Send this article to a friend:

February

18

2020

|

Send this article to a friend: February |

|

Q4 Earnings Shocker: Excluding The FAAMGs, Net Income Is Down 7.5%

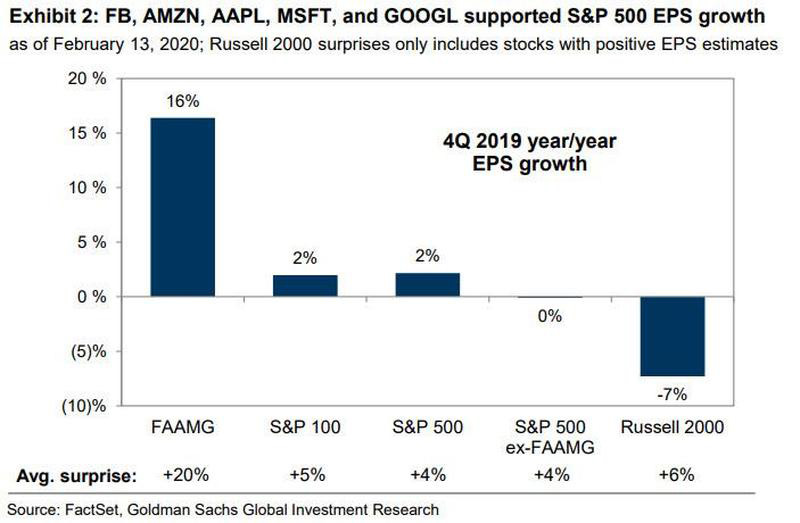

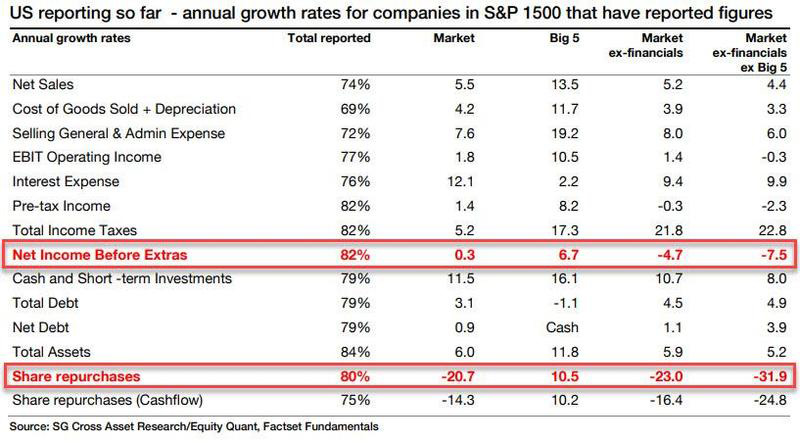

One day later, on Monday morning, SocGen's Andrew Lapthorne has further refined Goldman's analysis, and come up with an even more jarring conclusion on corporate profitability, one which avoids the impact of buybacks on artificially inflating EPS by simply looking at Net Income. What he founds is that "despite strong markets last year, net income barely moved, with a rise of just 0.3%. More worrying is without the Big 5 companies (Microsoft, Alphabet, Apple, Amazon and Facebook), net income fell 7.5%", which further underscores our recent discussion of how bifurcated the market is becoming between the handful of mega-caps, i.e., the "other 1%", and the "other" 495 companies in the S&P.

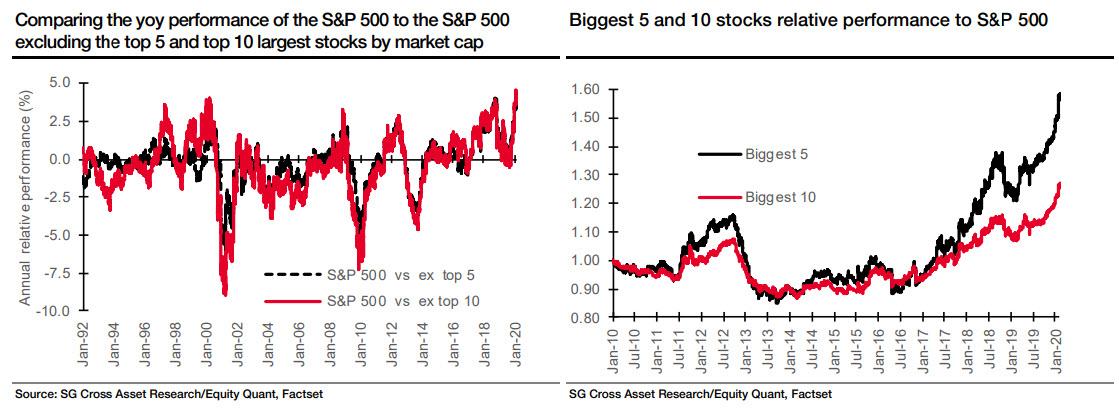

What is behind this disappointing result for virtually all publicly traded companies with the exception of a handful of mega techs? According to Lapthorne, "this is due to higher costs (SG&A) and a significant rise in both interest expense and taxes" with the SocGen strategist noting "that interest costs are rising so quickly despite low interest rates is remarkable and a challenge to policymakers." His bottom line is a carbon copy replica of what we have said on countless prior occasions, namely that "with all this debt, higher interest rates seem no longer feasible", something which even the Fed has now figured out. There were other issues as well: first, looking at the leverage front, asset growth rose marginally quicker than Net Debt, so debt-to-asset ratios declined but, at the same time, EBIT hardly grew, and again this problem is accentuated once the Big 5 are excluded. But the headline-grabbing figure is share buybacks. We measure buybacks both from the declared amount repurchased to the repurchase figure from the cashflow statement. As Lapthorne explains, "typically, the former is bigger than the latter. With 80% of the overall value of buybacks reported so far, buybacks are 20% lower in 2019 than 2018 - excluding the Big 5, the figure is down 32%" , which incidentally is exactly what we warned about a month ago when we showed that virtually every investor class - from institutions, to retail, to systematics (risk parity/CTA/vol targeting) are all in - and yet buybacks are tumbling. Yet not everyone is cutting back on buybacks: that the Big 5 continue to buy back - with a 10.5% increase in buybacks compared to the 32% decrease for everyone else - "no doubt helps explain the performance divergence" which Lapthorne demonstrated last week, when he showed that the top 5 (and 10) largest companies are now outperforming the broader market by the widest margin on record.

And now we know why.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)