Send this article to a friend:

February

24

2020

|

Send this article to a friend: February |

|

Coronavirus Slams Chinese Economy

Here are the official statistics on the coronavirus (technically COVID-19) as of today: There are 75,685 confirmed infections worldwide, with 98% of that total in China alone. Of those cases, 82.5% are in the single province of Hubei, mostly centered in the city of Wuhan, with 11 million residents. Of the over 75,000 worldwide cases, there have been 2,236 deaths; that’s a mortality rate of roughly 2.5%. If a 2.5% mortality rate sounds low, it’s not. That’s roughly comparable to the Spanish flu pandemic of 1919–20 that killed 50 million people by some estimates.

Coronavirus has reached pandemic proportions in China. Over 60 million people are locked down, which means they cannot leave their homes except once every three days to buy groceries. Streets are empty, stores are closed, trains and planes are not operating. The Chinese economy is slowly grinding to a halt. While the disease has been predominately centered in China, and Wuhan in particular, there have been significant outbreaks in Singapore (58 cases), Hong Kong (56 cases), Thailand (33 cases) and Japan (29 cases including one fatality). Approximately 218 cases have been identified among those trapped on cruise ships where all passengers are under quarantine. Fifteen cases have been identified in the United States. These statistics barely scratch the surface of what is happening with coronavirus in China. There is good reason to believe that the actual incidence of the virus may be five–10 times the official numbers. Tencent (a popular internet search and social media platform in China) reported on Feb. 1, 2020, that actual infections were 154,000 and deaths from the disease were 24,589. (A screenshot of the Tencent release is shown below; source: Taiwan News). The infection figure was approximately 10 times what the official figure was on the same date. The death toll was more than 300 times the official figure. Applying this death toll to total infections gives a fatality rate of 16%, which is over seven times the official fatality rate.

There is no reason for a high-profile platform such as Tencent either to fabricate data or incite panic. It is reasonable to conclude that these figures are close to actual data. The Tencent posting was suppressed by the Chinese government within minutes of what may have been an accidental release of accurate data. The preeminent U.K. medical journal The Lancet also published an article on Jan. 31, 2020, using hard data (city populations, incidence of travel, estimated transmissibility, etc.) and a reliable SEIR model (susceptible, exposed, infected, resistant). That article estimated total infections of 75,815 in Wuhan as of Jan. 25. That figure is 17 times the official figure of 4,400 available on Jan. 27. The multiple of the estimate by The Lancet to the official figure is roughly in line with the multiple of the Tencent release to official data five days later. Using either The Lancet or Tencent as a baseline suggests that the official infection and death rates are grossly understated. Anecdotal evidence is consistent with the view that official data are materially understated. Many bodies have been picked up off the streets and sent for cremation without blood samples or autopsies. It is highly likely that these victims died from coronavirus but are not included in official counts because no tests were performed. Authorities are running out of body bags and refrigerated trucks, so bodies are simply being wrapped in plastic sheets and hauled away in ordinary vans. A shortage of face masks, latex gloves and testing kits has also emerged. This means that doctors and medical personnel are highly susceptible to infection. It also means that patients who complain of fever and difficulty breathing are sent away because officials have no way to test them for coronavirus. These developments simultaneously inflate the number of infected and deflate the official count. The story gets worse. Wuhan, the city that is ground zero for coronavirus infections, is also the location of the sole bioweapons laboratory for the Chinese military and Chinese Communist Party. One of the scientists at the laboratory is Zhengli Shi, a virologist. Shi formerly worked at a laboratory at the University of North Carolina, where he engineered a hypervirulent bat-based coronavirus that bears a striking resemblance to the COVID-19 coronavirus, including gene sequences not found in nature. These linkages at least suggest that the outbreak of the coronavirus in Wuhan may be linked to an accidental release of the virus from the biological weapons laboratory located there. If this thesis is correct, the coronavirus may be difficult to contain with vaccines or drug therapies since it would have been engineered to be highly resistant to such treatments. What impact will the coronavirus pandemic have on the Chinese economy and global supply chains, especially in the technology sector? Right now my models are telling me that the impact of coronavirus on the Chinese economy is orders of magnitude greater than most analysts estimate. In fact, the Chinese economy, second largest in the world, may be grinding to a halt. The following excerpt from an article by Ambrose Evans-Pritchard in The Telegraph on Feb. 12, 2020, tells the tale:

This article contains valuable vignettes of what is happening in China, but they barely scratch the surface. An even bigger story is the extent to which the disruption in China from coronavirus is not only slowing the Chinese economy but is also disrupting global supply chains and slowing output around the world.

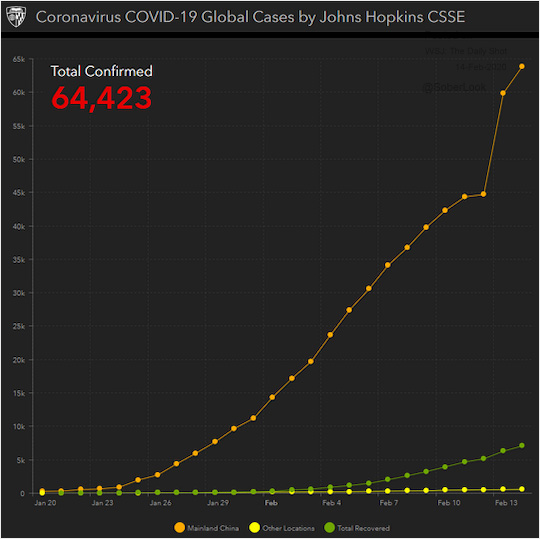

This chart prepared by the Johns Hopkins University based on official data provided by China and other nations shows the total number of confirmed cases of coronavirus infection as of Feb. 14, 2020 (orange line). Wall Street was encouraged by a prior update that showed 44,700 confirmed cases. Then cases increased by over 15,000 in a single update. The resulting near-vertical slope of the graph blew up Wall Street wishful thinking and triggered a downdraft in stock markets worldwide. As of Feb. 15, confirmed cases had increased to 64,447. The pandemic is far from under control and spreading quickly. Production shutdowns in China are reducing exports of high-tech inputs from South Korea, Japan and Germany. Likewise, the extreme reductions in exports from China (due to plant closures) are hurting sales by European and U.S. distributors and retail outlets. Independent of production and sales bottlenecks, there are massive transportation bottlenecks as vessels and crews are quarantined or refuse to enter Chinese ports at all. The tech sector may be the hardest hit of all. In addition to coronavirus disruption, the U.S. Department of Justice last week indicted China’s largest telecommunications device and network provider, Huawei, on racketeering charges. The Pentagon also reversed a prior determination and agreed that the Commerce Department can put Huawei on an export control list, which prohibits sales of processors and other high-tech components to Huawei by U.S. firms. These measures are certain to invite retaliation by China against U.S. firms in the tech supply chain. This story isn’t going away anytime soon. Regards, Jim Rickards

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)