Send this article to a friend:

March

02

2018

|

Send this article to a friend: March |

|

The Albatross Of Debt: The Stock Market's $67 Trillion Nightmare, Part 2

Needless to say, we have reached the mane. What drove the US economy for the past three decades was debt expansion----private and public--- at rates far faster than GDP growth. But that entailed a steady ratcheting up of the national leverage ratio until we hit what amounts to the top of the tiger's back---that is, Peak Debt at 3.5X national income. As we also showed yesterday, the fulcrum event was Nixon's abandonment of the dollar's anchor to a fixed weight of gold at Camp David in August 1971. That unleashed the Fed to expand it balance sheet at will, thereby injecting fiat credit into the financial system at relentlessly accelerating rates; and it also paved the way for takeover of the FOMC by Keynesian academics and apparatchiks in lieu of the conservative bankers and money men who had run the Fed prior to 1970. At length, the Fed's balance sheet grew by 82X over the 48 years since June 1970, erupting from $55 billion to $4.5 trillion at the recent QE3 peak. The effect was drastic and enduring financial repression that drove bond yields far below what would have prevailed on the free market based on the supply of domestic real money savings. Stated differently, as the so-called "reserve currency issuer" the Fed's massive balance sheet eruption forced money-printing reciprocity among all the central banks of the world owing to the fear of rising exchange rates---a syndrome which afflicts politicians and policy-makers everywhere. So the convoy of modest central bank balance sheets that collectively stood at perhaps $80 billion in June 1970 totals more than $22 trillion today. That is, herded-on by the rogue central bank unleashed at Camp David, the convoy of global central banks evolved into a gigantic yield-insensitive bond buyer. For all practical purposes, they collectively operated the monetary equivalent of roach motels: The bonds went in but never came out. This massive sequestering of real debt funded by fiat credits, which central banks conjured from thin air, had the obvious first order effect of suppressing yields well below honest market clearing levels. That's just the law of supply and demand 101. But the second order effect----front running by carry-trade speculators----drove bond prices even higher, thereby pushing yields even deeper into sub-economic levels. That, in turn, caused the carry cost of debt relative to income to steadily fall, incentivizing the public and private sectors alike to ratchet up their leverage ratios to levels that were unheard of prior to 1970. At length, cheap debt got built into the warp and woof of public and private sectors alike. So doing, rising leverage ratios caused future economic activity to be pulled forward in time----meaning that domestic and world GDP are far higher than they would otherwise be had growth been funded by real savings extracted from current production, not debt enabled, financed and stimulated by central banks. For example, fixed asset spending financed on the margin through central bank bond purchases---directly or indirectly through arbitrage displacement---added to GDP faster than savings-based investments would have otherwise. Even then, however, the eruption of global central bank balance sheets proceeded apace at rates dramatically faster than the growth of debt-bloated GDP. Thus, global GDP has expanded from about $3 trillion to $80 trillion since 1970 or by 26X. By contrast, the balance sheets of central banks has exploded by around 275X. Yet, as economist Herb Stein once famously observed, things which are unsustainable tend to stop. And foremost among them at the present juncture is the central bank driven explosion of total debt.

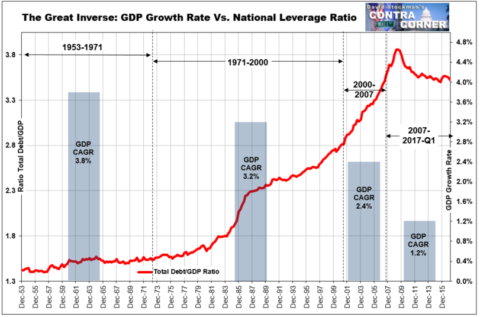

Indeed, the current state of the US economy and its total public and private balance sheet embodies Stein's Law in spades. To reiterate: In June 1970 the GDP was $1.1 trillion and it has since expanded by 18X to $19.6 trillion. By contrast, total public and private debt outstanding was $1.58 trillionand has since expanded by 42X to $67 trillion. In effect, the law of compounding eventually rules. That's because to extend these unsustainably divergent trends for even another decade would lead to an outright absurdity. As we also pointed out in Part 1, ten years from now nominal GDP would total $35 trillion and total public and private debt would reach $150 trillion. Can you say, tilt! Even the Fed thinks so. And that is the real reason for its pivot to rate normalization and QT (quantitative tightening). Unfortunately, our monetary central planners fail to realize that the 50 year march up the blue line (debt) in the chart below has badly injured the main street economy, and that as it "removes accommodation" and shrinks its balance sheet the damage will only be further compounded. Secondly, during the final phases of the 50-year debt bubble, cheap debt increasingly cycled back into the canyons of Wall Street via corporate buybacks, M&A deals and other financial engineers maneuvers. There it fueled an enormous inflation of financial asset values and a veritable tsunami of speculative invention and dangerous wagering. To wit, there never would have been a double inverse VIX ETF under a regime of honest money and free market financial discipline; nor would you find European junk bond yields trading inside of US treasuries or radically cyclical, price sensitive shale oil plays funded with junk bonds, or "volatility" being traded as an "asset class". In a free market, the latter would have no trend and would therefore be unprofitable to trade. In a word, the long-running illicit regime of Keynesian central banking is now "priced-in" to the entire warp and woof of the world's $300 trillion market for debt ($220 trillion) and equity securities ($80 trillion). Therefore, as the Fed moves forward into the terra incognito of QT and the massive draining of cash from the canyons of Wall Street, thereby eventually triggering reciprocal QT up and down the rest of the global central bank convoy, its essential impact will be to "un-price" the falsifications, distortions, deformations and malinvestments accumulated over decades. Needless to say, "un-pricing" will trigger chain reactions or what the central bankers are pleased to call "contagions" throughout the interstices of the world's vast financial system. Mis-pricing was pleasant and arrived slowly, silently and incrementally; un-pricing, not so much. Indeed, what lies ahead is akin to what Keynes once observed (in 1919 when he had not yet gone off the deep end) about the insidious workings of inflation: It gets embedded so deeply in the fabric of finance and economic life that it becomes virtually invisible. Substitute "financialization" and debt-fueled "asset inflation" in the Great Thinker's most famous quote, and you have exactly what the era of Bubble Finance has wrought in the present day world.

In any event, buried in the chart below is the enormous damage to Main Street and Wall Street alike that has remained dormant most of the time since 1970. But no more. The great pivot to central bank QT is about to trigger Warren Buffett's equally famous aphorism: The naked swimmers are about to be beached and exposed.

At the main street level, it has long been evident that the nation's post-1970 LBO is grinding the trend growth of real GDP steadily lower. Like in all debt driven economies, the initial impact was pleasant because the incremental activity which was brought forward in time more than outweighed the rising carry cost of the debt. But those salutary effects were temporary. Thus, the first panel on the chart below represents the pre-Camp David status quo ante. During 1953-1971---the golden age of US prosperity-----real GDP grew at a 3.8% rate per annum rate, while the US economy's historic leverage ratio hugged tightly to the 1.5Xgolden mean. Growth was organic, sustainable and arose from the genius of private capitalism relatively untrammeled by heavy-handed state intervention. As shown by the red line in the second panel for 1971-2000, the leverage ratio began its relentless climb--accelerating sharply after Alan Greenspan arrived at the Fed in 1987 and explicitly launched the era of Bubble Finance. During this period, the boost to growth from more leverage was only partially off-set by the rising burden of debt carry costs. The third panel for 2000-2007 captures the final manic blow-off phase of the national LBO when the Greenspan housing boom took mortgage debt into the financial stratosphere. During that seven year interval of insanity, the national leverage ratio soared from an already extended 2.8X national income to 3.8X at the financial crisis peak. But not withstanding the greatest debt pumping spree ever---including more than $3 trillion of mortgage equity withdrawal (MEW)---which flowed into the consumption spending stream, the toll on economic growth became patently obvious. On a peak-to-peak basis, real GDP growth slowed to just 2.4% per annum. The final panel covers the ten years since the pre-crisis peak and speaks for itself: Notwithstanding the greatest one-two punch of fiscal and monetary "stimulus" in recorded history, the debt ratio stopped growing and so nearly did the main street economy. The red line has modestly rolled over because households were already at Peak Debt in 2007 and business debt has grown only modestly----even as it was almost entirely cycled back into Wall Street via financial engineering. The bottom line, however, leaves little to the imagination. In combination, the carry cost of what is now $67 trillion of public and private debt and the acceleration of C-suite strip-mining of corporate cash flows and balance sheets into order to fund financial engineering, have caused the trend rate of real GDP growth to fall to just 1.2%. That's barely one-third of the rates posted during the golden era of growth prior to the folly of Camp David. Needless to say, the paint-by-the-numbers folks at the Fed and on Wall Street have no clue about the dismal reality represented in the graph below. They are so focused on the short-term "flows" and high-frequency "incoming data" that they recognize neither the fact of the national LBO, as so stunningly evident in the red line, nor the demise of historic economic growth, as is so unequivocally evident in the grey bars. Moreover, by now the claim that the tepid recovery is owing to the deep plunge of the Great Recession doesn't wash. To the contrary, if that shock to main street was merely cyclical, as claimed by our Keynesian central bankers, the lost GDP would have been more than recovered after 9 years from the bottom. In fact, however, the 1.2% real GDP growth rate in the final panel represents the permanent condition of the main street economy and exposes the real truth about the 40-year debt bubble. To wit, the US economy has reverted to payback time. That's the real price of $67 trillion of debt and leveraging the US economy to its peak tolerance at 3.5X national income.

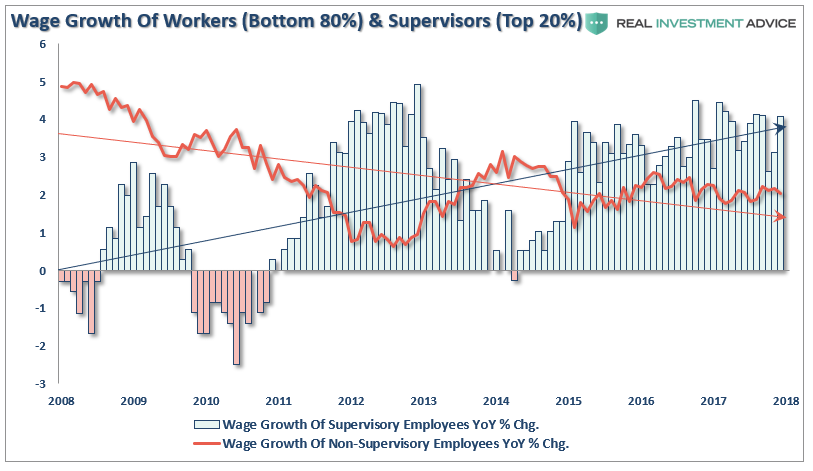

Even then, the grey bars in the chart above probably understate the severity of damage to the main street economy that has resulted from the post-1970 debt explosion. That's because some significant part of even the tepid trend growth since 2007 is owing to the hideous reflation of the stock market and resulting (reversible) wealth effects since March 2009. What we mean is that the top 10-20% of US household have benefited---both financially and psychologically----from the 4X rebound of the S&P 500 (from 670 at the March 2009 bottom to approximately 2750 at present). Accordingly, they have captured sufficient wage and salary increases plus capital gains to finance robust consumption spending levels. That spending at the top, in turn, has boosted the punk aggregates that are being held down by the 80% of the households at the bottom, which own little stock and have experienced tenuous wage gains, if at all. The chart below is striking proof, and it happens to divide the work force on a 20/80 basis. The trend rate of the red line, reflecting production and non-supervisory workers, has actually been falling, not rising, since the 2008 crisis. At the current rate of 2.3% Y/Y growth, nominal wage growth is hardly keeping up with CPI inflation, which itself considerably understates the true rise in the cost of every day living. By contrast, the top of the job ladder is comprised of so-called supervisory workers. Their wages have generally accelerated since the post-crisis bottom and are now in the 4% growth zone. That's in part due to the fact that the top 20% of jobs have been considerably less exposed to the off-shoring of US production and wages, and also because the supervisory category of workers captures the lions share of bonuses and incentive pay. Consequently, the top 20% of job holders have contributed disproportionately to the modest rebound of consumption spending and reported GDP growth since 2009.

In fact, as we will show in Part 3, the great bulk of the main street economy has flat-lined at best since 2008. For instance, industrial production is still flat with it pre-recession level and real weekly wages of prime age workers have not risen at all. Consequently, the massive monetary stimulus since September 2008 has never really left the canyons of Wall Street; the massive inflow of central bank credit has simply extended and elevated the financial distortions and excess valuations that have been building there for decades. So un-pricing the central bank financial bubble will hit Wall Street a lot harder than main street, which has far less to loose. And we believe the hit to Wall Street will start with the great dip-buyers in the C-suites of corporate America. Having loaded themselves up with cheap debt in order to fund $15 trillion of financial engineering maneuvers over the last decade, the "yield shock" dead ahead will slam the flow of corporate cash into stock buybacks and M&A deals---even as it eats upwards of $40 per S&P 500 share in higher pre-tax interest expense. More importantly, the chain reaction triggered by slumping stock buybacks will be virtually uncontrollable. The great wall of passive investment vehicles-----ETF and indexed funds----will automatically dump stocks when the smart money realizes that the jig is up and that the carry costs and risks of speculation have suddenly shot dramatically higher. We have called this prospect Wall Street's worst nightmare. In Part 3, we will further examine the particulars of the financial time bombs that are unavoidably lurking in the two extra turns of debt----$37 trillion----which weigh heavily on the economy and financial system. It amounts to a monumental central bank triggered yield shock that is most definitely not priced-in.

avid Stockman was a two-term Congressman from Michigan. He was also the Director of the Office of Management and Budget under President Ronald Reagan. After leaving the White House, Stockman had a 20-year career on Wall Street. He’s the author of three books, The Triumph of Politics: Why the Reagan Revolution Failed, The Great Deformation: The Corruption of Capitalism in America and TRUMPED! A Nation on the Brink of Ruin… And How to Bring It Back. He also is founder of David Stockman’s Contra Corner and David Stockman’s Bubble Finance Trader.

davidstockmanscontracorner.com

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)