Send this article to a friend:

March

17

2020

|

Send this article to a friend: March |

|

Zoltan Stares Into The Abyss: Here Is What The Fed Must Do Right Now To Avoid Global Devastation

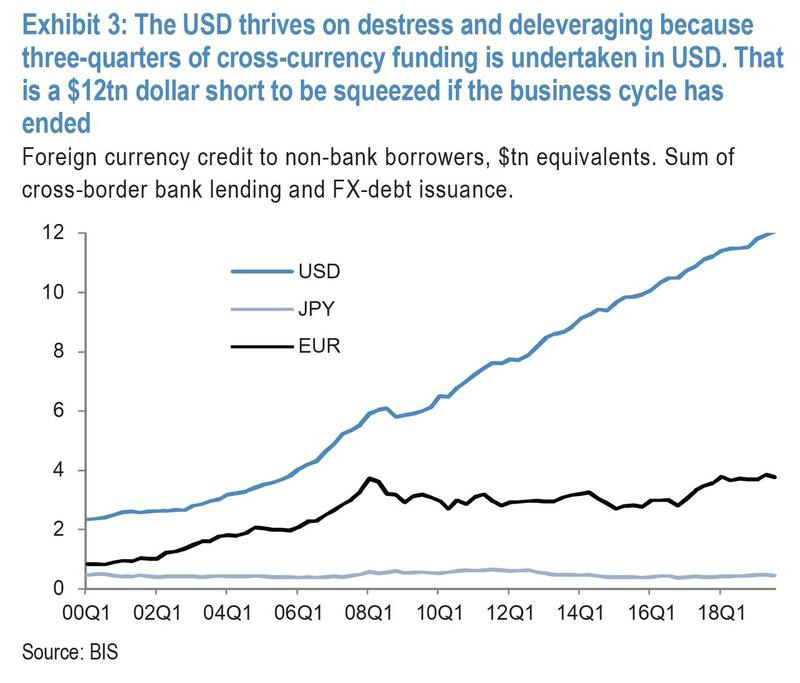

And even though the Fed belatedly followed through with all of Pozsar's March 3 policy recommendations, going so far as throwing a commercial paper bailout facility which was also recommended by BofA's Marc Cabana (another former NY Fed staffer), the market remains unconvinced that any of this is enough, especially with JPMorgan warning that the world is facing an unprecedented dollar margin call, as a result of the $12 trillion synthetic dollar short, some 60% of US GDP.

Faced with this unprecedented dollar shortage, the Fed has so far failed to assure the world it can provide all the funding needed. Furthermore, as we said yesterday, in some ways we sympathize with the Fed, as every day something new breaks among this record funding strain:

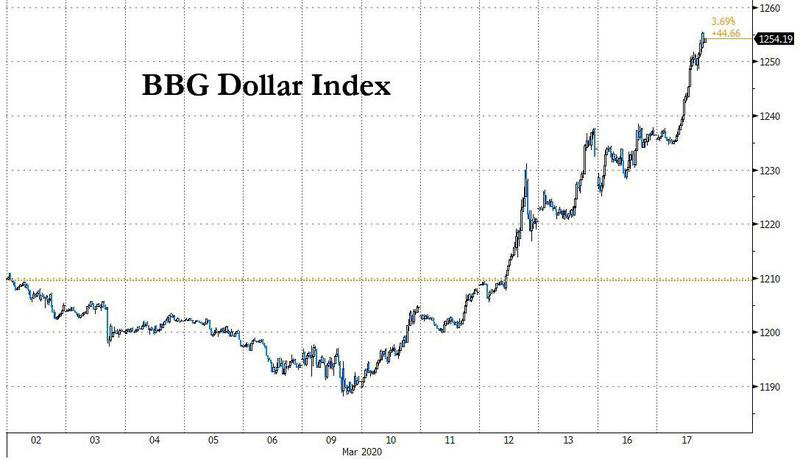

As we further said, "what the Fed needs is the monetary equivalent of Dr. House: someone who can diagnose what is actually wrong with the monetary plumbing, instead of using the same old shotgun approach of shoveling trillions in blunt liquidity into the market, which clearly is not working anymore." Alas, that is not a credible option, meanwhile the Fed’s liquidity injections are failing with the BBG dollar index - the simplest proxy of dollar demand alongside FRA/OIS and FX basis swaps - continuing to surge as various actors rush to procure what, with all due respect to Ray Dalio, is the opposite of trash.

Confirming our take that everything the Fed does, including this morning's Commercial Paper facility restart, is either insufficient or targeting the wrote underlying cause (today even BofA's Marc Cabana who pushed for the CPFF slammed it, saying "this facility does nothing to assist the money funds trying to raise cash and address outflows"), is none other than Zoltan Pozsar who in his latest note published this morning, writes that "all segments of funding markets – secured, unsecured and FX swaps – continue to show growing signs of stress", prompting him to conclude that "the Fed may have to do more still." Scratch "may", and replace with "will", unless Powell wants to watch the dollar short squeeze go all "Volkswagen" on him. So what can the Fed do? Well, according to Zoltan, the time for half-measures is over (incidentally, he too panned the Fed's CFPP writing that "the Fed needs to become a buyer of CDs and CP, but not through the CPFF"), and instead the printer of the world's reserve currency has to become the bank of last resort not only for US institutions, where access should be expanded to non-banks, but also banker to the entire world in the form of unlimited, 24/7 swap lines open with every central bank, not just the G7. Below we present a summary of his must read "Fed must act or else" note:

Summarizing the above is simple: Pozsar is basically recapping what we said in "The World Is Hit With A $12 Trillion Dollar Margin Call", and explains that to fix this potentially catastrophic margin call, the Fed must grant access to virtually every global entity in need of dollars, including those shadow banks which over the past decade scramble to lever themselves to the gills, fully aware that when the day came, the Fed would bail them out. That day has arrived, and it Pozsar's proposal is accepted - and in the past everything he has suggested was promptly pursued by the US central bank - it means that the Fed is about to bail out the world. The repo export than notes that he is most concerned about four key areas which the Fed has so far failed to address:

Going down the list, Pozsar first focuses on the initial shock to the CD and CP markets which he notes came from the equity market collapse and the flows it triggered whereby cash started to flood back from securities lenders’ cash collateral reinvestment accounts to short sellers’ accounts. Given that secured lenders invest cash in the CD and CP markets and short sellers invest mostly in Treasury bills, these flows turned sec-lenders into net sellers of CD and CP, precisely when issuance from corporations and banks is picking up. Outflows from prime money funds have been small to date, but given ongoing stresses in funding markets and heightened risk aversion, prime funds could see more outflows this week as investors take refuge in the safety of government money funds. Such a rotation would further hurt demand for CD and CP this week and will continue to pressure funding spreads including U.S. dollar Libor-OIS. This is notable because it explains why Pozsar does not think that the right solution now is to reactivate the CPFF, as the Fed just did:

And since the Fed is now going, all in, Pozsar says that "this template could then be extended to corporate bond purchases by adding more buffer and as President Dudley would say “going out the curve and down the credit spectrum”. And why stop there, after corporate bonds the Fed can also buy stocks, and oil, and baseball cards, and why not fresh air... But not gold, never gold, at least not until the Fed is ready to fully devalue the dollar against the precious metal, which is also coming in the near future. But we digress... Second, Pozsar is concerned that the Fed's FX swap lines are now active "but it feels like the operational aspects of it need to be fine-tuned. Currently dollars are being offered weekly, but the FX swap market trades like they should be offered daily, and not only at weekly and three three-month maturities but at ultra-short tenors as well, similar to how the Fed lends in the repo market." Third, the swap lines (which we first profiled in late 2009) are open only for banks which is a legacy "fault line in the system." The swap lines were originally designed to help the funding needs of banks during 2008; they work by the Fed lending dollars to other central banks which then lend it to banks. But since the financial crisis, non-banks eclipsed banks as the biggest borrowers in the FX swap market: a hallmark theme of the post-QE global financial order has been the secular growth of FX hedged fixed income and credit portfolios at non-bank institutions like life insurers and asset managers – the new shadow banking system epitomized by money market funding (FX swaps) of capital market lending (Treasuries and credit). According to Pozsar, unless these non-bank entities get access to dollar auctions – from local central banks – FX swap spreads may remain wide if banks won’t serve as matched-book intermediaries; in other words, yet another half-baked liquidity bailout which will not reach the target audience. Additionally, there is a growing risk that such intermediation will fracture as the assets that FX swaps fund include not only Treasuries but credit and CLOs too. Credit quality is fast deteriorating across various sectors and that makes it riskier for dealers to fund some life insurers through FX swaps, just like it became riskier to fund some insurers during the 2008 crisis. As Pozsar puts it, "over the past five years balance sheet and the availability of reserves were the main drivers of spreads in the FX swap market. It’s time to think about credit risk creeping in to funding markets through the asset side of some portfolios funded through FX swaps." To this we will also note that counterparty risk - especially when a certain massive European bank is involved - is also starting to be a factor when making funding calculations... just like 2008. Fourth, and final, the repo expert believes that the geographic reach of the swap lines is too narrow. The Fed has swap lines only with the BoC, the BoE, the BoJ, the ECB and the SNB, and that’s because the 2008 crisis hit banks mostly in these particular jurisdictions. But the breadth of the current crisis is wider as every country is struggling to get dollars. The dollar needs of Sweden, Norway, Denmark, Hong Kong, Singapore, South Korea, Taiwan, Australia and Brazil and Mexico seem particularly striking for a variety of reasons.

Finally, sooner or later, one will also have to include China - and its upcoming dollar maturity wall - to this list. In short, "the Fed’s dollar swap lines need to go global, the hierarchy needs to flatten." * * * Concluding the surprisingly short - for his standards note - Pozsar says that the message for central banks that emerges from this brief note is this: backstop not only the banks at the core of the financial system, but also markets and non-banks. In short: backstop/bailout everyone. The market backstops should include the CD and CP market where we need a buyer of last resort as the structural buyers of paper are losing cash fast; the backstop of the FX swap market should include daily operations at more points along the FX curve. Additionally, "Like primary dealers offer round the clock liquidity across timezones, dealers of last resort – the central banks of the swap network – should offer dollar liquidity round the clock too." Finally, like primary dealers, who trade with anyone with an ISDA, dealers of last resort should too: "the Fed by broadening access to other central banks and other central banks by broadening access to dollar auctions to non-banks like life insurers and asset managers." While free market capitalists will howl with rage at what the former Fed staffer is proposing, he makes a valid point that demand on bank balance sheets will increase from here to provide credit locally for the real economy – that will consume balance sheet and risk capital and will naturally leave less room for market making and arbitrage, which under current circumstances are luxury. Of course, none of this would have been an issue if instead of buying back trillions in their own stock, pushing the stock price to all time highs, corporations had simply saved for a rainy day... a day like today when it is pouring and hailing. But alas, while we warned repeatedly that a day of buyback reckoning is coming, nobody bothered to do anything at the time to reverse it. And now it's too late. In his final observation, Pozsar writes that "while it’s too much to ask central banks to lend to the real economy" - but why, after all if we are going there, why not load up the proverbial helicopter with money and just make it rain: why should just the financial sector benefit from this last systemic bailout - "it’s not too much to ask them to become more active in making markets as banks free up balance sheet for lending more to the real economy. The breakdown of o/n repo markets today tell us that balance sheet is now scarce to conduct even the most basic type of market making." He also points out that while charts showing Target2 balances became known as the visual representation of the ECB clearing payment imbalances between northern Europe and southern Europe through the balance sheet of local central banks within the eurozone, "it’s now time for the Fed to do the same globally with other central banks and for those central banks to lend broadly – after all what is at stake here is the funding of U.S. assets: Treasuries, MBS and credit." In short: bail out everyone... everywhere. The alternative is 107 years of fake price discovery and Fed market manipulation crashing upon themselves, ending the fiat system as we know it, and leading to the biggest social, economic and financial catastrophe of all time.

|

Send this article to a friend:

|

|

|

Two weeks ago, on March 3, before a liquidity panic had gripped capital markets, corporations and global banks, Credit Suisse repo icon and former NY Fed staffer, Zoltan Pozsar issued a recommendation to halt the funding crisis early in its tracks, writing that the Fed should "combine rate cuts with open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary." Unfortunately, since then the coronavirus supply chain (and payments) crisis has been joined by the oil price war, which has crippled the petrodollar exchange system by sending the price of oil sharply lower and exacerbating the global dollar funding shock.

Two weeks ago, on March 3, before a liquidity panic had gripped capital markets, corporations and global banks, Credit Suisse repo icon and former NY Fed staffer, Zoltan Pozsar issued a recommendation to halt the funding crisis early in its tracks, writing that the Fed should "combine rate cuts with open liquidity lines that include a pledge to use the swap lines, an uncapped repo facility and QE if necessary." Unfortunately, since then the coronavirus supply chain (and payments) crisis has been joined by the oil price war, which has crippled the petrodollar exchange system by sending the price of oil sharply lower and exacerbating the global dollar funding shock.

our mission:

our mission:![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)