Send this article to a friend:

February

14

2019

|

Send this article to a friend: February |

|

Fed Warns Dollar "Might Not Retain Its Dominance Forever"

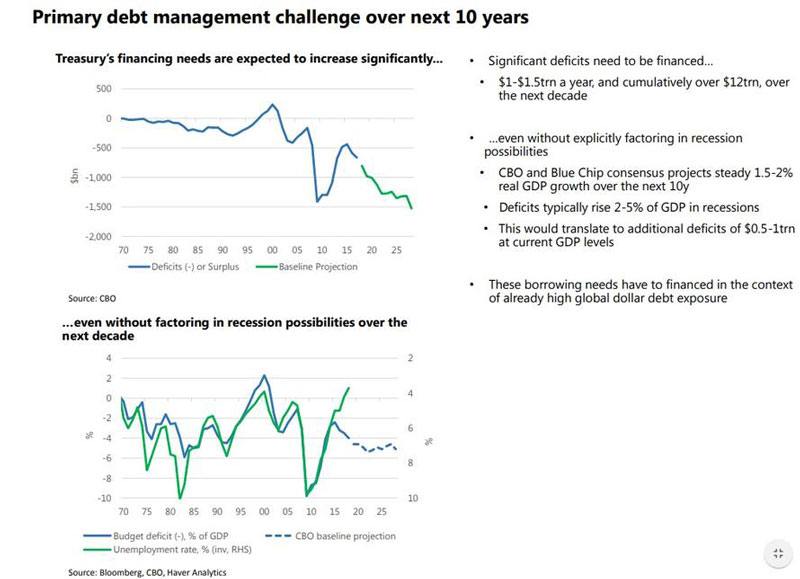

Here, among other things (which potentially include the Green New Deal, with its $6+ trillion cost) the TBAC cautioned that the Treasury’s financing needs are expected to increase significantly even without factoring in recession possibilities over the next decade. The TBAC warned that deficits to the tune of $1-$1.5trn a year, and cumulatively over $12trn, over the next decade, are coming and will have to be funded in the bond market. Meanwhile, the CBO stubbornly refuses to forecast a recession during the next decade, instead projecting a steady 1.5-2% real GDP growth over the next 10y. While the TBAC did not take a position on this laughable assumption, it warned that deficits typically rise 2-5% of GDP in recessions, which would translate to additional deficits of $0.5-1trn at current GDP levels, and warns that "these borrowing needs have to financed in the context of already high global dollar debt exposure."

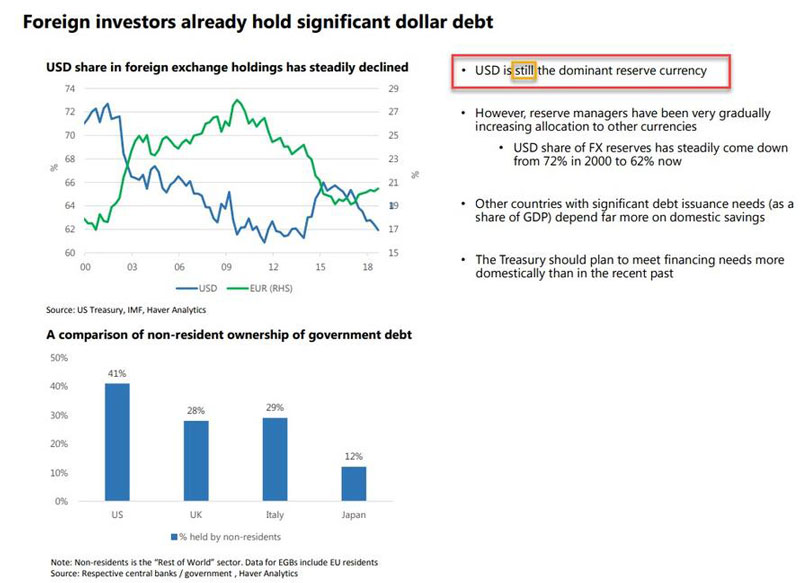

But the bigger problem is that in the context of soaring deficit funding needs, the TBAC is also increasingly worried that "foreign investors already hold significant dollar debt" which is why the US will have to increasingly rely on domestic savings to fund its future budget deficits. And here the TBAC made a surprising, tongue-in-cheek observation, namely that reserve managers have been very gradually increasing allocation to other currencies, and that the USD share of FX reserves has steadily come down from 72% in 2000 to 62% now even though the "USD is still the dominant reserve currency." Still. As in for the foreseeable future, but not that much longer.

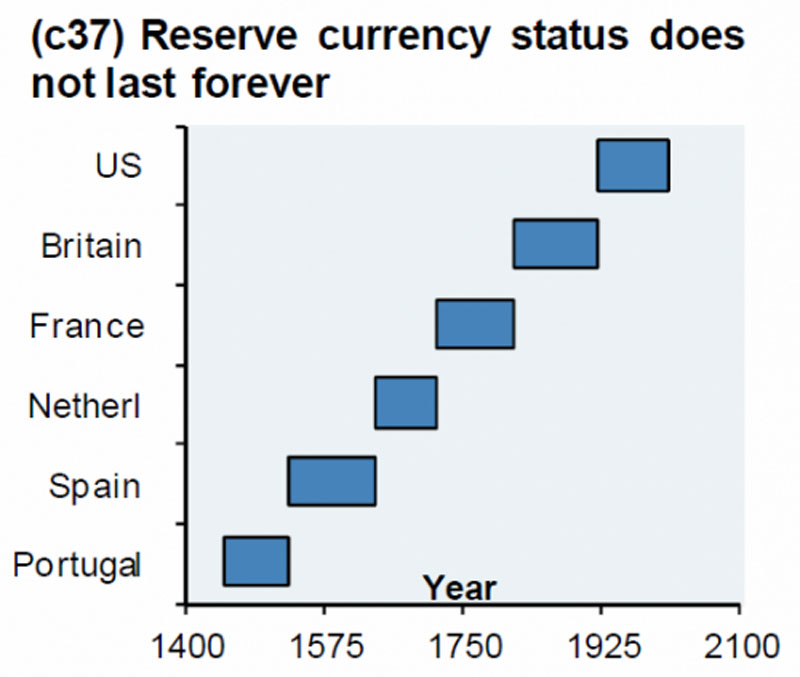

Needless to say commenting (or joking) even sarcastically about the reserve status of the dollar, is generally frowned upon in very polite company because if enough people start "joking" about it, it just might become a self-fulfilling prophecy. It won't be the first time, just ask any of the countries below which all enjoyed reserve currency status for decades... and could print their way out of all trouble until one day, poof: "it's gone."

We bring up all of this again, because yesterday in a blog post on the NY Fed "Liberty Street Economics" website, the researchers of the US central bank doubled-down on the snyde observations made by the TBAC when they "addressed the potential implications for the United States if the dollar’s global role changed" and we quote, noted that "the currency might not retain its dominance forever." But why now? Because just like Mnuchin's calls to banks to comfort the public that they have sufficient liquidity sparked questions why is Mnuchin suddenly concerned about bank liquidity, so the recent focus on the viability of the dollar's reserve status, first by the Treasury Department's smartest Wall Street advisors, and now - by the Federal Reserve itself - is... a little troubling. In any case, this is how the authors set the stage:

So nothing to worry about? Well, not really. First, the good news: as the blog writes, since the global financial crisis, "central banks have accumulated official reserves more extensively to self-insure against dollar-funding market disruptions."

Some more good news: the dominant role of the dollar as a unit of exchange and as a transactions and settlement currency is illustrated by its continued broad use in 88 percent of foreign exchange transaction volumes and at least 40 percent of the invoicing of imports of countries other than the United States. Sixty-two percent of international debt securities issuance, 49 percent of all debt securities issuance, and 48 percent of all cross-border bank claims are dollar-based. Roughly half of the $1.6 trillion of dollar banknotes in circulation are held overseas, fluctuating with economic and political uncertainty in foreign countries. In payments systems, roughly half of the $5 trillion of transactions settled daily through the CLS system are denominated in dollars, according to 2018:H1 data. So far so good: and yet some clouds are forming on the horizon, as the following observation details:

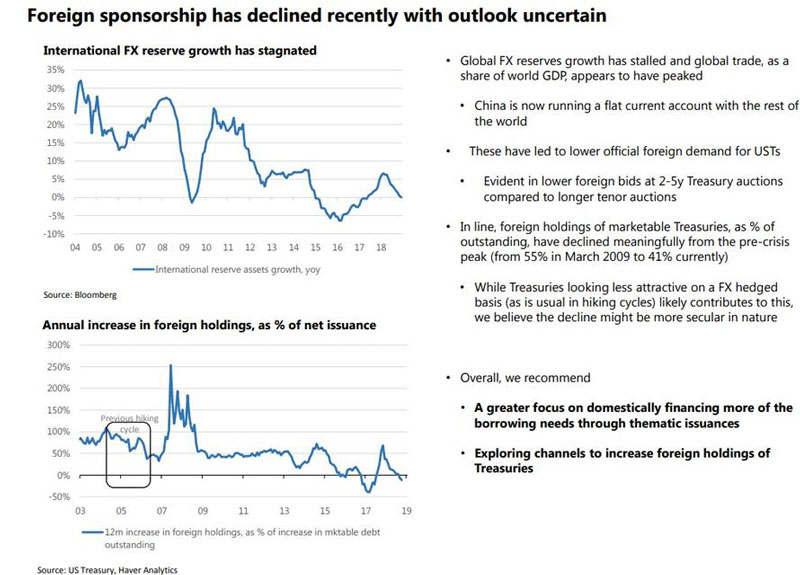

This brings us back to an observations made by the TBAC at the end of January, according to which global FX reserves growth has stalled and global trade, as a share of world GDP, appears to have peaked, while China is now running a flat current account with the rest of the world, something we discussed extensively in "A Tectonic Shift In China's Economy Has Largely Gone Unnoticed By Investors." As a result of these transformations, there has been an even lower official foreign demand for USTs, which has been evident in lower foreign bids at 2-5y Treasury auctions compared to longer tenor auctions. Furthermore, foreign holdings of marketable Treasuries, as % of outstanding, have declined meaningfully from the pre-crisis peak (from 55% in March 2009 to 41% currently) And while the TBAC admits that Treasuries look far less attractive on a FX hedged basis, something we also discussed recently, which is likely contributing to this decline in foreign demand, the TBAC believes "the decline might be more secular in nature."

In its conclusion, the NY Fed econ team tries to take the TBAC's somewhat alarmist conclusion and nuance it, noting that "while the dollar’s international status may have declined in some pockets, overall it remains dominant." Nevertheless, it concedes that "recent trends bear watching" warning that "as history suggests a currency’s dominant status is not immutable" and just in case repeating its warning that "the [US Dollar] might not retain its dominance forever." Sadly the Fed did not specify just what actions taken by, well, It would be necessary and sufficient to finally end the dollar's exorbitant privilege, after which any and all discussions about Magic Money Tree theories or who would fund various Green New Deals would promptly end as the "Venezuela alternative" would be all too clear.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)