Send this article to a friend:

February

24

2022

|

Send this article to a friend: February |

|

What Does The Ukraine War Mean For What The Fed Does Next: Here Is Goldman's Take

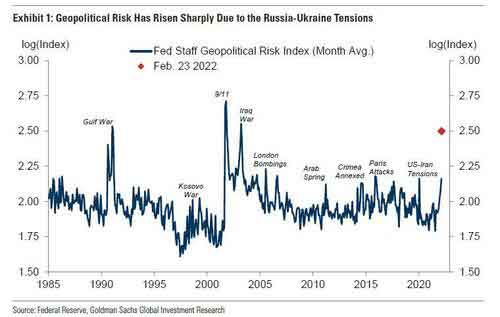

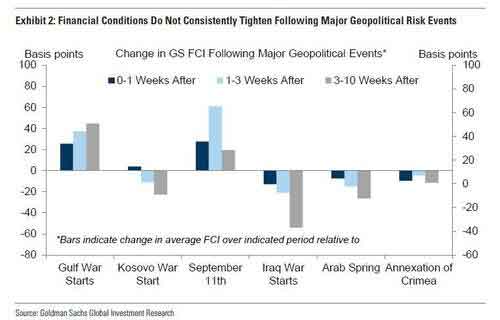

Those are the considerations facing western central banks - and the Fed - as they evaluate whether to push on with continued monetary tightening - to be sure, central banks are always leery of tightening financial conditions into a major global geopolitical conflict - or to relent at least modestly, especially if a global recession is one of the potential side-effects of the war in Ukraine. In a note seeking to address these concerns, overnight Goldman's chief economist Jan Hatzius looks at the implications of the Russia-Ukraine conflict for the US economy and Fed policy, and writes that the silver lining of the conflict is that any direct effects on the US economy should be limited because trade links are weak and energy prices are likely to be affected far less in the US than in Europe. However, the surging price of oil is a big red flag. According to Goldman, a $10/bbl increase in the price of oil boosts US core inflation by 3.5% and headline inflation by 20bp, but lowers GDP growth by just under 0.1%. While that is certainly negative for inflation, (and growth), the impact via tighter financial conditions is the most unpredictable. The next chart shows that past geopolitical risk events have only rarely been followed by a meaningful tightening in US financial conditions, though it is hard to generalize to the current situation. As Goldman puts it, "a larger tightening in financial conditions and an increase in uncertainty facing businesses would further weigh on US growth."

So what does that mean for the Fed? Here we get the first admission from Goldman that Wall Street consensus estimates of as much as 7 (or more) rate hikes in 2022 may not materialize, with the bank writing that "the combination of upside inflation risk and downside growth risk has mixed implications for monetary policy. Historically, Fed officials have sometimes preferred to delay major policy decisions until uncertainty surrounding geopolitical risks diminished. In some cases, such as after September 11 or during the US-China trade war, the FOMC has cut the funds rate." Of course that is not an option with rates now at 0% and inflation, well... higher. Having caveated the dovish case, however, Goldman then sticks to its hawkish guns, and notes that "the current situation is different from past episodes when geopolitical events led the Fed to delay tightening or ease because inflation risk has created a stronger and more urgent reason for the Fed to tighten today than existed in past episodes." And with some signs of "problematic wage-price dynamics emerging and near-term inflation expectations already high" , Hatzius notes that "further increases in commodity prices might be more worrisome than usual." As a result, while Goldman does not expect geopolitical risk to stop the FOMC from hiking steadily by 25bp at its upcoming meetings, "we do think that geopolitical uncertainty further lowers the odds of a 50bp hike in March." In short, Goldman does not expect geopolitical risk to stop the FOMC from hiking by 25bp at its upcoming meetings. But Presidents Bostic, Daly, and Mester and Governor Bowman have cited geopolitical uncertainty as a downside risk to the economic outlook over the last week, and the bank suspects that some participants will see it as a compelling reason not to hike by 50bp in March. For now, the market seems to agree and after hitting almost 100% earlier in the month, odds of a 50bps rate hike have since sunk to just 20%. Meanwhile, looking at the full year, traders are still confident that the Fed will somehow pull off at least 6 rate hikes for the full year without sending the economy into recession.

|

Send this article to a friend:

|

|

|

On one hand, the soaring commodity prices as a result of the Ukraine invasion presage much higher inflation for the foreseeable future (with

On one hand, the soaring commodity prices as a result of the Ukraine invasion presage much higher inflation for the foreseeable future (with

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)