Send this article to a friend:

February

07

2023

|

Send this article to a friend: February |

|

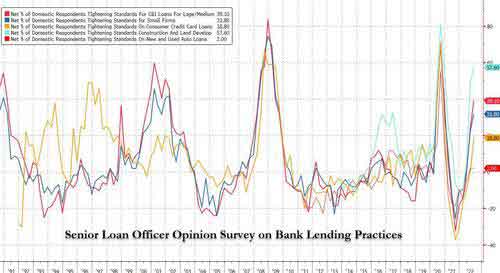

Fed Loan Officers Paints Dire Picture: Loan Standards Approaching Record Tightness As Loan Demand Plummets

As Bloomberg's Vincent Cignarella observed, "tighter credit likely will drive slower spending, a reduction in risk and the potential for the Fed to pivot sooner rather than later to avoid or shorten a potential recession. That would be more good news for bond bulls."

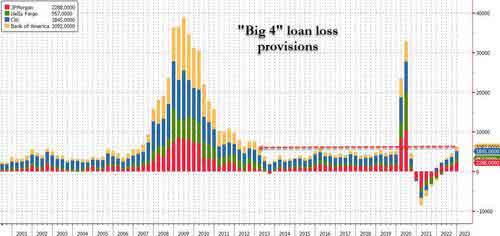

Furthermore, the tightening standards are a result of most banks assigning the probability of between 40% and 80% to the likelihood of a recession in the next 12 months, with no bank reporting a probability less than 20%. Needless to say, in a recession loan losses soar which is why banks are seeking to limit their exposure having already boosted credit loss provisions heading into 2023.

As luck would have it, today the Fed released the latest SLOOS report (just ahead of tomorrow's monthly consumer credit update), and it should come as no surprise that standards tightened again while demand weakened broadly for commercial and industrial loans for firms of all sizes as well as for all types of commercial real estate loans. Even more ominously, on the household side, banks also reported weaker demand on balance for credit card, auto, and residential real estate loans, as well as for home equity lines of credit. Here are the main findings in the latest report: The January 2023 Senior Loan Officer Opinion Survey (SLOOS) found that lending standards for commercial and industrial (C&I) loans tightened further in Q4; in fact, as shown in the chart below, loan standards are approaching tights last seen during the covid crash and the global financial crisis: 45% of banks on net tightened lending standards for large and medium-market firms (vs. 39% on net in the previous quarter), while the number of banks tightening lending standards for small firms increased to 44% (vs. 32% on net in the previous quarter). 45% of banks on net widened spreads of loan rates over the cost of funds for large firms (vs. 30% on net in the previous quarter), while 33% on net widened spreads for small firms (vs. 25% on net in the previous quarter). Standards for commercial real estate (CRE) loans also tightened in Q4. 69% (+12pp) of banks on net reported tightening credit standards for construction and land development loans, and 57% (+17pp) on net reported tightening lending standards for loans secured by multifamily residential properties. The number of banks that reported tightening standards for loans secured by nonfarm nonresidential properties increased to 58% (+5pp). Demand for loans secured by multifamily residential properties, secured by nonfarm nonresidential properties, and construction and land development loans all decreased by more than during the previous quarter. Credit standards on mortgage loans also tightened. Standards were almost unchanged for GSE-eligible mortgages (+0.1pp at +0.1%), but tightened for non-jumbo, non-GSE eligible (+10.3pp to +6.9%), Qualified Mortgage jumbo (+10.1pp to +15.3%), non-Qualified Mortgage jumbo (+7.1pp to +14.5%), non-Qualified Mortgage non-jumbo (+2.0pp to +5.8%), and subprime residential mortgages (+3.2pp to +14.3%).

For banks that tightened credit standards or terms for C&I loans or credit lines, all of them cited a less favorable or more uncertain economic outlook as playing a role; 71% cited reduced tolerance for risk; 50% cited a worsening of industry-specific problems; 50% cited decreased liquidity in the secondary market for these loans; 47% cited a deterioration in their current or expected liquidity position; 41% cited less aggressive competition from other lenders; and 24% cited a deterioration in their bank’s current or expected capital position as playing a role. On the other hand, demand for C&I loans from large- and medium-sized firms weakened in Q4; in some case - such as housing - loan demand cratered to record low, while most other categories tumbles sharply as well: 31% of banks on net reported weaker demand for C&I loans for large and medium-market firms, compared to 9% on net reporting weaker demand in the previous survey. 42% of banks reported weaker demand for C&I loans from small firms, compared to 22% reporting weaker demand the previous quarter.

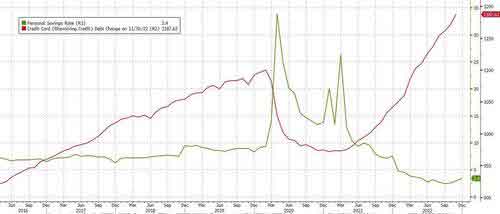

Banks’ willingness to make consumer installment loans decreased in Q4 (-13% on net vs. -7% on net previously). The portion of banks tightening credit standards for approving credit card (+10pp to +28%) and auto loan (+15pp to +17%) applications increased. The portion of banks reporting stronger demand for credit card loans decreased (-22pp to -11% on net), while demand for auto loans also declined (-11pp to -39% on net). TL/DR: the above levels are comparable to previous recessions (and even global financial crisis), and present a powerful contrast with benign market views of an increasingly-likely soft-landing. Bottom line: in a time when US savings have been shrinking fast, and are offset with record credit card borrowings, the only thing that has allowed the party to go on, have been relatively loose loan standards.

But those are now tightening at a furious pace and unless something changes, loan standards will soon hit the tightest on record. At that point, only the most credit-worthy US households will maintain their access to credit; everyone else will be stopped out. The numbers were so ugly, even the Fed's mouthpiece took to twitter to lament the "significant" deterioration in lending standards. Ironically, even though the US economy may be resilient enough to avoid a recession (if one believes the job numbers... as Goldman clearly does which is why it aggressively shrank its recession odds earlier today) it won't matter if banks are skeptical and continue to tighten loan standards, an act which in itself is largely self-fulfilling and reflexive, and could on its own tip the economy into a recession.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)