocks to buy VERY small amounts of the high quality names as they are dropping. What to doIf your sitting here watching this, and you have money wrapped up in the market, do not count on a rally to sell what you need to. Many have already thought the same, and we kept plunging. By now if we did have a rally, we would likely top out lower then where many thought things were a good buy at. If you're having trouble sleeping, if you are too exposed to the market with no cash on the sidelines, if you don't have an emergency fund, of at least a few thousand dollars to get you through in a time where economic activity is declining, there is a global pandemic that could have things on standby for quite some time, and there is serious risk of unemployment skyrocketing in the near future, then that needs to be your only priority. Have the liquidity to get you through for a while if things get bad. Don't make the mistakes so many "genius" CEOs made.If you are sitting here with cash available, then you are the envy of many. The same rule applies though, if you have 10,000 in cash, and need 15,000 in case of an emergency, then sell what you need to. If you are liquid and trying to figure out what to buy and when, the most important thing to do first is have a plan. I have a plan. I came up with it in case of a situation like this. It's what I'm going to buy, how much of it, and what my expected cost is. I have analyzed what the balance of my portfolio will look like doing this. It's important to not find yourself 80% invested in oil or any other one asset. You must have a balance, you must have hedges. Now granted, my plan is very different looking now, as these events are happening then it was when I created it. There are some stocks I was interested in that I will not touch now because the panic is too great and their debt is too large and that is a massive liability right now. There are some stocks where my expected price targets are now far off, and I have to adjust my intended share purchases to match the portfolio balance I am looking for. But the point is the structure of it is there and I can edit it in an Excel spreadsheet with new information on the fly and make automatic calculations. Now I can approach this from a calm, strategic state instead of in a panic, and that gives me a tremendous advantage. Bailouts will occur, for now its too early to tell how cheap is cheap, so don't try to bottom fish on too many individual names. Lack of debt is the key thing here. Those are the quality names you should be looking for, but you should focus your attention on investing straight into the S&P index fund. I say this for a number of reasons. The stock market index has never been worth 0. It has also rarely declined by more then 50%. The reason is that if a particular component is going bankrupt or severely under-performing, they will simply take it out of the index and add another, like they did with Citigroup in 2008, replacing it with Traveler's. Also, over 100 years the market has averaged a 10% gain annually. If you wanna try and beat the market, maybe you can for a year or two, maybe you'll get a few years of 12% gains, but you will probably under-perform. And even if you don't the extra bit you make won't be worth the effort most people will spend on researching and studying the individual investment. Take the cash you have to spend on stocks and start putting 10-15% of that cash into the S&P now while its down 30%. When it goes down another 10%, put another 10-15% of your money into it. Keep going as long as it goes down. Expect a 50% decline. You have to think of this like a business, and as most business owners will tell you, it's expected that you may not make a profit for about 2 years. Treat your investments for your future and retirement like this. In the long run, you will average 10% a year. The first few years out of a recession it will likely be much more then 10%, then it will pare off. At 10% it means your money doubles in 7 years, then again in 7 more. In 21 years, $50,000 invested in the market today would be worth $400,000. (And much more if you continue to add money over those 21 years.) You should have hedges as well, and for that I recommend gold. Bonds offer very little incentive to own them, other then the fact that you can likely always find a buyer for them in the Fed when you want to sell, but it simply isn't prudent to buy bonds at less then 1% yield even if you are expecting negative interest rates in the future. I hesitate to recommend gold itself as a metal because it is still relatively high right now. Silver by comparison is at a 10 year low, but there is a reason for that. Gold is like the high quality stocks, silver is like Macy's. The world views silver as an industrial metal. You can think all day long that it is a monetary metal like gold, but the rest of the world disagrees with you, so if your buying silver for that purpose, your goal is to convince the rest of the world they are wrong and you are the one who is right. (Good luck). I like silver for a number of reasons, and you can make a great argument for investing in silver while leaving out the conspiracy theories of central bank price manipulation or an end of the world dollar collapse that forces us back onto a gold standard while watching silver prices climb to $500/oz. That's just ridiculous. I won't rule it out as a possibility, but if that's your "investment" strategy I would advise you to take your money to 7-11 and buy a Powerball ticket. The 300,000,000 to 1 odds are more in your favor there. Invest in silver if you have a strong stomach and the cash to do so. DO NOT overweight yourself there. The better investment is silver mining companies, which at these prices are at best mining at break even or losing money to do it. There are 2 possible outcomes: Silver mines all go bankrupt and silver supply drops to 0, or the price of silver goes higher. In reality there is one outcome: Some silver miners will go bankrupt dropping the supply of silver on the market, THEN silver will go up. Be careful to avoid the high-cost, high debt miners. Unfortunately, there are a lot of them, so I would be very selective with what I buy and do so in VERY small amounts. First Majestic (AG) has been a favorite of mine for a while. At $6/share, it could very well drop by 50%, as right now they are losing money on their costs of mining which currently sits at about $14/oz. But since 2010, they're production has increased by about 200%, from 10 million ozs a year to about 30 million. That is a lot of leverage on the price of silver. Here is why you buy miners versus metals: Lets say silver stabilizes at about $13/oz and First Majestic reduces their cost to be around 13 as well. They are essentially making no money. A move higher in silver by $1 represents about a 7.5% increase in value of the metal, but the miner goes from $0 in profit, to now making $1 on 30 million ozs. If silver increases another dollar to $15/oz from $13, you have made about a 15% profit. But a silver miner like First Majestic's profit margin just went from $1 an oz, to $2 an oz, a 100% increase. In general, what do you think a stock is going to do when their proifits double? This is why mining companies swing up 30-50% when the metals go up 10-15%. There are very few others in the silver sector that I think are "safe" at this stage, other then First Majestic and Wheaton Precious Metals (WPM). WPM is a streaming company, they buy silver and other metals mined from Gold and other miners that they do not want. They have contracts to buy at specific prices, so if costs go up, it effects the miner, not WPM. I should note though, that with oil under $30, costs for miners is actually at a significant advantage right now. As for gold you could by the GLD, but I advise against that for the same reasons as not buying silver directly. It also has not backed off its highs too much so the value there is less compelling. (Also when you look at the Silver to Gold ratio, which is now over 100, it makes Gold look like less of a compelling investment then miners or silver.) You could also buy the GDX, but mining company problems have riddled all gold miners, and can be easily seen buy looking at a long term chart of miners vs the metal, or vs royalty companies. Not to mention that the business of gold mining in general is a business where a million things could go wrong at any time and often do, and when they do, it is very expensive. At this stage, the safest gold investments to build a hedge in your portfolio is the Royalty companies, which are Royal Gold (RGLD) and Franco-Nevada (FNV). If you want to nibble at a little more risk and buy a growing royalty company, Sandstorm Gold (SAND) looks compelling if you can get it under $5/share. Right now, I have been actively adding to my positions in Royal Gold and adding a small amount to my Sandstorm position. I am not very interested in Franco-Nevada at these levels though, I personally do not see where the value is there vs Royal Gold, and it has not fallen much from it's high leaving it hard to make a compelling case for. In the gold mining sector, the only stock you should consider buying is Newmont Mining (NEM). They are the biggest miner out there, they are the only gold company on the S&P 500, their purchase of rival Goldcorp has seen their production and earnings increase greatly and costs decline, all while they have risen their dividend and seen a nice uptick in the stock price on this rally in gold. But beware, all miners will face problems the Royalty companies do not have.

ConclusionMoney will be printed, bailouts will occur, stocks will drop until they are ready not to and the same with most asset classes. High Quality is the name of the game across the board. Riding out this decline and buying into it to plan for your financial future will not be easy. You will see massive drops that will shock you. You will lose money likely for years before turning a profit. Do NOT get emotional. Have a plan. Don't invest when you have no savings to live off of. Buy into the indexes as they decline as opposed to picking winners and losers. I have seen so many people miss out on so much money thinking they can beat the market and they never do. Some of the losers will be obvious, some will shock you. I can almost guarantee you there is a very big company out there who has been doing something shady, cooking their books, etc, that will have massive problems that will come out now during the crunch and it will shock everybody. There WILL be bankruptcies. It is more likely you will buy a company waiting for a bounce and lose everything then see the quick 100% move higher you were hoping for. Wait till we see some more of the fall out from this and the damage done to the economy and balance sheets before you gamble like that. And realize it's just that, gambling. If you wouldn't bring $5000 to the casino for a weekend of fun, fully expecting to lose it all in the name of entertainment, then do not put $5000 into a $3 stock that is 85% down in a month. We are truly living through historic times right now. We will look back at this event for decades to come. Do not take unnecessary risks financially or otherwise right now. Be calm and deliberate in everything you do and you will have a significant advantage versus the majority. Good luck out there. Jonathan M Mergott

alchemyfinancials.blogspot.com

|

Send this article to a friend:

|

|

|

I haven't written any market updates in some time, and was quite surprised to be receiving requests for one. I am going to attempt to go over as much as possible without devolving into a rant. There is so much happening to analyze and consider, everything from the markets, to politics and of course the corona virus pandemic, and every bit of it is interconnected and affecting the outcomes of everything else. I am going to break this into individual sections analyzing the important issues, markets, and ending with a feasible investment and savings plan for people to follow as we navigate through some of the most volatile markets in this country's (and the world's) history.

I haven't written any market updates in some time, and was quite surprised to be receiving requests for one. I am going to attempt to go over as much as possible without devolving into a rant. There is so much happening to analyze and consider, everything from the markets, to politics and of course the corona virus pandemic, and every bit of it is interconnected and affecting the outcomes of everything else. I am going to break this into individual sections analyzing the important issues, markets, and ending with a feasible investment and savings plan for people to follow as we navigate through some of the most volatile markets in this country's (and the world's) history.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)