Send this article to a friend:

February

22

2023

|

Send this article to a friend: February |

|

The Market Faces A Second "Shattering Revelation"

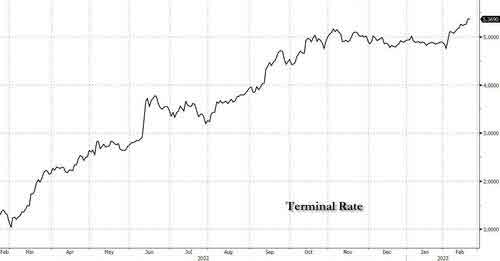

Yesterday saw stocks swoon (S&P -2.0%, Dow -2.1% to negative year-to-date) and bonds slump (US 2-year yields +10bp, 10-year yields +12bp to test closer to 4%), with expectations of the Fed Funds terminal rate rising to 5.35% - still 15bps short of reality, but a partial market catch-up to it.

There were lots of reasons why the “2023 is not 2022 because reasons!” crowd saw their hopes shattered. First, early February global PMI surveys underlined growth is picking up in services, where inflation, staff shortages, and pay pressures are most deeply entrenched: Japan was 53.6 (vs. 52.3 in January), the Eurozone 53.0 (50.8), the UK 53.3 (48.7), and the US 50.5 (46.8). Where is the economic downturn that means unemployment rises, so rates and yields plunge, so stocks surge? Second, Timiraos of the Wall Street Journal highlighted research from the Cleveland Fed arguing "A deep recession would be necessary to achieve”2.1% inflation by 2025, i.e., the curve flattening trade. Yet, “the researchers also conclude that, **if 2.8% inflation doesn't result in an un-anchoring of inflation expectations**, the December FOMC projection (in which inflation stays somewhat above the 2% target for longer) would be the optimal policy.**” That’s a hypothetical argument for curve steepening trades, surely? Third, geopolitics. President Putin’s bellicose national address expressed that Russia feels betrayed by the West, despises what the West now is, and won’t retreat from Ukraine. President Biden, in Poland (not France or Germany) stressed in lofty terms that the US will never abandon Ukraine. As the Guardian puts it, Biden and Putin both implicitly tie their futures to the outcome in Ukraine. That will be expensive for one, or both, politically. It is expensive economically too. Higher production of military goods is inflationary. Poland are doubling their defence spending to 4% of GDP: the rest of the EU is doing a tenth of that in new spending while waiting for the US to lead. Are you putting a Cold War surge in defence spending and the need for a larger army despite labour shortages into your inflation projections? No? Because in an op-ed Monday, Dutch Prime Minister Rutte wrote...

Escalation will also be costly for the geopolitical and geoeconomic architecture markets rest on. A European Council on Foreign Relations (ECFR) survey of opinion in nine EU states, the UK, US, China, Russia, India, and Turkey underlines the war in Ukraine is “defining a new world order”. This is no revelation to anyone outside Europe or blue states in the US, and the limited subset of countries surveyed still displays Western-centric thinking. However, the revealed sharp geographical differences in attitudes to the war, democracy, and the global balance of power suggest to the ECFR that we may be at an historic turning point to a “post-western” world order. “The paradox of the Ukraine war is that the west is both more united, and less influential in the world, than ever before,” says the ECFR’s director. The unity is clear as PM Rutte argues, “I cannot see how this will be China’s century… the 21st century will be the century of democracy and thus the century of America,” and, “It is extremely important that we in the Netherlands and Europe appreciate the great role of the US.” Yet the loss of influence is also clear, as the Wall Street Journal is blunter: “Russia, China Challenge US-Led World Order” – and to thunderous applause in places. Relatedly, Friday will see China’s proposed peace plan for Ukraine. Any such attempt should be applauded, but the question is on whose terms. Western observers remain skeptical the plan will see any concrete details, while rumors are also flying China may threaten to do for Russia what the US is doing for Ukraine, amplified by the news that Xi Jinping will visit Moscow soon. Logically, assuming China is not going to dump Russia, which it won’t, there are few potential outcomes:

In short, the most logical probability is that neither the China peace plan nor the upcoming Xi visit to Moscow provide anything new. In which case, Ukraine escalation, inflation, and global polarisation it is. Yet the fact that we have a war in Ukraine at all should underline that the fat tail-risks are of something even worse – a scenario we originally flagged in our Ukraine metacrisis report in early 2022. If you think markets are unhappy in recognizing that they have been wrong on Fed Funds again, wait until they grasp that shattering revelation.

Michael Every is the Head of Financial Markets Research Asia-Pacific. Based in Hong Kong, he analyses the major developments in the Asia-Pacific region and contributes to the bank’s various economic research publications for internal and external customers and to the media. Michael has nearly two decades of experience working as an Economist and Strategist. Before Rabobank, he was a Director at Silk Road Associates, a strategy consultancy based in Bangkok. Prior to this, he was Senior Economist and Fixed Income Strategist at the Royal Bank of Canada based in both London and Sydney. Michael was formerly also an Economist for Dun & Bradstreet in London, covering ASEAN. Michael holds a Masters degree in Economics (with distinction) from University College London and speaks Thai.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)