Send this article to a friend:

February

10

2023

|

Send this article to a friend: February |

|

Money and recession

Monetarists are warning now that money supply has stopped growing and even turned negative, so we are heading for a recession. This article examines the position for US dollar M2 money supply and the prospects for the US economy. But monetary growth, or the lack of it, doesn’t only affect GDP, but a large element of economic activity which is not included in it, principally financial activities, and the acquisition of assets such as property. This raises the question: is the downturn in money supply due to financial activities, or the non-financial economy? What is its actual relevance? In this article, I delve into the relationship between credit and the economy. I examine the process of credit contraction. I conclude that rather than relying solely on the monetarist’s favourite indicator, an understanding of the credit cycle and loan officer surveys are more valuable evidence. The credit cycle In the current economic climate, there are increasing fears of recession. Because the definition of a recession is imprecise, I prefer to call it a downturn in economic activity, or if it is significant, a slump. Either way, it begs the question as to what the cause is. Other than the consequence of the withdrawal of bank credit, all other explanations are unsatisfactory. Before Keynes discredited markets in favour of government intervention, it was commonly understood that intervention was not the solution. Austrian economists had perfected their business cycle theory, which explained the relationship between variations in credit and economic activity. But no matter; Keynes was determined that government intervention was preferred to the boom and bust under free markets. He observed the failure of free markets, failing to understand it was the consequence of credit cycles. Perhaps the Austrians should have called it a credit cycle, instead of a business cycle. It is credit which drives business activity, and perhaps a wider appreciation of credit cycles would have made Austrian business cycle theory more widely understood. Indeed, the best way to counter the Keynesians who rewrote economics to suit their statist sponsors is to explain the role of bank credit. And with legal money removed from the picture, which is physical gold, all economic transactions are settled in credit — bank notes which are central bank credit and deposit accounts which are the counterpart to credit created by commercial banks. Together, they are erroneously described as money, as in the phrase “money supply”. The point about real money is that its value was recognised across jurisdictions by everyone. But apart from smaller amounts settling transactions in silver and copper coin, money was always less convenient than money substitutes, which we can define as credit where its value differed from money only in respect of counterparty risk. The amount of this credit or currency rapidly became considerably greater than the money it represented, but so long as its expansion was within credible limits, it retained the value of money as its substitute. Credibility, and not the quantity was key. Where monetarism originally erred by tying a currency’s purchasing power to its quantity was in dismissing human confidence in the purchasing power of gold, and so long as people believed the link with currency was sound, they would accept it as a substitute, despite changes in its quantity. But how could this be, when mathematics clearly indicate that the expansion of a currency’s quantity would dilute its purchasing power? The answer is that the tendency for prices to rise as the quantity of a gold substitute is expanded is countered by individuals deciding not to pay the higher prices, preferring to hold onto their money substitutes instead. In other words, they place values on not only goods and services, but on gold as well. But when the link between money and a currency is broken, this confidence is displaced by confidence in the currency. And that is the case today, with the state now telling everyone that its currency is money, and not gold. We are commanded to use it by fiat. Instead of a globally accepted money without counterparty risk, we now must rely on faith and credit in our state as issuer and guardian of its value, and everyone else is equally reliant on their government currencies as well. Consequently, the current monetary system is inherently unstable in terms of its purchasing power. No longer are changes in its quantity automatically absorbed by its users as if it was a credible gold substitute. The issue has become more complex. We only use our currencies as if they are gold substitutes by way of habit. People hold onto their deposits in the banks and are prepared to accept a gold-like return on their government bonds, which is why with CPI roaring ahead US Treasuries’ ten-year maturities are acceptably priced for a yield of 3.5%. Underlying this backwardation between the Federal Government’s obligations and reality is a legacy of faith, that when the dollar and the entire global currency system abandoned the Bretton Woods agreement, nothing actually changed. Really? The history of the relationship between gold’s purchasing power and the major fiat currencies tells us otherwise.

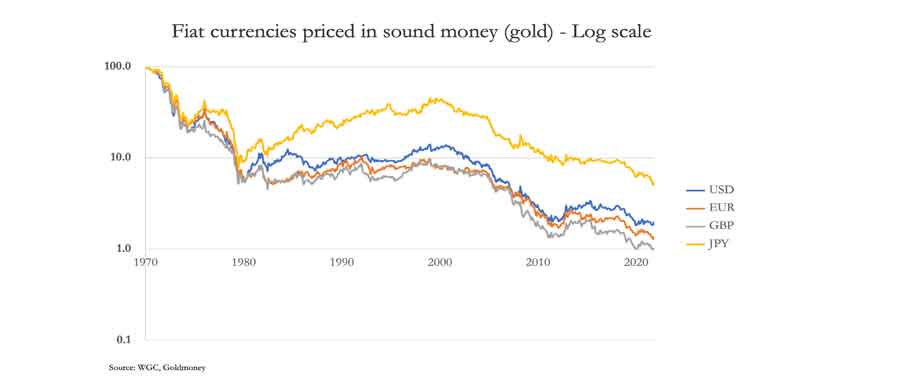

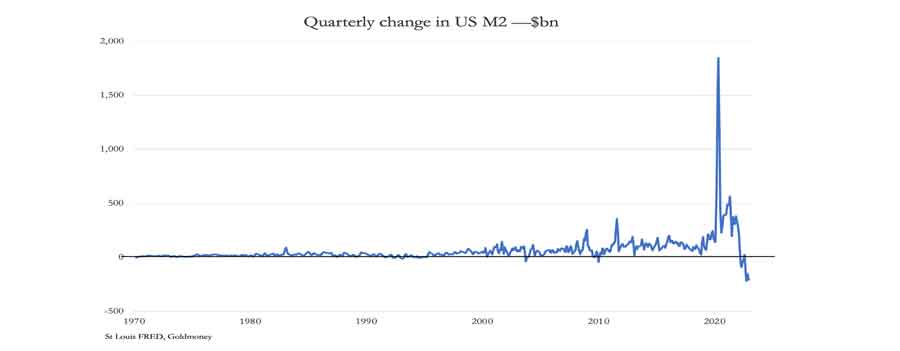

Eventually, government abuse of their fiat currencies always leads to their demise — that is the lesson of history, and we are currently observing the process. This is the big-picture background against which today’s central banks are tasked with managing the upcoming recession. We know from official monetary policies that central banks rely on the expansion of credit to prevent recessions. More specifically, they rely on credit at the central bank level to kick-start things. Originally it was pure Keynesianism, with deficit spending being the means of stimulation, but that has now evolved into attempts at wider economic management by suppressing interest rates, quantitative easing, and even direct injections of central bank credit into individuals’ bank accounts. And now there are even plans to bypass commercial bank credit by the invention of an entirely new class of central bank liability, central bank digital currencies, not as a replacement for central bank currency but an addition to it. The unrecognised danger comes from commercial bank credit taking its cue from fiat currencies and not gold. When a central bank increasingly expands its credit, there comes a point when it is realised that the state’s fiat currency is nothing like a gold substitute and is in acute danger of becoming worthless. Economic actors begin to realise that it’s not prices which are rising, but the purchasing power of a currency falling. In our interconnected world, the dawning of this realisation commences in the foreign exchanges, long before domestic users of a currency become aware of its debauchment. But in time, they will learn that their government’s substitute for genuine money is not backed by anything, and nor is all its associated credit. As stated above, every fiat currency ends this way, and we can safely assume that today’s fiat currencies will equally prove to be ephemeral. In theory, at least, their demise can be gradual, taking decades. The chart above, which shows the dollar has already lost over 98% of its purchasing power since the last tenuous link with gold was abandoned, has been declining for over five decades. And that’s not including the dollar’s 40% devaluation in 1934. The relevance of this background is that the currency issue is becoming centre stage to geopolitics, with the US Government’s abuse of its currency hegemony now being challenged by China and Russia. These powerful nations are not easily destabilised by currency embargoes. And they have attracted the majority of the world’s population away from the fiat dollar regime into a yet-to-be-defined currency future. But all the indications are that the Asian hegemons realise that international trade requires sound currencies, and that they must return to some sort of gold backing. It is extraordinary that these developments are as yet on no one’s radar in America and her western allies. So far as we are concerned the currency emperor is richly clothed. The reality is not only very different, but obvious to anyone who cares to look with independent eyes. We are shortly to see a new phase of the proxy war in Ukraine, potentially leading to nuclear brinkmanship. From his statements, President Putin understands the currency question. He has most of the world on his side — which may surprise some readers who are blinded by their own media. In partnership with China in the Shanghai Cooperation Organisation, the Eurasian Economic Union, and BRICS, Russia has the backing of 3.8 billion Asians, a billion Africans, and a further billion or so who are attracted by trade opportunities and a willingness to escape from America’s weaponised currency regime. It compares with 1.2 billions in the western alliance — America, NATO, five-eyes, Japan, and various hangers on. All Putin has to do is reveal plans to incorporate gold into a new Asia-led currency regime, and the dollar will suffer a debilitating flight into commodities. It is the nature of these events that the American public will be the last to wake up to this danger, stubbornly believing that the dollar is money which everyone around the world will always need. But when Asia’s hegemons declare that their interests are served best by backing their currencies with gold and escaping from the west’s manipulative currency schemes, the collapse of our currency illusion could be a speedy process. Common errors in the monetarist approach The economic consequences of governments intervening in their economies is a controversial subject. Before Keynes, it was generally understood that government intervention was undesirable. Following Keynes, it became a primary objective. And as described above, intervention has spread from deficit stimulus to increasingly desperate means of expanding central bank credit. Currency and credit expansion has become a one-way ticket, and any sign of it faltering is viewed with horror. That is why modern monetarists are ringing alarm bells over slowing monetary growth, and in some cases turning negative. In common with the Keynesians, monetarists are inflationists, believing in the state’s management of the economy by regulating the expansion of credit. At the inaugural Mont Pellerin Society meeting in 1947, the debate turned to how to save liberalism. Some attendees argued that their approach needed to be modified, and on his first trip abroad from America, Milton Friedman, argued “we need to agree on the necessity for a positive approach”. Instead of being a debating forum for the evoluton of economic knowledge, in effect these attendees were attempting to enter into political management of outcomes. According to the record of the meeting: “Not all meeting attendees agreed such a reformulation was necessary. Austrian economist Ludwig von Mises was a vocal dissenter, at one point declaring “you’re all socialists!” and storming out of the room. Mises was among a minority contingent who remained uncomfortable with any revision of liberalism that justified an expanded role for the state.”[i] Freidman was reportedly stunned at Mises’s behaviour, but he failed to understand the implications of compromising the fundamental precepts of a science. Mises refused any compromise. He had lived through the Austrian and German inflations, working as an adviser to the Handelskammer (the Vienna Chamber of Commerce), dealing with issues of finance, currency, credit, and tax policy. In his Memoirs, he wrote that his only regret was his willingness to compromise by permitting politics to corrupt his science. He was not about to make that mistake again at Mont Pellerin. Von Mises had lived through an episode that completely disproved monetarism as promoted by Freidman. In a fiat currency, the concept that managing the quantity of credit would deliver economic outcomes had failed spectacularly in Austria and Germany. Instead of credit expansion by the central bank delivering economic recovery, it led to total economic collapse. And claims by modern observers that the abuse of credit was primarily to fund the state and not engender economic recovery amounts to skating on very thin ice, both factually and intellectually. The role of commercial bank credit It is with this important caveat that we must with scepticism regard any supposed link between changes in the quantity of credit and economic outcomes. Apart from the work of early Austrians, few attempts have been made to understand the role of commercial bank credit in the economy. Bank credit is over 90% of circulating media, yet some mainstream economists even deny the ability of banks to create it out of nothing, let alone understanding the process, exposing their ignorance of this important subject. To complicate matters even further, they fail to understand that when they talk of economic growth measured by GDP, they are actually talking about the expansion of commercial bank credit. Without that, there is no economic “growth”, because GDP is the sum of credit deployed in all GDP transactions. Furthermore, we must distinguish between economic progress, which surely, is what we really mean when we use the term, “growth”, and the financial record of qualifying transactions. Changes in GDP are not measures of progress, but a summary of changes in credit deployed. It is impossible to measure progress. However, without an understanding of credit, all monetary analysis is worthless. And now, we face a contraction of bank credit in the world’s reserve currency, as the chart below shows.

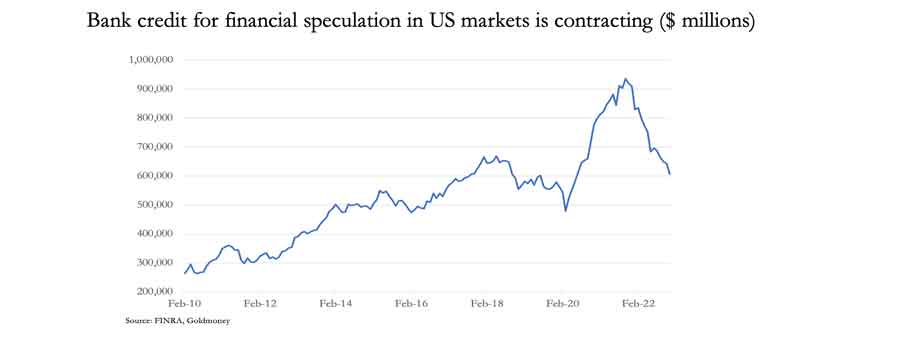

Since the abandonment of Bretton Woods, the average quarterly change in US M2 was $68 billion up to a year ago, increasing over time. Since then, a serious contraction has set in with M2 appearing to implode. With the currency element still growing, the collapse of M2 is purely down to deposits at the commercial banks, the principal means of their balance sheet funding. A significant application of money supply is for non-qualifying GDP transactions, principally financial in nature or for the acquisition of non-financial assets, particularly residential and commercial property. The chart below shows how the quantity of credit has changed with respect to one aspect of financial transactions in the US, the application of credit to speculation in listed securities.

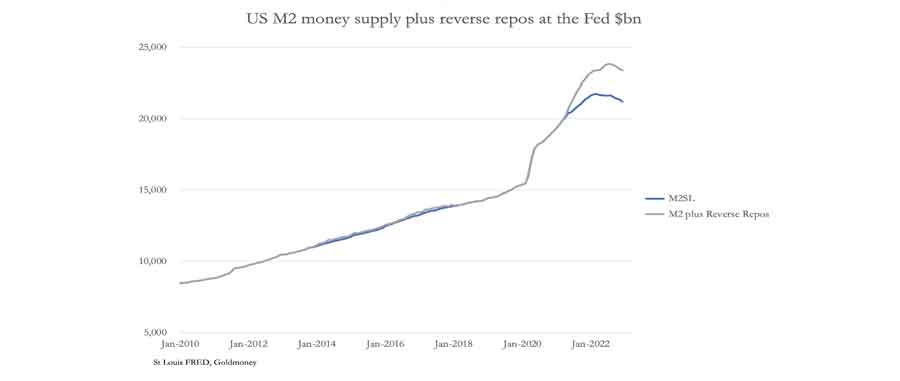

Since October 2021, margin loans have contracted by $330bn. Virtually all this bank credit is secured by collateral, which in the case of distressed borrowers would have been liquidated. Losses to the lending banks would have been negligible. But to understand the consequences for money supply statistics which principally consist of commercial bank liabilities to their depositors, we must delve into how deposits are created and extinguished. A bank deposit comes into existence when a loan is made to a customer. It must be the case, because double entry bookkeeping requires there always to be a balancing ledger entry. Having taken out a loan, the bank’s customer will draw down his facility (i.e., his bank deposit) to pay his obligations. In effect, he novates his credit at his bank in favour of other parties. When it is novated to another party with an account at the same bank, then the bank’s overall deposit obligations do not change. But if the deposit obligation is novated to another bank, then the lending bank must replace it with another deposit obligation. In practice, payments between banks occur all the time, so that balancing a bank’s deposit liabilities with its assets is a function of lending surplus deposits or borrowing to make up a deficiency from other banks. This is why wholesale money markets exist. Assuming all the banks in a banking network are continuingly solvent, then novations of credit across the system must always balance. Daily excesses and shortfalls only occur in individual banks. Monetary statistics are a summation of the entire banking system’s deposit liabilities. To understand the effects of transfers between individual banks is therefore unnecessary, so the way to understand how changes in money supply come about is to treat the entire commercial banking system as a single entity. This permits us to consider the consequences for monetary statistics of the withdrawal of total credit of $330bn from lending to finance the acquisition of listed securities. For simplicity, let us assume that a bank forecloses on its loan by selling the collateral for exactly the value of the loan. Therefore, on its balance sheet, the proceeds of the sale balance the deposit obligation to the customer, and both are written off the balance sheet. The bank no longer has the loan as an asset, the depositor has no deposit obligation from the bank in his favour, and the collateral has been removed. In other words, outstanding bank credit has been extinguished. Therefore, since US M2 money supply includes this $330bn contraction, we can also conclude that if financial assets continue to fall in value, more money supply will be liquidated. And we can extend this analysis into non-financial lending, which is the engine that creates bank deposits for the wider population. The same procedure applies. A bank will make a loan for various non-financial purposes, either secured or unsecured by collateral, to businessmen and consumers alike. While their accounts at a bank may not reflect the accounting position (commonly recording a customer’s account as overdrawn with a credit limit instead) in the bank’s books all loans will have balancing entries of deposits in favour of the customers to which they are made. When a loan is extinguished, the balancing entry is as well. If the asset side of an entire banking system contracts, then so will its liabilities. Deposits will be cancelled, and where losses occur, they are written off against shareholders’ funds. The position of deposits which have been novated to savers who have no matching obligations to their bank is secure, so long as the bank discharges its credit obligations. The origin of their deposits will have been loans to an earlier party, deposit obligations that may have been novated many times. But once novated, they cannot be written off by a bank because they are an obligation to a customer against which the bank has no counterclaim. If a bank develops a view that it must reduce its risk, then it will either call in or refuse to extend the loans which it deems are most at risk of failure. These actions will affect the supply of credit to the non-financial sector, reflected in a downturn in deposits, and therefore money supply statistics. And when an entire banking cohort takes this view, the withdrawal of credit reflected in money supply statistics results in an economic downturn, commonly referred to as a recession. It should be noted that a recession does not emanate from businesses turning collectively cautious over trading prospects, but from the contraction of bank credit. REPO markets are increasingly important Back in 1979, I got my first consultancy contract with a London-based bank. I observed that imbalances in the consortium bank I worked with were settled daily in the interbank market. In the absence of retail customers, after participating in syndicated loans and trading in floating rate notes this bank always had surpluses to lend into the interbank market. The interbank market is uncollateralised, and the consortium bank controlled its counterparty risk by having position limits with all the other banks operating in that market. In those days, the limits for all but the largest banks were no more than a few million pounds. Moving on to today, the interbank market still operates this way, but for larger imbalances collateral is required. The Bank of England introduced repurchase agreements (repos) for the gilt market in 1995, and the use of repos, which are collateralised loan agreements, has spread into routine bank liquidity finance, and is used for financing additional security leverage. According to the European Repo Market Survey of October 2022, in the UK and Europe repos totalled a record €9,680 billion last June: 54.7% was in euros, 15.6% in sterling, and 20.3% in US dollars, with the balance in yen and other currencies. Clearly, since the repo market kicked off in Europe, it has evolved into a major element in banking liquidity. We await with interest to see what happens to these markets as interest rates and repo rates continue to rise, and collateral values fall — as they will surely do, when the Ukraine conflict escalates in the coming weeks. In the US, repos are also a major means of obtaining liquidity, but there is an additional feature. The Fed offers a reverse repo facility which currently absorbs excess liquidity from the banking system amounting to over $2 trillion. Eligible counterparties are money market funds, primary dealers, banks, and government-sponsored enterprises. For these institutions, they are in effect operating a deposit account at the Fed. The reason reverse repos at the Fed have increased is mainly due to the Basel 3’s net stable funding ratio, which penalises banks with large individual deposit liabilities, favouring retail depositors instead. This is why JPMorgan is expanding its global retail funding sources through its Chase brand, while turning away money-market funds. For the dollar, at least, while these large deposits have been removed from public circulation by being deposited at the Fed, the reverse repo facility is overwhelmingly short-term and should be added back to the M2 statistic. M2 so adjusted is illustrated below.

From this adjustment we learn that since 2010, the quantity of currency and deposits has increased by 175%, and that the downturn in the last year has been more marked than M2 appears to be on an unadjusted basis. In an economy whose GDP transactions totalled an estimated $26 trillion to last December, to have a circulating medium totalling $23.4 trillion is plainly excessive, suggesting that a substantial element of it is funding financial transactions. The Financial Stability Board’s estimate of the US’s shadow banking system in 2021 totalled $20.5 trillion on a narrow measure. Shadow banks do not create credit, merely borrowing to fund for profitable returns.[ii] Therefore, most of their activities are funded by borrowing from commercial banks, matched by deposits as described above. The future course of M2 money supply will be heavily dependent on the interest rate outlook and how that affects shadow banking activity. There will always be turns to be made in any interest rate environment, but the growth in shadow banking has primarily been a response to declining and ultra-low interest rates. For insurance companies and pension funds, the use of financial leverage to obtain nominal returns is now set to decline. Put another way, the everything financial bubble which has progressively grown with the financialisation of the US economy is being deflated by a change in the underlying interest rate trend. The consequences for the dollar’s M2 money supply, of which bank deposits are 90.5% of our adjusted M2 in the chart above, will see a continuing decline as shadow banking withers. This has little to do directly with a downturn in the non-financial economy, which makes up GDP. If we could truly isolate bank credit which applies to GDP, then that portion of it would be relevant insofar as a reduction in the circulating medium is restricting economic activity. But we cannot do this exercise. Perhaps more relevant is to acknowledge that a stagnating or contracting M2 money supply, only so far as it applies to non-financial activities, should be adjusted for a rising level of producer and consumer prices. Producer prices are likely to be the more reliable deflator of the money supply statistic because the CPI has been heavily corrupted over the decades. In the case of the US, that would knock about 6% currently off the unknowable GDP portion of M2. At a best guess basis, the withdrawal of credit from non-financial business is in its infancy. The Fed’s Senior Loan Officer Opinion Survey for January released earlier this week confirmed “tighter standards and weaker demand for commercial and industrial loans to large, middle-market, and small firms over the fourth quarter [of 2022]”. Banks responded to the survey that they anticipated a less favourable economic outlook, a reduced tolerance for risk, and the worsening of industry-specific problems. Clearly, the banking cohort’s appetite for balance sheet expansion into non-financials is turning sour. Banks are also reported to be tightening standards on high-margin credit card lending. This survey is more defining than money supply statistics, much of which do not relate to GDP spending, because it tells us where the US economy is in the credit cycle. It is a mistake to think that money supply statistics reliably quantify the economic outlook or tell us anything we already know.

[i] The incident was related in an article for the Mont Pellarin Society by Jennifer Burns: https://www.hoover.org/sites/default/files/research/docs/mps_burns.pdf [ii] See Global Monitoring Report on Non-Bank Financial Intermediation 2022

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)