Send this article to a friend:

January

07

2019

|

Send this article to a friend: January |

|

Perhaps The Fed Is Not Clueless

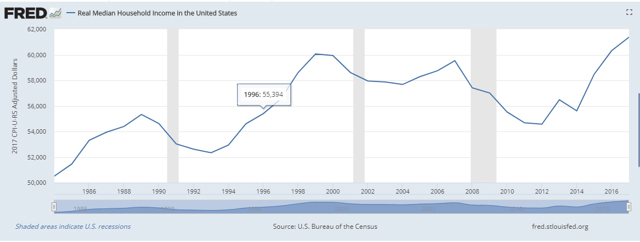

There has been quite a bit of criticism of current Federal Reserve policy in media and certain political circles lately. I have to admit that this article has been inspired by Mr. Cramer's semi-populist rhetoric in regards to the Federal Reserve's policy of raising interest rates, as well as President Trump's criticism in this regard. This critical rhetoric is easy to embrace, especially among the investment community, which has been somewhat rattled by the market activity we saw in the past few months. I cannot say that I am necessarily happy about it myself, given that I have gone from having six out of seven stocks in my portfolio being up, to only three being up, as I write this. But we should keep in mind that while we are going through an unpleasant period of re-adjustment at this moment, after a very long period of very low interest rates that we became accustomed to, perhaps we may all be better off in the longer term, assuming that the Federal Reserve does indeed have valid reasons to opt for monetary tightening. It is not the first time that Mr. Cramer found it necessary to be critical of the activities of the US central bank. He is famously known for the: "They know nothing" statement he made in a 2007 interview, referring to Fed leaders as being out of touch with the reality of the impending crisis, arguing that they should have been loosening monetary policy, in order to accommodate certain companies which were increasingly finding it hard to digest the sub-prime, AAA-rated mortgage loans on their books. Of course, he brought up the prospect of millions of people who were on the brink of losing their homes as a reason for the public to be concerned. There were of course valid reasons for the Fed to opt for higher interest rates back in those days, which we can clearly see in hindsight. The price of oil was just months away from spiking to an all-time record and there were also a number of related and non-related inflationary pressures that it had to be mindful of. It was also most likely mindful of the mortgage debt bubble that was forming in parallel with the housing price bubble. It is hard to say what would have been the outcome if the Federal Reserve would have done what Mr. Cramer wanted them to do back then, namely jump on a preemptive course of loose monetary policy. It might have actually aggravated the crisis, while admittedly possibly delaying it. More than a decade later, Mr. Cramer is criticizing the Federal Reserve again Since the market upheaval of the past few months, Mr. Cramer decided to revisit his own "they know nothing" quote once more, pointing out that while the economy is doing well, there are also some signs of weakness, therefore there is no need to worry about inflation and the economy overheating. He also rightly pointed out the fact that only recently did average households start feeling improvements in their livelihood. In this respect, he is absolutely right. In fact, aside from the last three years or so, median household incomes have been below the level we had in 1999, each and every year, so far this century.

It is also true that after the period of high unemployment, loss of investments, loss of houses and other negative side-effects suffered in the aftermath of what is considered the worst economic downturn since the end of the Second World War, a few years of plentiful jobs, rising wages and improving household finances is just the thing needed for society to get past the pain and trauma inflicted. Not to mention that we are increasingly getting data points which show that the economy is not necessarily in much danger of overheating. The latest ISM Manufacturing numbers show deceleration. New home sales have been weakening, while price increases are moderating.

Source: Trading Economics. New car sales peaked in September 2017 and it does not look like we are about to see a new peak any time soon. We should be mindful, however, that natural disasters played a role in that September 2017 record. While we are seeing some resiliency in auto sales, the overall trend is one of stagnation in this important segment as well. Higher interest rates tend to affect both home and car sales, as well as other major purchases. Looking at all these indicators showing us a less than stellar state of the economy, perhaps Mr. Cramer may have a point. But then there are other factors to consider. For instance, we have the high stock market valuation, which was making it increasingly look overbought.

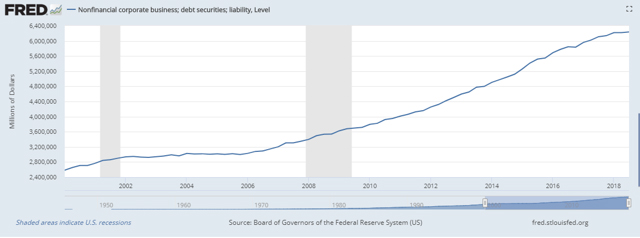

Even with the recent selloff, the market is still far from being a bargain. While we may now be at the point where some investments may be worth looking at, the overall market suggests that even in the event of robust returns going forward, at best it is fairly priced, with little room left for investors to judge the broader market as being a place where the rewards will justify the risk, especially within the context of a very mature recovery, which could give way to a recession at any time going forward. The continued increase in corporate debt is another reason for the Federal Reserve to worry about the effects and eventual outcome of a continued low interest rate environment.

Source: Federal Reserve Bank Of St. Louis. Since the beginning of this century, the total level of corporate debt increased by almost 150%. That is a much higher increase compared with the stock market's current value, even within the context of arguably high valuation levels. Measured up against the growth in the economy overall, it has been outpacing it by a wide margin. The US economy also doubled in non-adjusted terms since the beginning of the century, which is far short of the growth in corporate debt we experienced. There is also the issue of the quality of that debt. Given lower interest rates, relatively weak companies have been able to take on substantial amounts of debt. Shale drillers are the perfect example of this, where a large percentage of companies have been able to tap the bond markets for money, despite the fact that they failed to show a profit for many years in a row. A market desperate for yield accepted it and justified it through less than rational arguments. This situation extends well beyond the shale sector, with many companies which ordinarily would have had a hard time securing funds, finding themselves in favor with the bond markets, for the simple reason that it was the only way for investors to get some yield. There is of course the issue of timing; in other words, questioning whether or not the Federal Reserve may have moved too soon. In this regard, I am in no position to question the Fed's decision, or Mr. Cramer's assessment of it being too soon. But I do think that the reasoning behind the Federal Reserve moving to increase interest rates at a time of its choosing is preferable to waiting for a situation to arrive, such as an oil price spike for instance, where it would have to act in order to stem runaway inflation, while also having to contend perhaps with a corporate debt crisis, or other such issues. Inflation has been over the ideal target of 2% for all of 2018. We should be mindful to take a step back and contemplate where we might be in this regard if the Federal Reserve would have failed to tighten monetary policy in time to preempt a more severe rise in inflation. I have no doubt that the DOW index would be closer or at 30,000 points right now, rather than threatening to visit or breach the 20,000 level, if the Federal Reserve would have been less aggressive in raising rates. Most investors, including yours truly, would no doubt be much happier with that outcome than the one we are experiencing right now on the markets. But this may be short-sighted, because we also want to have a viable economy for the longer term. We certainly do not want potentially unhealthy financial or economic trends to run their course to the point where they blow up in our face, which is when the pain we as investors as well as most households may face as a consequence, would eclipse the relatively minor discomfort that we are experiencing right now. The latest news is that Fed Chair Jay Powell made some rather dovish statements, suggesting that we may see a pause in monetary tightening, or even perhaps a reverse if necessary. Markets are rejoicing and rallying as a result. We should keep in mind, however, that by far the most important thing is for the Federal Reserve to get policy right in the interest of the economy's longer term viability, which is what I hope they have in mind as well. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

My name is Zoltan Ban, I have a double honors degree in history and anthropology, as well as a BA in economics. I am also a personal investor with over a decade of active trading.

|

Send this article to a friend:

|

|

|

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

![[Most Recent USD from www.kitco.com]](http://www.weblinks247.com/indexes/idx24_usd_en_2.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/silver/t24_ag_en_usoz_2.gif)