Send this article to a friend:

February

02

2019

|

Send this article to a friend: February |

|

Recession Lessons Not Learned as Leveraged Loan Risk Soars Again

But it looks like those lessons were ignored, and history may naively repeat itself. This time, the alarms are sounding because of $1 trillion in the corporate leverage loan market, according to Tiana Lowe at Washington Examiner:

While there isn’t a precise criteria for these loans, according to Investopedia they are defined for both corporations and individuals as:

Even more alarming, investors in this type of loan appear to be unloading their investments in droves. This is in part because of fears driven by two reasons highlighted in a CNBC piece (text separation ours):

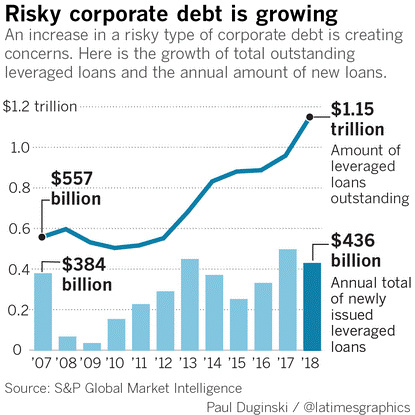

And over at the Los Angeles Times, a recent report contained a chart that confirms the growing amount of risky corporate debt, including leveraged loans:

What’s telling from the chart above are the $557 billion of outstanding loans in 2007 compared to the $1.15 trillion now. If all this high-risk corporate loan activity has a familiar “feel” to the subprime mortgage loans made to individuals in 2008, you would be right. 2008 Subprime Mortgage Crash and 2019 Corporate “Junk” The years leading up to the 2008-09 recession were loaded with “simple interest” loans made to people in the subprime market. But when that credit bubble burst, it set off a firestorm that led to bail outs, new financial policy and panic. A Los Angeles Times article drew an interesting similarity between the recession and investors leaving the leveraged loans market:

Except this time, the borrowers aren’t individuals with $250,000 mortgages though. According to the same Los Angeles Timespiece, it’s corporations like Uber and Burger King taking out leveraged loans and taking on millions in debt load. Debt load that can crush a company and force it into bankruptcy. Another CNBC article analyzed the debt load, while highlighting the similarity between the 2008 recession and what’s happening now:

Former Federal Reserve Chair Janet Yellen was quoted in that article voicing concerns of her own about how “weak” the debt underwriting was:

This “weakly” underwritten debt has to be paid at some point. When the tab is due, if interest rates rise at any point in 2019, that could certainly prolong a headache, and there’s already a good possibility that two rate hikes are coming. If a recession hits this year, debt load like this could potentially cause bankruptcies to soar, and make the recession last much longer. This type of debt already claimed Toys R’ Us as a victim of bankruptcy. Not good, and certainly not the sign of a “strong economy.” Don’t Let the Next Recession Leverage Your Retirement All it’s going to take for trouble to arise is inflation to rise out of control and reduce the ability for these corporations to pay back their debt, and there is quite a big tab to pay. Plus, the Fed isn’t giving a clear signal as to whether or not it will continue to hike rates this year. So it looks as though the market may be propped up by companies that are in massive amounts of “junk” debt. That, and the recent recession showed us that housing market optimism was pushed until it was too late. Lessons from that period sure don’t seem like they were learned. After 8 long years of ultra-loose monetary policy from the Federal Reserve, it’s no secret that inflation is primed to soar. If your IRA or 401(k) is exposed to this threat, it’s critical to act now! That’s why thousands of Americans are moving their retirement into a Gold IRA. Learn how you can too with a free info kit on gold from Birch Gold Group. It reveals the little-known IRS Tax Law to move your IRA or 401(k) into gold. Click here to get your free Info Kit on Gold.

|

Send this article to a friend:

|

|

|

There are lessons from the 2008-09 recession that the banking industry should have taken note of to prevent egregious lending errors from happening again.

There are lessons from the 2008-09 recession that the banking industry should have taken note of to prevent egregious lending errors from happening again.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)