With growing complexity, such as greater mechanization of processes and supply lines that extend around the world.

All three of these approaches are reaching limits. The empty shelves some of us have been seeing recently are testimony to the fact that complexity is reaching a limit. And the growth in debt looks increasingly like a bubble that can easily be popped, perhaps by rising interest rates.

In my view, the first item listed is critical at this time: Is the supply of cheap-to-produce energy products growing fast enough to keep the world economy operating and the debt bubble inflated? My analysis suggests that it is not. There are two parts to this problem:

[a] The cost of producing fossil fuels and delivering them to where they are needed is rising rapidly because of the effects of depletion. This higher cost cannot be passed on to customers, without causing recession. Politicians will act to keep prices low for the benefit of consumers. Ultimately, these low prices will lead to falling production because of inadequate reinvestment to offset depletion.

[b] Non-fossil fuel energy products are not living up to the expectations of their developers. They are not available when they are needed, where they are needed, at a low enough cost for customers. Electricity prices don’t rise high enough to cover their true cost of production. Subsidies for wind and solar tend to drive nuclear electricity out of business, leaving an electricity situation that is worse, rather than better. Rolling blackouts can be expected to become an increasing problem.

In this post, I will explore the energy-related issues that are contributing to the recessionary trends that the world economy is facing, starting later in 2022.

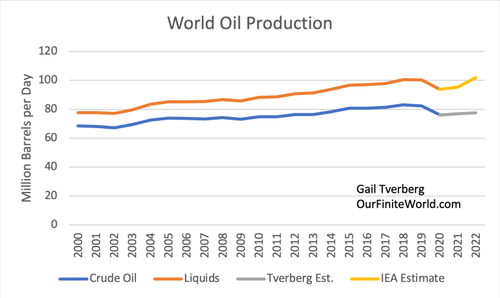

[1] World oil supplies are unlikely to rise very rapidly in 2022 because of depletion and inadequate reinvestment. Even if oil prices rise higher in the first part of 2022, this action cannot offset years of underinvestment.

Figure 1. Crude oil and liquids production quantities through 2020 based on EIA data. “IEA Estimate” adds IEA indicated increases in 2021 and 2022 to historical EIA liquids estimates. Tverberg Estimate relate to crude oil production.

The IEA, in its Oil Market Report, December 2021, forecasts a 6.4-million-barrel increase in world oil production in 2022 over 2021. Indications through September of 2021 strongly suggest that there was only a small rebound (about 1 million bpd) in the world’s oil production in 2021 compared to 2020. In my view, IEA’s view that liquids production will increase by a huge 6.4 million barrels a day between 2021 and 2022 defies common sense.

The basic reason why oil production is low is because oil prices have been too low for producers since about 2012. Companies have had to cut back on developing new fields in higher cost areas because oil prices have not been high enough to justify such investments. For example, producers from shale formations could add new wells outside the rapidly depleting “core” regions if the oil price were much higher, perhaps $120 to $150 per barrel. But US WTI oil prices averaged only $57 per barrel in 2019, $39 per barrel in 2020, and $68 per barrel in 2021, so this new investment has not been started.

Recently, oil prices have been over $80 per barrel, but even this is considered too high by politicians. For example, countries are releasing oil from their strategic oil reserves to try to force oil prices down. The reason why politicians are interested in low oil prices is because if the price of oil rises, both the price of food and the cost of commuting are likely to rise, since oil is used in farming and in commuting. Inflation is likely to become a problem, making citizens unhappy. Wages will go less far, and politicians who allow high oil prices will be voted out of office.

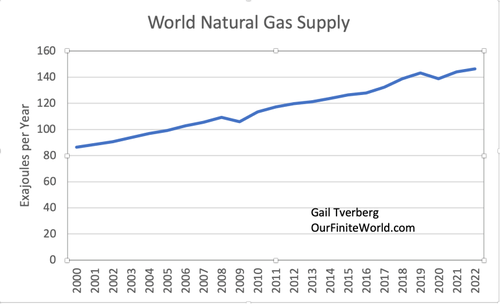

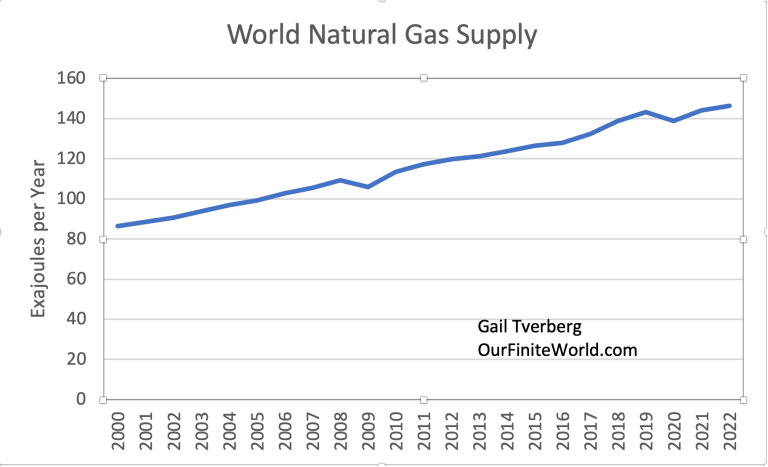

[2] Natural gas production can be expected to rise by 1.6% in 2022, but this small increase will not be enough to meet the needs of the world economy.

Figure 2. Natural gas production though 2020 based on data from BP’s 2021 Statistical Review of World Energy. For 2020 and 2021, Tverberg estimates reflect increases similar to IEA indications, so only one indication is shown.

With natural gas production growing at a little less than 2% per year, a major issue is that there is not enough natural gas to “go around.”Natural gas is the smallest of the fossil fuels in quantity. We are depending on its growth to solve many problems, simultaneously:

- To increase natural gas imports for countries whose own production is declining

- To provide quick relief from inadequate production by wind turbines and solar panels, whenever such relief is needed

- To offset declining coal consumption related to a combination of issues (depletion, high pollution, climate change concerns)

- To help increase world electricity supply, as transportation and other processes are gradually electrified

Furthermore, the rate at which natural gas supply increases cannot easily be speeded up because (a) the development of new fields, (b) the development of transportation structures (pipeline or Liquefied Natural Gas (LNG) ships), and (c) the development of storage facilities all require major upfront expenditures. All of these must be planned years in advance. They require huge amounts of resources of many kinds. The selling price of natural gas must be high enough to cover all of the resource and labor costs. For those familiar with the concept of Energy Returned on Energy Invested (EROEI), the basic problem is that the delivered EROEI falls too low when all of the many parts of the system are considered.

Storage is extremely important for natural gas because fluctuations tend to occur in the quantity of natural gas the overall system requires. For example, if stored natural gas is available, it can be used when wind turbines are not producing enough electricity. Also, a huge amount of energy is needed in winter to keep homes warm and to keep the lights on. If sufficient natural gas can be stored for months at a time, it can help provide this additional energy.

As a gas, natural gas is difficult to store. In practice, underground caverns are used for storage, assuming caverns of the right type are available. Trying to build storage, if such caverns are not available, is almost certainly an expensive undertaking. In theory, importing natural gas by pipeline or LNG can transfer the storage problem to LNG producers. This is not a satisfactory solution, however. Without adequate storage available to sellers, this means that natural gas can be extracted for only part of the year and LNG ships can only be used for part of the year. As a result, return on investment is likely to be poor.

Now, in 2022, we are hitting the issue of very slowly rising natural gas production head-on in many parts of the world. Countries that import natural gas without long-term contracts are facing spiking prices. Countries in Europe and Asia are especially affected. The United States has mostly been isolated from the spiking prices thanks to producing its own natural gas. Also, only a small portion of the natural gas produced by the US is exported (9% in 2020).

The reason for the small export percentage is because shipping natural gas as LNG tends to be very expensive. Long-distance LNG shipping only makes economic sense if there is a several dollar (or more) price differential between the buyer’s price and the seller’s costs that can be used to cover the high transport costs.

We now seem to be reaching a period of spiking natural gas prices, especially for counties importing natural gas without long-term contracts. If natural gas prices rise, this will tend to make electricity prices rise because natural gas is often burned to produce electricity. Products made with high-priced electricity will be less competitive in a world market. Individual citizens will become unhappy with their high cost of heat and light.

High natural gas prices can have very adverse consequences. In areas with high prices, products made using natural gas as a raw material will tend to be squeezed out. One such product is urea, used as a nitrogen fertilizer. With less nitrogen fertilizer available, food production is likely to fall. If food prices rise in response to short supply, consumers will tend to reduce discretionary spending to ensure that there are sufficient funds for food. A reduction in discretionary spending is one way recession starts.

Inadequate growth in world natural gas production can be expected to hit poor countries especially hard. For example, a recent article mentions LNG suppliers backing out of planned deliveries of LNG to Pakistan, given the high prices available elsewhere. Another article indicates that Kosovo, a poor country in Europe, is experiencing rolling blackouts. Eventually, if natural gas available for export remains limited in supply, electricity blackouts can be expected to spread more widely, to less poor parts of Europe and around the world.

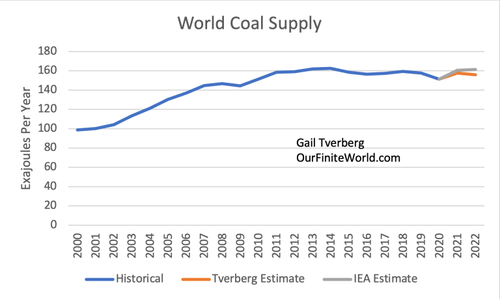

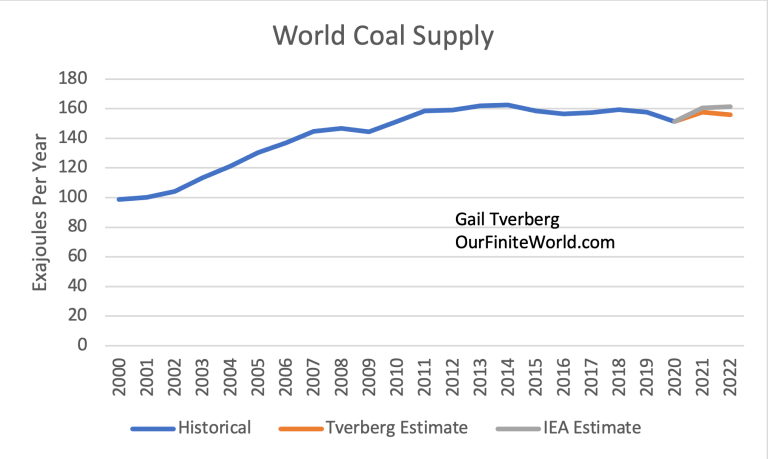

[3] World coal production can be expected to decline, further pushing the world economy toward recession.

Figure 3 shows my estimate for world coal production, next to a recent IEA forecast.

Figure 3. Coal production through 2020 based on data from BP’s 2021 Statistical Review of World Energy. “IEA Estimate” adds IEA indicated increases to historical BP coal quantities. Tverberg Estimate provides lower estimates for 2021 and 2022, considering depletion issues.

Figure 3 shows that world coal consumption has not been rising for about a decade.

Coal seems to be having the same problem with rising costs as oil. The cost of producing the coal is rising because of depletion, but citizens cannot afford to pay more for end products made with coal, such as electricity, steel and solar panels. Coal producers need higher prices to cover their higher costs, but it becomes increasingly difficult to pass these higher costs on to consumers. This is because politicians want to keep electricity prices low to keep their citizens and businesses happy.

If the cost of electricity rises, the cost of goods made with high-priced electricity will tend to rise. Businesses will find their sales falling in response to higher prices. In turn, they will tend to lay off workers. This is a recipe for recession, but a slightly different one than the ones mentioned earlier. It also is a good way for politicians not to get re-elected. As a result, politicians will try to hide rising coal costs from customers. For example, laws may be enacted capping electricity prices that can be charged to customers. Because of this, some electricity companies may be forced out of business.

The decrease in coal production I am showing for 2022 is only 1%, but when this small reduction is combined with the growth problems shown for coal and oil and the rising world population, it means that world coal supplies will be stretched.

China is the world’s largest coal producer and consumer. A major concern is that the country has serious coal depletion problems. It has experienced rolling blackouts since the fall of 2020. It has tried to encourage its own production by limiting coal imports, thus keeping wholesale coal prices high for local producers. It also limits the extent to which high coal costs can be passed on to electricity customers. As a result, the 2021 profits of electricity companies are expected to be reduced.

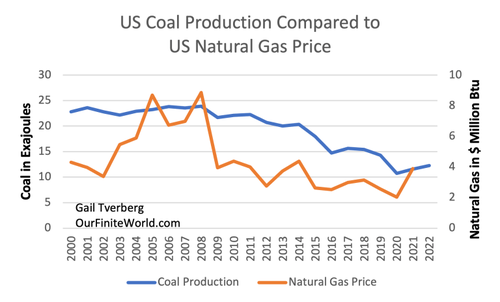

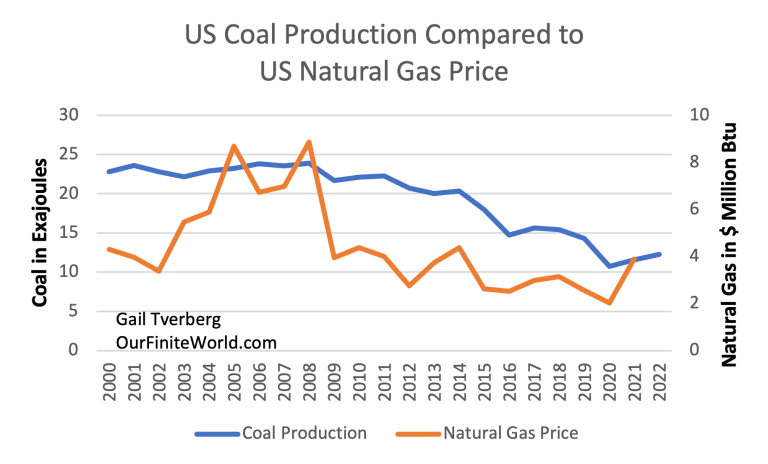

[4] The US may have some untapped coal resources that could be tapped, if there is a plan to ship more natural gas to Europe and other areas in need of the fuel.

The possibility of additional US coal production occurs because coal production in the US seems to have occurred because of competition from incredibly inexpensive natural gas (Figure 4). To some extent, this low natural gas price results from laws prohibiting oil and gas companies from “flaring” (burning off) natural gas that is too expensive to produce relative to the price it can be sold for. Prohibitions against flaring are a type of mandated subsidy of natural gas production by the oil-producing portion of “Oil & Gas” companies. This required subsidy leads to part of the need for high oil prices, especially for companies drilling in shale formations.

Figure 4. US coal production amounts through 2020 are from BP’s 2021 Statistical Review of World Energy. Amounts for 2021 and 2022 are estimated based on forecasts from EIA’s Short Term Energy Outlook. Natural gas prices are average annual Henry Hub spot prices per million Btus, based on EIA data.

A major reason why US coal extraction started to decline about 2009 is because a very large amount of shale gas production started becoming available then as a byproduct of oil production from shale. Oil producers were primarily interested in extracting oil because it (hopefully) sold for a high price. Natural gas was a byproduct whose collection was barely economic, given its low selling price. Also, the economy didn’t have uses, such as trucks powered by natural gas, for all of this extra natural gas production. Figure 4 suggests that wholesale natural gas prices dropped by close to half, in response to this extra supply.

With these low natural gas prices, as well as coal pollution concerns, a significant amount of US electricity production was switched from coal to natural gas. It is my view that this change left coal in the ground, potentially for later use. Thus, if natural gas prices rise again, US coal production could perhaps rise again. The catch, of course, is that many coal-fired electricity-generating plants in the US have been taken out of service. In addition, coal mines have been closed. Any increase in future coal production would likely take place very slowly because of the need for many simultaneous changes.

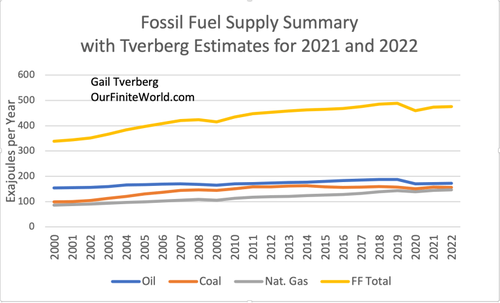

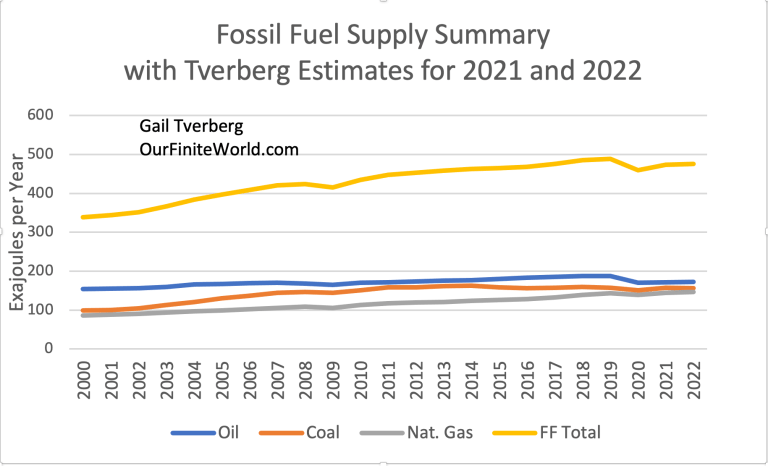

[5] On a combined basis, using Tverberg Estimates for 2021 and 2022, fossil fuel production in total takes a step down in 2020 and doesn’t rise much in 2021 and 2022.

Figure 5. Sum of Tverberg Estimates related to oil, coal, and natural gas. Oil includes natural gas liquids but not biofuels. Historical amounts are from BP’s 2021 Statistical Review of World Energy.

Figure 5 shows that on a combined basis, the overall energy being provided by fossil fuels is likely to remain lower in 2021 and 2022 than it was in 2018 and 2019. This is concerning, because the economy cannot go back to its 2019 level of “openness” and optional travel for sightseers, without a big step up in energy supply, especially for oil.

This same figure shows that the production of the three fossil fuels is somewhat similar in quantity: Oil is the highest, coal is second, and natural gas comes in third. However, oil shows a step down in 2020’s production from which it has not recovered. Coal shows a smoother pattern of rise and eventual fall. So far, natural gas has mostly been rising, but not very steeply in recent years.

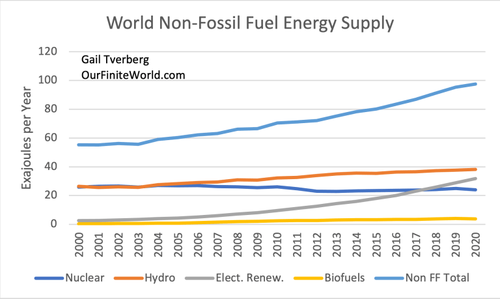

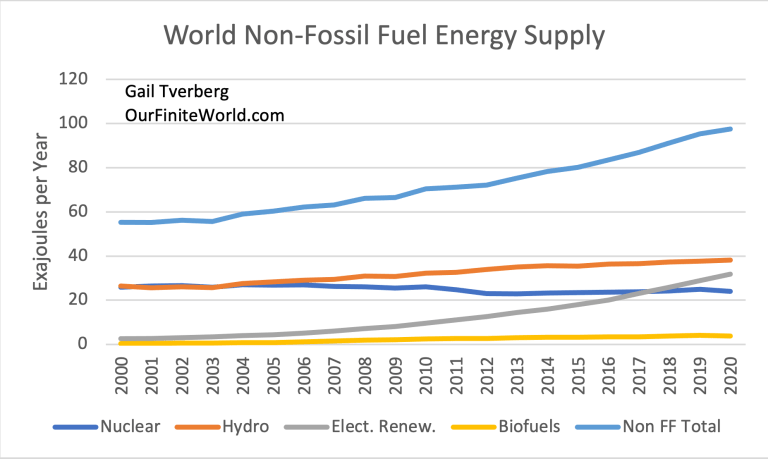

[6] Alternatives to fossil fuels are not living up to early expectations. Electricity from wind turbines and solar panels is not available when it is needed, requiring a great deal of back-up electricity generated by fossil fuels or nuclear. The total quantity of non-fossil fuel electricity is far too low. A transition now will simply lead to electricity blackouts and recession.

Figure 6 shows a summary of non-fossil fuel energy production for the years 2000 through 2020, without a projection to 2022. For clarification, wind and solar are part of the electrical renewables category.

Figure 6. World energy production for various categories, based on data from BP’s 2021 Statistical Review of World Energy.

Figure 6 shows that nuclear electricity production has been declining at the same time that the production of electrical renewables has been increasing. In fact, a significant decrease in nuclear electricity is planned in Europe in 2022. This reduction in nuclear electricity is part of what is causing the concern about electricity supply for Europe for 2022.

The addition of wind and solar to an electrical grid seems to encourage the closure of nuclear electricity plants, even if they have many years of safe production still ahead of them. This happens because wind and solar are given the subsidy of “going first,” if they happen to have electricity available. Wind and solar may also be subsidized in other ways.

The net result of this arrangement is that wholesale electricity prices set through competitive markets quite frequently fall too low for other electricity producers (apart from wind and solar). For example, wind and solar electricity that is produced during weekends may be unneeded because many businesses are closed. Electricity produced by wind and solar in the spring and fall may be unneeded because heating and cooling needs tend to be low at these times of the year. Wind and solar electricity providers are not asked to cut back supply because their production is unneeded; instead, low (or negative) prices encourage other electricity producers to cut back supply.

Nuclear electricity producers are particularly adversely affected by this pricing arrangement because they cannot save money by cutting back their output when wind and solar are over-producing electricity, relative to demand. This strange pricing arrangement leads to unacceptably low profits for many nuclear electricity providers. They may voluntarily choose to be closed. Local governments find that if they want to keep their nuclear electricity producers, they need to subsidize them.

Wind and solar, with their subsidies, tend to look more profitable to investors, even though they cannot support the economy without a substantial amount of supplementary electricity production from other electricity providers, which, perversely, they are driving out of business through their subsidized pricing structure.

The fact that wind and solar cannot be depended upon has become increasingly obvious in recent months, as coal, natural gas and electricity prices have spiked in Europe because of low wind production. In theory, coal and natural gas imports should make up the shortfall, at a reasonable price. But total volumes available for import have not been increasing in the quantities that consumers need them to increase. And, as mentioned above, nuclear electricity production is increasingly unavailable as well.

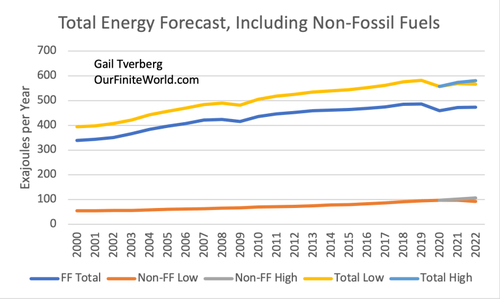

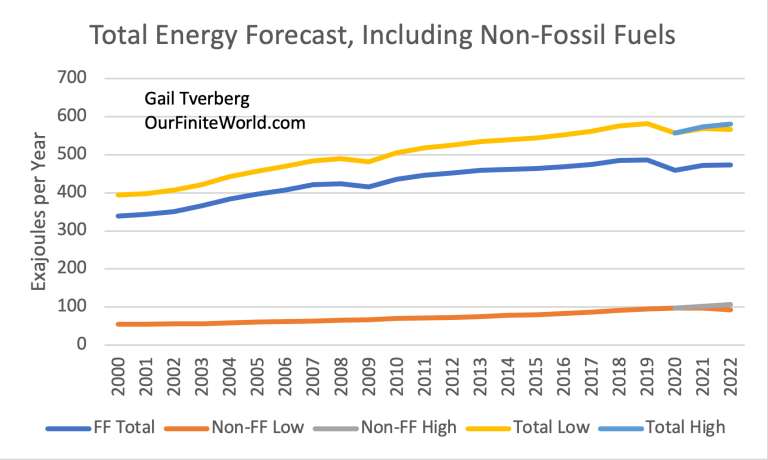

[7] The total quantity of non-fossil fuel energy supplies is not very large, relative to the quantity of fossil fuel energy. Even if these non-fossil fuel energy supplies increase at a trend rate similar to that in the recent past, they do not make up for the projected fossil fuel production deficit.

Figure 7. Total energy production, based on the fossil fuel estimates in Figure 5 together with non-fossil fuels in Figure 6.

With respect to anticipated future non-fossil fuel electricity generation, one issue is how much nuclear is being shut off. I would imagine these current closure schedules could change, if countries become aware that they may be facing rolling blackouts without nuclear.

A second issue is the growing awareness that renewables don’t really work as intended. Why add more if they don’t really work?

A third issue is new studies suggesting that prices being paid for locally generated electricity may be too generous. Based on such an analysis, California is proposing a major reduction to its payments for renewable-generated electricity, starting July 1, 2022. This type of change could reduce new installations of solar panels on homes in California. Other locations may decide to make similar changes.

I have shown two estimates of future non-fossil fuel energy supply in Figure 7. The high estimate reflects a 4.5% annual increase in the total supply, in line with recent past increases for the group in total. The lower one assumes that 2021 production is similar to that in 2020 (because of more nuclear being closed, for example). Production for 2022 represents a 5% decrease from 2021’s production.

Regardless of which assumption is made, growth in non-fossil fuel electricity supply is not very important in the overall total. The world economy is still mostly powered by fossil fuels. The share of non-fossil fuels relative to total energy ranges from 16% to 18% in 2020, based on my low and high estimates.

[8] The energy narrative we are being told is mostly the narrative that politicians would like us to believe, rather than the narrative that historians and physicists would develop.

Politicians would like us to believe that we live in a world of everlasting economic growth and that the only thing we should fear is climate change. They base their analyses on models by economists who seem to think that an “invisible hand” will fix all problems. The economy can always grow; enough fossil fuels and other resources will always be available. Governments seem to be able to print money; somehow, this money will be transformed into physical goods and services. With these assumptions, the only problems are distant ones that central banks and carbon taxes can handle.

The realists are historians and physicists. They tell us that a huge number of past economies have collapsed when their populations attempted to grow at the same time that their resource bases were depleting. These realists tell us that there is a high probability that our current economy will eventually collapse, as well.

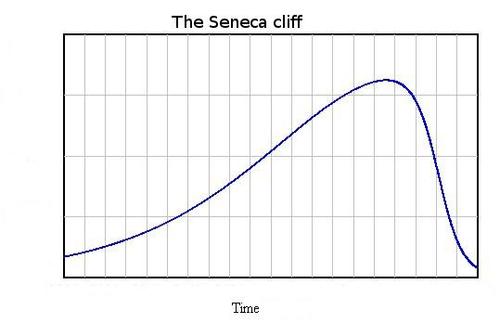

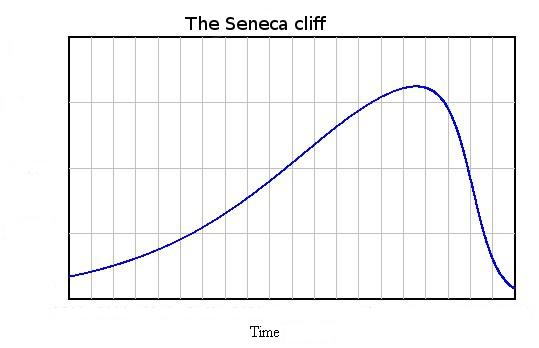

Figure 8. The Seneca Cliff by Ugo Bardi

The general shape that economic growth is likely to take is that of a “Seneca Curve” or “Seneca Cliff.” In the words of Lucius Annaeus Seneca in the first century CE, “Increases are of sluggish growth, but the way to ruin is rapid.” If we think of the amount graphed as the total quantity of goods and services received by citizens, the amount tends to rise slowly, gradually plateaus and then falls.

We now seem to be encountering lower energy supply while population continues to rise. It takes energy for any activity that we think of as contributing to GDP to occur. We should not be surprised if we are at the edge of a recession. If we cannot get our energy problems solved, the downturn could be very long-lasting.

The author of Our Finite World is Gail Tverberg. She is a researcher focused on figuring out how energy limits and the economy are really interconnected, and what this means for our future. Her background is as a casualty actuary, working in insurance forecasting.

The author of Our Finite World is Gail Tverberg. She is a researcher focused on figuring out how energy limits and the economy are really interconnected, and what this means for our future. Her background is as a casualty actuary, working in insurance forecasting.

Gail Tverberg, Charles Hall, Mario Giampietro, and Joseph Tainter in auditorium in Barcelona, Spain. They would later answer questions from students from 11 high schools in the area. Translation from Catalan to English was provided by headphone.

Gail first became aware of oil shortages, and the impact they could have on insurance companies, back in the 1973 – 1974 period, when oil limits were first a problem. In 2005, she began reading books on the subject, including Jeremy Leggett’s The Empty Tank. Gail did further research about the situation, and wrote her first article about the potential impact on the property-casualty insurance industry in early 2006.

In March 2007, Gail decided to research the issue of limits of a finite world on a full-time basis, leaving her career in insurance consulting. She began OurFiniteWorld.com in 2007, but temporarily changed her writing base to TheOilDrum.com between mid-2007 and 2010, where she was a writer and editor. Since late 2010, her blog posts have been published on OurFiniteWorld.com. These posts are widely republished under Gail’s Creative Commons license; many posts are translated into other languages and republished.

Besides blog posts, Gail is the author of a number of academic papers. The most widely cited is, “Oil Supply Limits and the Continuing Financial Crisis.” Another academic paper of interest is, “An Oil Production Forecast for China Considering Economic Limits,” published in 2016. Section 2 of this paper discusses the possibility that the limit on oil extraction may be a financial limit: prices cannot rise high enough. A longer list of academic papers and papers for insurance audiences is given on the sidebar.

Gail also speaks to many groups regarding her views on energy limits and the economy. She has spoken in many countries around the world, including Italy, Spain, China, and India. She has spoken to academic groups, actuarial groups, “Peak Oil” groups, and more general groups, such as religious groups and graduate students. In early 2015, she taught a course at China University of Petroleum in Beijing on “Energy and the Economy.” In 2017, she was one of the invited speakers at a European Commission workshop relating to “New Narratives of Energy and the Economy” in Brussels. In February 2021, she gave a Zoom lecture called Where Energy Modeling Goes Wrong, on behalf of the Uncomfortable Knowledge Hub.

Gail’s work is different from that of other researchers in that she does not take widely-accepted views as a “given.” Instead she tries to figure out for herself precisely what is happening by looking at a wide range of data and literature, and by investigating leads offered by other researchers and by commenters on OurFiniteWorld.com. In a sense, her wide-ranging view is only possible because of the miracles of the internet and of second-hand books available through Amazon.

One key to Gail’s independence is the fact that she does not take donations or accept advertising on her website. Another key to her independence is the fact that she is not part of the university system, and thus is not subject to the demands of “publish or perish.” Being separate from the university system also allows her to take a broader view of the subject, because “academic silos” are no longer a problem.

Gail has an M. S. from the University of Illinois, Chicago, in Mathematics, and is a Fellow of the Casualty Actuarial Society. She is also a Member of the American Academy of Actuaries. Some of her early writing can be found under the name “Gail the Actuary,” a pen name used on articles published at The Oil Drum between 2007 and 2013. She has literally hundreds of articles on this site, OurFiniteWorld.com.

Gail can be reached at GailTverberg at comcast dot net or at (407) 443-0505. Her twitter feed is @gailtheactuary.

In my view, there are three ways a growing economy can be sustained:

In my view, there are three ways a growing economy can be sustained:

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)