Send this article to a friend:

January

12

2023

|

Send this article to a friend: January |

|

Schiff: Is "Cooling" CPI Setting The Stage For More Inflation?

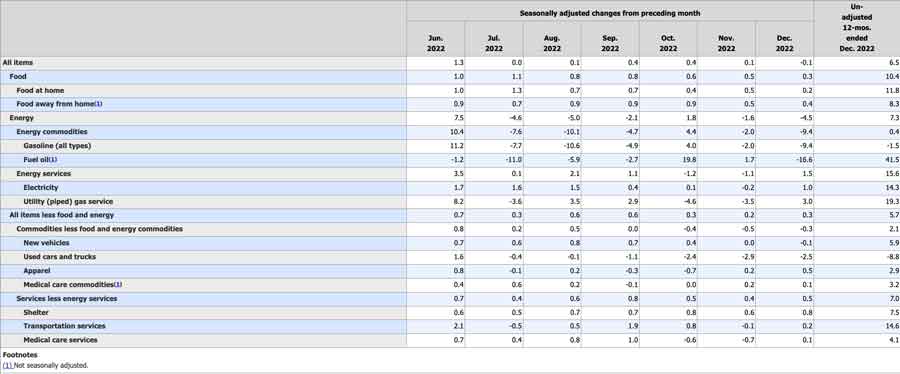

And a deeper look at the data reveals that a lot of inflationary pressure remains despite the optimistic headlines. The Consumer Price Index (CPI) came in at 6.5%, down from 7.1% in November, according to the latest data from the Bureau of Labor Statistics. That was right on the consensus projection. On a monthly basis, CPI ticked down -0.1%. The consensus was for monthly CPI to be unchanged. If you take the headline numbers in isolation, it appears that price inflation has cooled off, but digging deeper into the data reveals that falling energy prices papered over the fact that most other prices continued their relentless climb. Core CPI — excluding more volatile food and energy prices was up 0.3% month-on-month. That was a bigger increase than November’s 0.2% rise. On an annual basis, Core CPI was 5.7%, down from 6% in November. Keep in mind, inflation is worse than the government data suggest. This CPI uses a formula that understates the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. A Deeper Look at the Data Falling gasoline and energy prices were the biggest contributor to the overall decline in prices and skewed the overall numbers lower. Most other categories continued to chart price increases last month. The energy price index plunged by -4.5% on a monthly basis with gasoline prices down -9.4% and fuel oil cratering by -16.6%. But food prices continue to climb relentlessly. Overall, food prices rose by another 0.3% on a monthly basis. Year on year, food prices have risen by 10.4% according to the BLS data. Shelter costs were up another 0.8% month on month.

Peter Schiff summed up the CPI data in a tweet. Market Perception Nevertheless, the markets view this as a sign that inflation is cooling and it is buoying hope that the Federal Reserve will further slow monetary tightening. Stock futures were already rallying ahead of the CPI data release. In the 30 minutes after the data came out, gold rallied and briefly pushed through the $1,900 an ounce level. Before the data came out, Reuters reported that the CPI would “have a big impact on markets by shaping expectations of the speed of interest rate hikes in the world’s biggest economy. Markets have priced better-than-even odds that the Federal Reserve raises rates by 25 basis points, rather than 50, at February’s meeting.” But the markets seem to be missing the fact that any slowdown in Federal Reserve monetary tightening will almost certainly set the stage for bigger price increases down the road. Simply put, an end to the war on inflation means more price inflation. And as Schiff pointed out, inflation is far from beaten. CPI remains more than three times the Fed’s 2% target. Nevertheless, the narrative is that inflation has peaked. As Peter Schiff explained in a podcast, most people are still clueless about what is going on. This lull in rising prices is likely temporary.

How Will the Fed Play It? Absent a crisis in the economy, the Fed will likely keep pressing its war on inflation. But when the central bank does go back to rate cuts and ends balance sheet reduction, that means a return to accommodative monetary policy and money creation. Money creation is inflation. Price inflation is a symptom of monetary inflation. In effect, the markets are begging for a return to inflation because they think the Fed has beaten inflation. It is reasonable to think that the CPI will continue to cool in the next several months. The math works in its favor. We have big month-on-month increases from 2021 rolling out of the annual average. That pushes the yearly increase lower. Meanwhile, the economy is slowing. Make no mistake, high interest rates are subduing economic activity. An economy built on easy money and credit can’t function in this high interest rate environment. Two things need to happen in order to beat inflation. We need positive real interest rates — an interest rate above the CPI. And we also need the US government to cut spending and stop running huge budget deficits. A Fed paper admitted that it can’t tame inflation with monetary policy alone, saying, “When the fiscal authority [the federal government] is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt.” Neither of these things will likely happen. That means the Fed can’t possibly win this war. It might be able to brag about “progress,” but it is doomed to fail. Meanwhile, the bigger problem is that while this “high” interest rate environment isn’t high enough to truly tame inflation, it is high enough to break something in the economy. When that happens, the Fed’s back will really be up against the wall. It will have to choose between a deep, long recession or high inflation. I think it’s just a matter of time before something breaks in this debt-riddled, bubble economy. When that happens, the Fed will likely shift from a soft pivot to a hard pivot. To use a favorite Fed term, any cooling of the CPI is likely to be “transitory.”

Michael Maharrey is the managing editor of the SchiffGold blog, and the host of the Friday Gold Wrap Podcast and It's Your Dime interview series.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)