Send this article to a friend:

February

10

2018

|

Send this article to a friend: February |

|

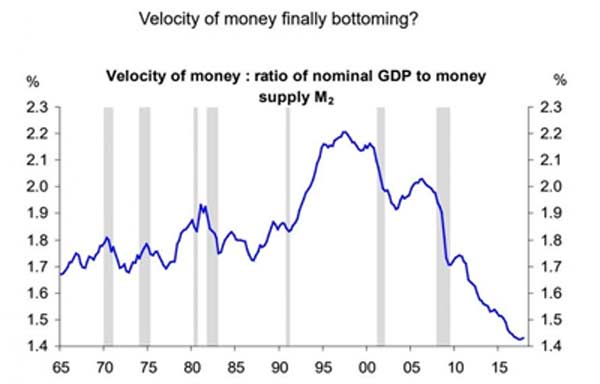

The Spark That Lights the Wick: Velocity of Money to Ignite Inflation

The velocity of money measures the turnover of dollars, how often they are spent, and then spent again by their recipients, over a certain period of time. It has been falling, more or less on a line, since 2008. It now appears that the velocity of money has finally bottomed, and is, in fact rebounding. And, in couldn't come at a worse time: with Trump dumping trillions into the economy to stimulate it further, the Fed is now painfully behind the curve, which means that chair Powell will find himself rushing to hike rates at virtually every opportunity to avoid getting Volckered. Over the past decade we have shown this chart on numerous occasions and usually in the context of failed Fed policy. After all, based on the fundamental MV = PQ equation, it is virtually impossible to generate inflation (P) as long as the velocity of money (V) is declining.

The Fed would like you to believe that the reason we haven’t seen a proportional surge in either GDP or inflation during that time is that people were so aggressively saving this money. That is provable nonsense. The US savings rate is near all-time lows. The truth, as oft stated here, is that all this printing press money was used to buy risk assets, stocks, and inflate that bubble. And that money has stayed there until now. That’s been some of the lowest velocity money around. None other than the St. Louis Fed discussed this in a report back in 2014:

The regional Fed went on to note that during the first and second quarters of 2014, the velocity of the monetary base was at 4.4, its slowest pace on record. "This means that every dollar in the monetary base was spent only 4.4 times in the economy during the past year, down from 17.2 just prior to the recession. This implies that the unprecedented monetary base increase driven by the Fed’s large money injections through its large-scale asset purchase programs has failed to cause at least a one-for-one proportional increase in nominal GDP. Thus, it is precisely the sharp decline in velocity that has offset the sharp increase in money supply, leading to the almost no change in nominal GDP (either P or Q)." So why did the unprecedented monetary base increase created by years of QE not cause a proportionate increase in either the general price level or GDP? The answer, according to the Fed at least, was in the private sector’s "dramatic increase in their willingness to hoard money instead of spend it. Such an unprecedented increase in money demand has slowed down the velocity of money, as the figure below shows." In light of the recent collapse in the US savings rate to just shy of record lows, that explanation makes zero sense, and what the St. Louis Fed meant to say is that of spending (or saving) freshly created money was immediately invested into risk-assets, almost exclusively by members of the 1% who were "closest to the money”. This explains why there was almost a 1:1 correlation between the increase in the Fed's balance sheet and the S&P for years. In any case, for whatever reason, after declining for nearly a decade, the Fed's greatest wish after all these years appears to have been granted, amd it now appears that the velocity of money has finally bottomed, and is, in fact rebounding. And, in couldn't come at a worse time: with Trump dumping trillions into the economy to stimulate it further, the Fed is now painfully behind the curve, which means that chair Powell will find himself rushing to hike rates at virtually every opportunity to avoid getting Volckered. It may be too late, however: since directional changes to the velocity of money take place at a glacial pace, the chart above from Deutsche Bank suggests that the Fed should have started its tightening cycle long ago. Still, the jury is still out on just how badly inflation will overshoot once money "spills" out of capital markets and into the broader economy, and how many rate hikes the Fed is "behind". One thing that is certain, however, is that as we find out the answers, for risk assets and active managers, all of whom recently listed rising rates and inflation as the biggest risk factor...

|

Send this article to a friend:

|

|

|

Forget the Trump tax cuts, the Senate budget deal, the Fed's Quantitative Tightening and the collapse in foreign buying of US Treasuries: after years of dormancy, the biggest catalyst for a sharp inflationary spike has finally emerged, and it is none of the above. Behold: the velocity of money.

Forget the Trump tax cuts, the Senate budget deal, the Fed's Quantitative Tightening and the collapse in foreign buying of US Treasuries: after years of dormancy, the biggest catalyst for a sharp inflationary spike has finally emerged, and it is none of the above. Behold: the velocity of money.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)